Did you know that the average tax refund in 2024 was thousands of dollars? While a refund feels like a bonus, it actually means you overpaid the government throughout the year . With the sweeping changes brought by the One Big Beautiful Bill Act and new inflation adjustments for 2026, your paycheck is likely operating under outdated rules.

If you are a salaried employee, the tax landscape has shifted beneath your feet. Social Security wage bases have increased, retirement contribution limits are up, and there are brand-new deductions for things like car loan interest and overtime pay that didn’t exist last year .

In this guide, we cut through the complexity of IRS Publication 15 and the latest union budgets to bring you 10 specific, legal strategies to reduce your taxable income right now. Whether you are a Gen Z professional filing your first W-4 or a seasoned executive looking to harvest investment losses, these actionable tips will help you keep more of your salary in 2026.

Max Out Your Retirement Accounts (Pre-Tax Powerhouses)

The most straightforward way to lower your taxable income is to funnel money into accounts the government wants you to use for retirement. For 2026, the IRS has increased the amounts you can stash away tax-free.

-

401(k) and 403(b) Plans: You can now contribute up to $24,500 of your salary on a pre-tax basis . If you are 50 or older, you get an extra $8,000 catch-up contribution .

-

Traditional IRA: Even if your employer doesn’t offer a plan, you can contribute up to $7,500 (or $8,600 if you’re 50+) and deduct that amount if your income falls under certain limits .

-

The “Super Catch-Up”: For those aged 60-63, the catch-up contribution limit in 2026 is a whopping $11,250, allowing for a total deferral of $35,750 .

Actionable Tip: Log into your retirement account today. If you aren’t hitting the max, increase your contribution by just 1%. You likely won’t miss it in your paycheck, but you will see the difference come tax time.

Embrace the Triple Tax Win of an HSA

If you have a High-Deductible Health Plan (HDHP) through your employer, your Health Savings Account (HSA) is arguably the best tax vehicle in existence. It offers three distinct tax advantages: contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free .

For 2026, the limits have increased:

-

Self-only coverage: You can contribute $4,400 .

-

Family coverage: You can contribute $8,750 .

-

Catch-up (55+): An additional $1,000 .

Unique Insight: Treat your HSA as a “Super IRA.” If you can afford to pay for minor medical expenses out-of-pocket now, let your HSA funds grow tax-free for decades. Pay yourself back later in retirement when you have more significant medical costs.

Use Flexible Spending Accounts (FSAs) Before You Lose Them

Unlike an HSA, a healthcare FSA is generally “use-it-or-lose-it.” However, that shouldn’t deter you from using this powerful tool to lower your taxable income. You can contribute up to $3,400 in 2026 for medical expenses .

Don’t forget about the Dependent Care FSA. If you pay for childcare for a child under 13 or care for an elderly parent so you can work, you can set aside pre-tax dollars for this. It pairs strategically with the Child and Dependent Care Credit (which we cover later), so you need to calculate which gives you a better outcome .

The New “Above-the-Line” Deductions You Can’t Miss

In 2026, you don’t always need to itemize to get major tax breaks. “Above-the-line” deductions lower your Adjusted Gross Income (AGI) even if you take the standard deduction . Thanks to recent legislation, several new ones have appeared:

-

Car Loan Interest Deduction: If you bought a qualifying new vehicle in 2025 or 2026, you may deduct up to $10,000 of the interest paid. This phases out at higher income levels, so check the specifics .

-

Qualified Tips Deduction: Service workers can now deduct up to $25,000 of qualified tips from their income .

-

Qualified Overtime Compensation: For tax years 2025 through 2028, you can deduct up to $12,500 (or $25,000 for joint filers) of qualified overtime pay .

Note: These deductions are temporary, so if you qualify, you need to act now. Ensure your employer notes these on your W-2 to make filing easier .

Table: 2026 Key Deduction Limits at a Glance

| Deduction Type | 2026 Contribution/Limit | Key Feature |

|---|---|---|

| 401(k) / 403(b) | $24,500 | Pre-tax contribution; +$8,000 catch-up |

| Traditional IRA | $7,500 | Deductible based on income; +$1,100 catch-up |

| HSA (Self-only) | $4,400 | Triple tax advantage: pre-tax, growth, withdrawal |

| HSA (Family) | $8,750 | Triple tax advantage for family HDHP coverage |

| FSA (Health) | $3,400 | Use-it-or-lose-it medical expense account |

| Car Loan Interest | Up to $10,000 | New for 2026; qualifying new vehicle purchase |

| Standard Deduction (Single) | $16,100 | No itemizing required; baseline deduction |

| Standard Deduction (MFJ) | $32,200 | No itemizing required; baseline deduction for couples |

Don’t Ignore the “Senior Bonus” Deduction (Even if You’re Not One Yet)

There is a new deduction specifically for taxpayers age 65 and older. It allows for an additional deduction of up to $6,000 for individuals or $12,000 for married couples filing jointly .

-

Income Limit: This phases out for individuals with MAGI over $75,000 ($150,000 for joint filers) .

-

Why this matters for families: If you are supporting an elderly parent, or if you are approaching this age, planning your income streams to stay under the threshold could save thousands.

Strategic Withholding: The W-4 Hack

Many employees “set and forget” their W-4. With the 2026 changes, that is a mistake. If you receive supplemental wages (bonuses, stock options, RSUs), your employer likely withholds at a flat 22% rate .

If you are in a higher tax bracket (32% or more), this 22% withholding won’t be enough, and you’ll owe money next April. Conversely, if you qualify for the new overtime or tip deductions, you can adjust your W-4 to account for that now and receive more money in each paycheck rather than waiting for a refund .

Ponder This: When was the last time you updated your W-4? If it’s been more than two years, your withholding is probably misaligned with your current tax reality.

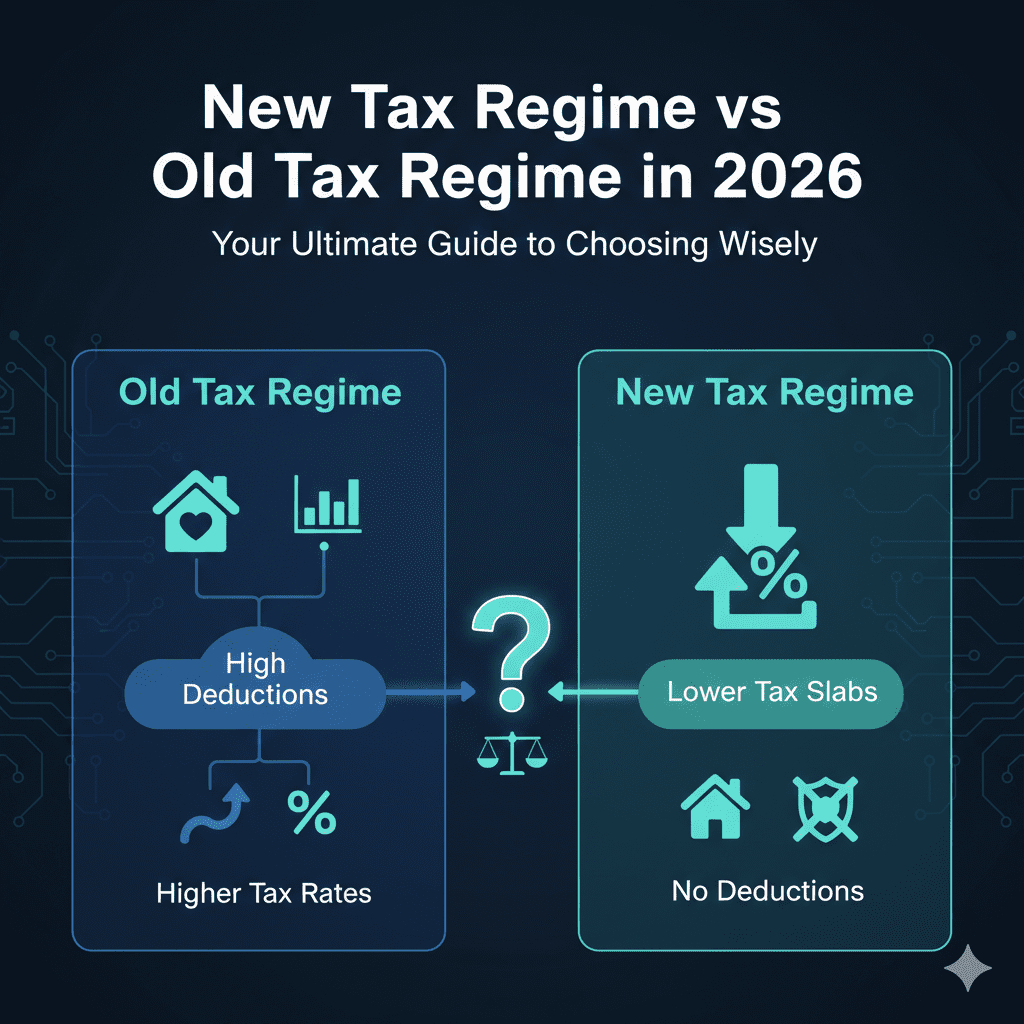

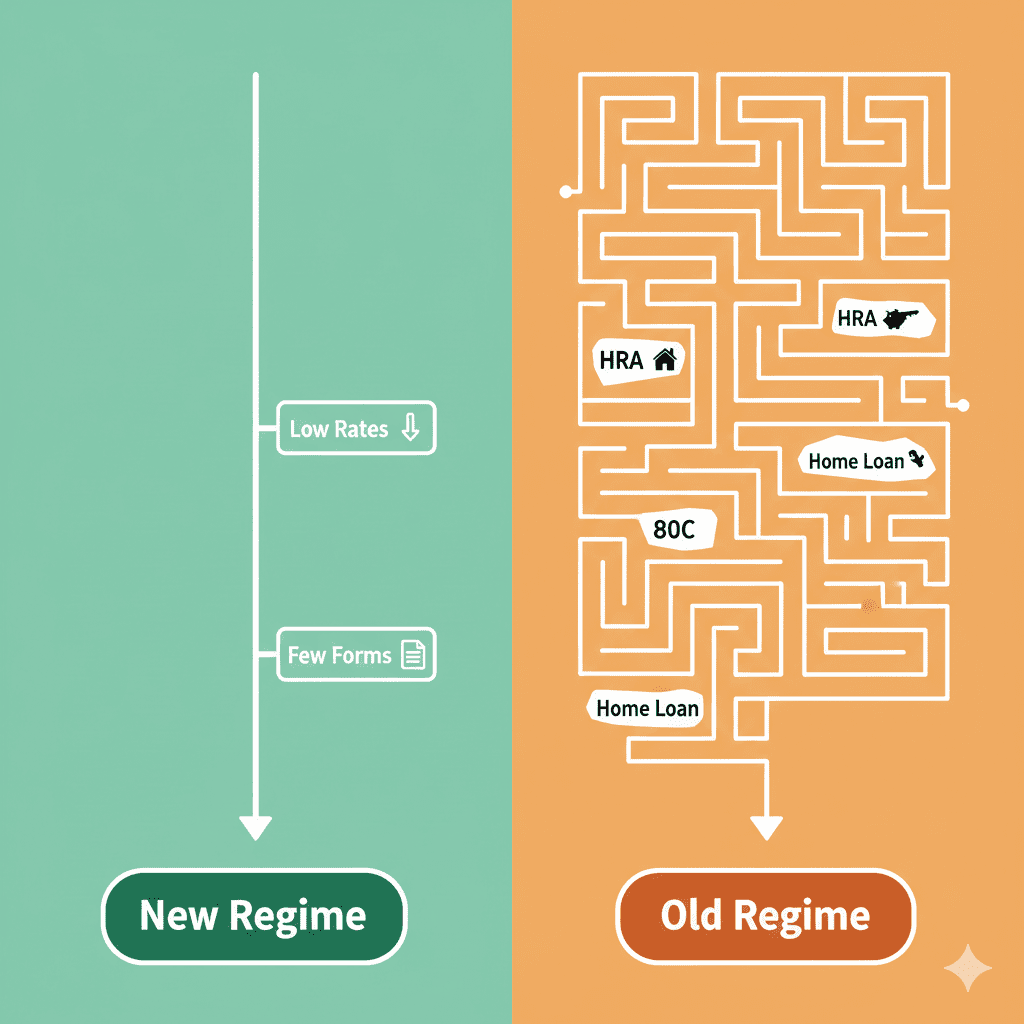

The Old vs. New Regime Dilemma (For International Readers)

Note: While the above focuses on the US tax code (IRS), many of our readers face similar choices globally. For example, the Indian tax regime presents a similar fork in the road.

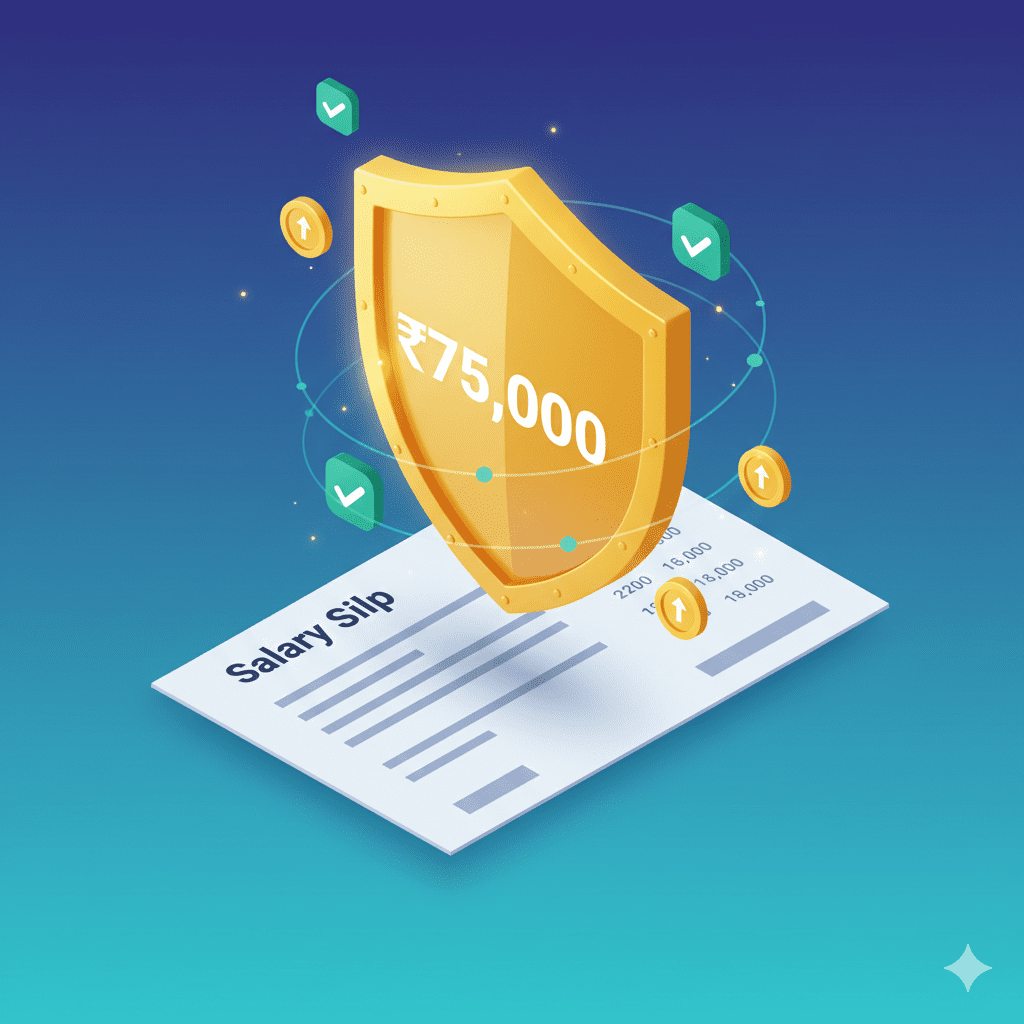

If you are a salaried employee in India, Budget 2026 has made the New Tax Regime the default . It offers lower rates and a higher standard deduction of ₹75,000, making income up to ₹12.75 lakh tax-free . However, you lose popular deductions like 80C (PPF, ELSS) and HRA .

-

Switch Every Year: Salaried employees have the flexibility to choose each year .

-

The Breakeven Point: If your total deductions (HRA + 80C + 80D + Home Loan) are less than a certain threshold (around ₹4-5 lakhs for higher incomes), the New Regime usually wins .

Tax-Loss Harvesting Your Investments

If you sold stocks or crypto at a gain this year (a capital gain), you are likely facing a tax bill. However, you can legally offset this by selling other investments at a loss—a strategy known as tax-loss harvesting .

-

The Limit: You can use losses to offset gains. If your losses exceed your gains, you can deduct up to $3,000 of that loss against your ordinary salary income.

-

The Strategy: Review your portfolio before the end of the year. If you have underperforming assets you were planning to sell anyway, do it now to offset those winners.

Education Credits and Deductions

Even if you aren’t a student, if you are paying off student loans or taking professional courses, you can save.

-

Student Loan Interest: You can deduct up to $2,500 of interest paid on qualified student loans, even if you don’t itemize. This is an above-the-line deduction .

-

Lifetime Learning Credit: If you took a course to learn a new job skill (even if it’s not a degree program), you might qualify for a credit worth up to $2,000 per tax return .

The Charitable Deduction for Non-Itemizers

For years, charitable donations only helped those who itemized. The new rules for 2026 allow cash donations to count even if you take the standard deduction.

-

The Limit: You can claim up to $1,000 (single) or $2,000 (married filing jointly) in cash donations directly off your income .

-

Keep Records: Even though it’s a small deduction, the IRS still requires proof. Keep those bank records and receipts from your favorite non-profits.

Conclusion: Your Paycheck, Your Choice

Saving taxes on your salary isn’t about hiding income; it’s about smartly directing it. The government uses the tax code to incentivize behaviors it wants to see: saving for retirement, investing in health, buying electric cars, and giving to charity. By aligning your financial moves with these incentives, you legally and ethically reduce your tax burden.

The rules for 2026 are set. The contribution limits are higher, and new deductions for everything from overtime to car loans are on the table. The question isn’t whether you can save; it’s whether you will take the time to act.

Your Next Step: Pick just three strategies from this list. Maybe it’s increasing your 401(k) by 1%, setting up that HSA, or checking your W-4. Implement them this week. Your future self—the one with a fatter refund or a smaller tax bill—will thank you.

Frequently Asked Questions (FAQ)

1. Can I contribute to both a 401(k) and an IRA in 2026 to double my tax savings?

Yes, absolutely. The contribution limits for 401(k)s ($24,500) and IRAs ($7,500) are separate. Contributing to both is a fantastic way to maximize your pre-tax savings, provided you have the earned income to support it .

2. I have a high-deductible health plan. Can I have both an HSA and an FSA?

Generally, you cannot have a general-purpose healthcare FSA if you have an HSA, as the FSA would cover first-dollar medical expenses, disqualifying you from the HDHP requirement. However, you can have a Limited-Purpose FSA (for vision and dental only) alongside an HSA .

3. What is the income limit for the new senior deduction in 2026?

The additional standard deduction for those 65 and older phases out for taxpayers with modified adjusted gross income (MAGI) over $75,000 for single filers and $150,000 for married couples filing jointly .

4. Is the new car loan interest deduction available for used cars?

The deduction has strict requirements. It generally applies to interest on qualifying new passenger vehicles purchased between 2025 and 2028. It is best to check the final IRS guidance or consult a tax professional, as it usually does not apply to used cars .

5. How do I claim the deduction for qualified tips?

Employers should be noting qualified tips on your Form W-2. You will then claim this as an above-the-line deduction on Schedule 1 of your Form 1040 when you file. Keep detailed records of your tip income .

6. If I choose the New Tax Regime (India), can I still get a standard deduction?

Yes. Under the new regime for FY 2026-27, salaried employees get a standard deduction of ₹75,000. This is higher than the ₹50,000 available in the old regime .