Meet Rajesh, who runs a small electronics trading business in Delhi. He files his GST returns every month—or so he thought. Last week, he received a notice from the tax department: ₹47,000 in tax demand plus interest for GSTR-1 and GSTR-3B mismatches over six months. The worst part? He had actually collected the tax from customers. He just reported it incorrectly across the two forms.

You’re not alone. Over 35% of GST notices issued in 2025 were related to mismatches between GSTR-1 and GSTR-3B, according to CBIC data. With the new Invoice Management System (IMS) and automated return filing blocks introduced in January 2026, these errors now have immediate consequences—including suspension of returns .

GSTR-1 (details of outward supplies) and GSTR-3B (summary return with tax payment) are the two most critical returns for any regular GST taxpayer. Get them wrong, and you face:

-

Late fees (₹50 per day, up to ₹5,000 per return)

-

Interest at 18% per annum on delayed tax

-

Blocked input tax credit for your customers

-

Mismatch notices demanding explanations

-

Return suspension under new 2026 rules

In this guide, you’ll discover:

-

The 7 most common GSTR-1 and GSTR-3B mistakes (with real examples)

-

How each mistake triggers notices or financial loss

-

Step-by-step prevention strategies

-

How to use tools like India Tax Tools to reconcile before filing

-

New 2026 rules that make accuracy non-negotiable

Let’s fix your GST filings—before the taxman comes knocking.

![]()

MISTAKE #1: MISMATCH BETWEEN GSTR-1 AND GSTR-3B TAX LIABILITY

This is the single most common error and the biggest trigger for GST notices.

What Goes Wrong

You file GSTR-1 with details of all sales invoices (say ₹10 lakh sales, ₹1.8 lakh tax). But in GSTR-3B, you accidentally report only ₹9 lakh sales with ₹1.62 lakh tax—a ₹18,000 mismatch. The GST system automatically flags this because GSTR-1 and GSTR-3B tax liability should match perfectly .

Why It Happens

-

Manual data entry errors (typing wrong totals)

-

Using different accounting bases (invoice vs. cash)

-

Missing invoices in one return but including in another

-

Incorrect classification of exempt vs. taxable sales

Real Example

A Pune-based trader reported ₹22,47,000 in GSTR-1 but only ₹20,15,000 in GSTR-3B for July 2025. The ₹2.32 lakh mismatch triggered a notice. Investigation revealed five high-value invoices were accidentally omitted from GSTR-3B. Outcome: ₹2.32 lakh tax + ₹41,760 interest + ₹5,000 late fee .

How to Avoid

| Prevention Method | How It Works |

|---|---|

| Monthly reconciliation | Before filing GSTR-3B, export GSTR-1 data and verify totals match your sales register |

| Use reconciliation tools | Tools like India Tax Tools’ GST Reconciliation Tool auto-compare GSTR-1 and GSTR-3B data |

| Maintain sales register | Real-time tracking of invoices with tax amounts |

| Auto-population check | Verify that GSTR-3B auto-populated liability matches your calculations |

Key Rule: Your GSTR-1 liability for the month must equal the liability declared in Table 3.1(a) of GSTR-3B. Always reconcile before payment .

MISTAKE #2: INCORRECT OR MISSING HSN/SAC CODES

HSN (Harmonized System of Nomenclature) codes for goods and SAC (Service Accounting Codes) for services are not just bureaucratic formalities—they directly impact tax rates and compliance.

What Goes Wrong

Using a 4-digit HSN when 6-digit is required, applying wrong codes, or mixing up goods and services codes leads to:

-

Incorrect tax rate application

-

ITC denial to customers

-

Mismatch in auto-generated e-invoices

-

Annual return (GSTR-9) reconciliation nightmares

The Rules for 2026

| Turnover Threshold | HSN/SAC Requirement |

|---|---|

| Up to ₹5 crore | 4-digit HSN/SAC optional (but recommended) |

| ₹5 crore – ₹10 crore | 4-digit HSN/SAC mandatory |

| Above ₹10 crore | 6-digit HSN/SAC mandatory |

| Export/Import | 8-digit HSN mandatory |

*Source: CBIC Notification 78/2025 *

How to Avoid

Action Steps:

- Download official HSN/SAC finder from India Tax Tools HSN Code Finder

- Maintain product master with correct codes mapped

- Validate before invoicing – check codes in ERP/accounting software

- Quarterly audit – review HSN/SAC usage across invoices

Pro Tip: Wrong HSN codes can also affect your eligibility for certain GST exemptions or composition schemes. If you’re unsure, use the official HSN search tool on the GST portal or India Tax Tools’ HSN/SAC Finder for accurate codes.

MISTAKE #3: ERRORS IN INPUT TAX Credit (ITC) CLAIMS

Input Tax Credit is the fuel that makes GST work—claiming credit for tax paid on purchases. But incorrect ITC claims are the second most common reason for GST notices.

Common ITC Errors

| Error Type | Description | Consequence |

|---|---|---|

| Claiming without vendor filing | Taking ITC even though supplier hasn’t filed GSTR-3B | ITC reversal + interest + penalty |

| Ineligible ITC claims | Claiming credit on blocked items (personal use, motor vehicles, etc.) | Notice + tax demand |

| Wrong ITC split | Incorrectly dividing ITC between IGST/CGST/SGST heads | Mismatch in returns |

| Missing ITC reversal rules | Not reversing ITC for exempt supplies or payment defaults | Excess credit claimed |

Real Example

A Bhopal-based manufacturer claimed ₹8.2 lakh ITC for purchases from a supplier who hadn’t filed returns for 4 months. During audit, the ITC was disallowed, with demand of ₹8.2 lakh + ₹1.47 lakh interest + ₹10,000 penalty .

The 2026 Rule: ITC Blocked for Non-Filing Vendors

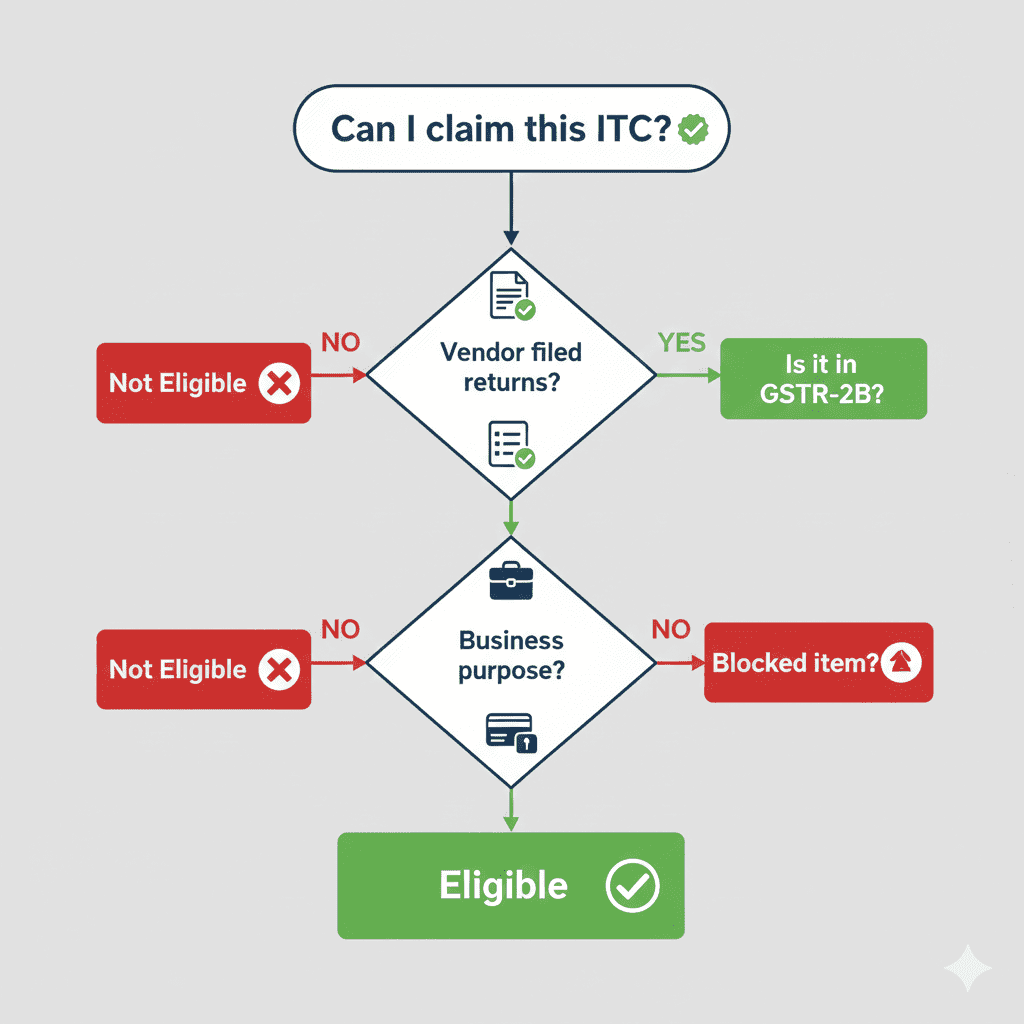

From January 2026, the GST portal automatically blocks ITC if your vendor hasn’t filed GSTR-3B for the relevant period . You can see this in GSTR-2B, which now shows only “eligible” ITC based on vendor compliance.

How to Avoid ITC Errors

Before Claiming ITC, Verify:

-

Vendor has filed GSTR-1 and GSTR-3B for the period

-

Invoice appears in your GSTR-2B

-

Purchase is for business purpose (not blocked list)

-

Goods/services actually received

-

Tax has been paid to vendor

Use the ITC Reconciliation Tool on India Tax Tools to:

-

Match purchase invoices with GSTR-2B

-

Identify vendors who haven’t filed

-

Track ITC reversals needed

Golden Rule: Only claim ITC that appears in your GSTR-2B. Everything else is at your own risk .

MISTAKE #4: MISMATCH IN ADVANCE RECEIPT REPORTING

Advance receipts are tricky because GST is payable when you receive payment, not when you issue the invoice.

What Goes Wrong

You receive ₹50,000 advance from a customer in March but don’t issue invoice until April. Many taxpayers:

-

Forget to report advance in GSTR-1 (it must be reported in Table 11)

-

Don’t pay tax on advance in GSTR-3B

-

Later, when invoice issued, fail to adjust advance correctly

Consequences

-

Tax on advance remains unpaid → interest at 18%

-

Mismatch between GSTR-1 (advance shown) and GSTR-3B (no tax paid)

-

Duplicate reporting if adjustment not done properly

How to Handle Advances Correctly

| Scenario | GSTR-1 Reporting | GSTR-3B Reporting |

|---|---|---|

| Advance received, no invoice | Table 11 (Advance receipts) | Pay tax in 3.1(a) as advance |

| Invoice issued against advance | Table 4 (regular invoices) and adjust advance in Table 11 | Show invoice tax and claim reduction for advance tax already paid |

| Advance adjusted partially | Proportional adjustment in Table 11 | Track remaining advance liability |

Use India Tax Tools’ Advance Receipt Tracker to monitor advances and adjustments month-to-month.

MISTAKE #5: INCORRECT REPORTING OF DEBIT/CEDIT NOTES

Debit and credit notes are essential for business adjustments, but they’re frequently mismanaged in GST returns.

Common Errors

| Error | What Happens |

|---|---|

| Credit note not linked to original invoice | System can’t match reduction, shows as separate supply |

| Reporting in wrong month | Credit note must be reported in month of issuance |

| Wrong tax rate in credit note | Mismatch with original invoice rate |

| Debit note for additional consideration | Treated as separate supply if not linked |

The Rules

-

Credit notes: Reduce your liability in the month issued, but must be linked to original invoice number

-

Debit notes: Increase liability, report as additional supply

-

Time limit: Credit notes can be issued up to 30th November of next financial year (for annual returns)

How to Avoid

For Credit Notes:

-

Always mention original invoice number and date

-

Ensure tax rate matches original invoice

-

Report in Table 9 of GSTR-1 in month of issuance

-

Verify reduction appears correctly in GSTR-3B

For Debit Notes:

-

Report as regular supply in Table 4

-

Link to original invoice if applicable

-

Pay tax in month of issuance

Use India Tax Tools’ Debit/Credit Note Manager to track all adjustments and ensure proper linking.

MISTAKE #6: IGNORING TIME LIMITS FOR ITC CLAIMS

Section 16(4) of CGST Act imposes strict deadlines for claiming ITC. Missing them means permanent loss of credit.

The Deadlines

| Period | ITC Claim Deadline |

|---|---|

| For FY 2024-25 | Due date of GSTR-3B for September 2025 |

| For FY 2025-26 | Due date of GSTR-3B for November 2026 (tentative) |

| Annual Return | Must reconcile ITC claimed vs. eligible |

What Goes Wrong

You receive an invoice from March 2025 in April 2025. If you don’t claim ITC by the September 2025 GSTR-3B deadline, that ITC is lost forever—even if you later file an annual return.

Real Example

A Chennai-based auto parts dealer missed claiming ₹3.4 lakh ITC on capital goods purchased in February 2025. The invoices arrived late, and by the time accounting caught up, the September 2025 deadline had passed. Result: ₹3.4 lakh permanent loss .

How to Avoid

Action Checklist:

-

Maintain invoice receipt register with dates

-

Set calendar reminders for ITC deadlines (September/November each year)

-

Reconcile purchase invoices with GSTR-2B quarterly

-

For missing invoices, follow up with vendors immediately

Use the ITC Deadline Tracker on India Tax Tools to monitor cut-off dates and pending invoices.

MISTAKE #7: FILING AFTER DEADLINES – LATE FEES AND BLOCKED RETURNS

Late filing isn’t just about penalties—with 2026 automation, it can block your entire GST ecosystem.

The Cost of Delay

| Return | Late Fee | Interest | Additional Consequence |

|---|---|---|---|

| GSTR-1 | ₹50/day (₹20 if nil) | N/A | Next month’s GSTR-3B may be blocked |

| GSTR-3B | ₹50/day (max ₹5,000) | 18% p.a. on tax due | Cannot file current month if previous pending |

| GSTR-9 (Annual) | ₹200/day (max 0.5% of turnover) | N/A | Future registrations impacted |

New 2026 Rule: Automatic Suspension

If you miss filing GSTR-3B for two consecutive months, the portal now automatically blocks you from filing future returns and generating e-way bills . Your registration is effectively suspended until you file the pending returns.

How to Avoid

Practical Tips:

-

Set calendar alerts – 10th (GSTR-1), 20th (GSTR-3B) every month

-

File even if nil – Nil returns also need filing; late fee applies otherwise

-

Use return trackers – India Tax Tools Return Due Date Calendar

-

Maintain buffer – Don’t wait until last day; technical glitches happen

-

Reconcile early – Start preparing data by month-end

Pro Tip: If you have multiple GST registrations, track each separately. Late filing for one GSTIN affects only that entity, but can impact overall compliance rating.

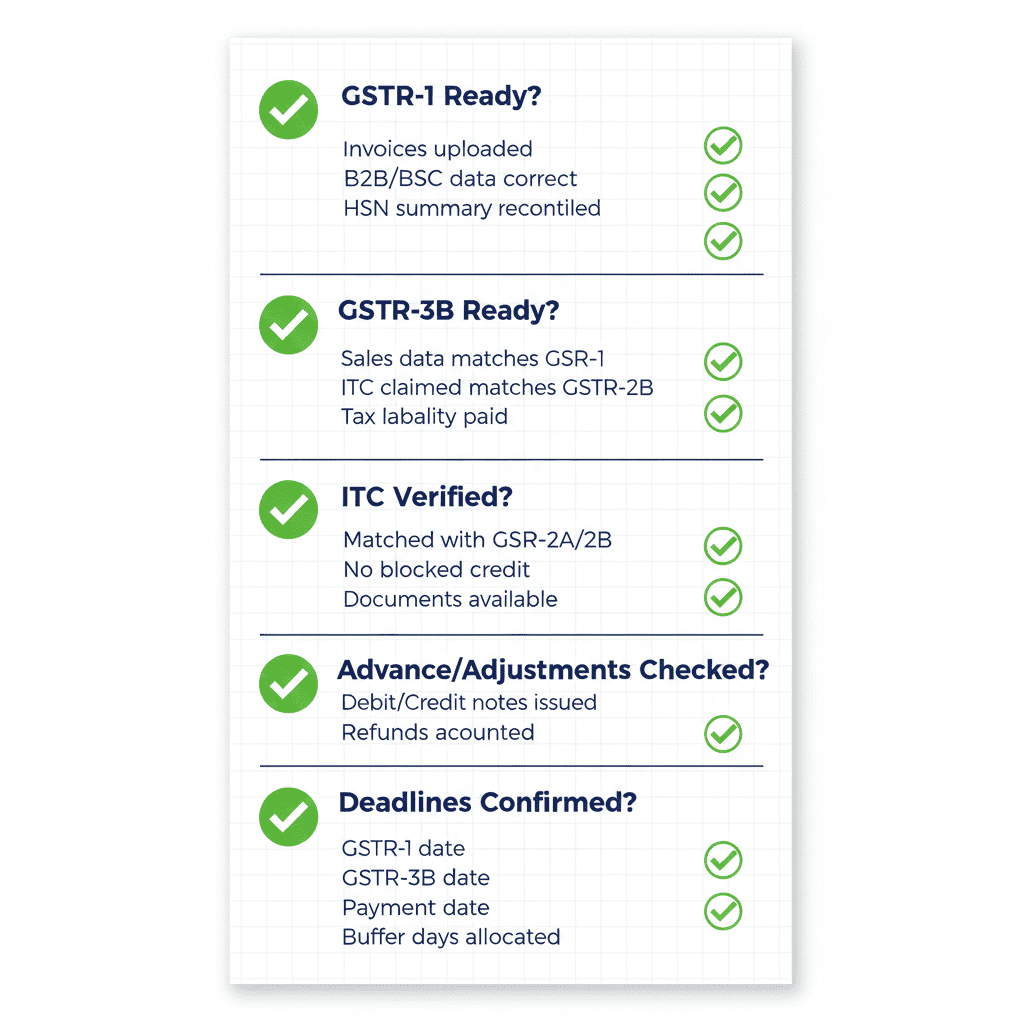

BEFORE YOU FILE: RECONCILIATION CHECKLIST

Use this checklist before submitting any GSTR-1 or GSTR-3B. It takes 15 minutes and saves thousands in penalties.

GSTR-1 Verification

| Check | Done? |

|---|---|

| All sales invoices for the period included? | ☐ |

| Debit/credit notes properly linked to original invoices? | ☐ |

| HSN/SAC codes correct (as per turnover threshold)? | ☐ |

| Advances received reported in Table 11? | ☐ |

| Exempt/Nil-rated supplies correctly classified? | ☐ |

| Inter-state vs. intra-state supplies correctly coded? | ☐ |

| Total tax liability matches sales register? | ☐ |

GSTR-3B Verification

| Check | Done? |

|---|---|

| Total tax liability matches GSTR-1 (Table 3.1(a))? | ☐ |

| ITC claimed matches GSTR-2B eligible credit? | ☐ |

| ITC split correctly between IGST/CGST/SGST? | ☐ |

| Tax paid through cash ledger matches liability? | ☐ |

| Previous period adjustments correctly carried forward? | ☐ |

| Bank account details updated (to avoid suspension)? | ☐ |

ITC Verification

| Check | Done? |

|---|---|

| All vendors whose ITC you claim have filed GSTR-3B? | ☐ |

| Invoices appear in GSTR-2B? | ☐ |

| ITC on capital goods correctly reported? | ☐ |

| Reversals under Rule 42/43 (exempt supplies) applied? | ☐ |

| ITC claimed within time limit (September/November deadline)? | ☐ |

Final Checks

| Check | Done? |

|---|---|

| Previous month’s returns filed (no blocking)? | ☐ |

| Bank balance sufficient for tax payment? | ☐ |

| Filing deadline still open (not last minute)? | ☐ |

| Downloaded and saved filed returns? | ☐ |

| E-way bills generated for all goods movement? | ☐ |

FREQUENTLY ASKED QUESTIONS

Q1: What is the penalty for GSTR-1 and GSTR-3B mismatch?

The GST system automatically flags mismatches. If the mismatch is due to incorrect reporting, you’ll receive a notice (FORM GST ASMT-10). If tax is short-paid, you must pay:

-

Tax demand (short-paid amount)

-

Interest at 18% per annum from due date

-

Penalty of up to 10% of tax or ₹10,000, whichever is higher

Q2: Can I revise GSTR-1 after filing?

No, GSTR-1 cannot be revised once filed. However, you can correct errors in subsequent months’ returns by issuing debit/credit notes or including missed invoices in future GSTR-1 . For annual return (GSTR-9), you can reconcile and adjust.

Q3: What is the new Invoice Management System (IMS) from 2026?

IMS, introduced in January 2026, allows recipients to Accept, Reject, or Keep Pending invoices reported by suppliers in GSTR-1. Only accepted invoices flow into GSTR-2B for ITC claims. This reduces mismatches but requires active reconciliation monthly .

Q4: How do I reconcile GSTR-1 and GSTR-3B?

Step-by-step:

- Export GSTR-1 data from portal (Excel/JSON)

- Note total taxable value and tax liability (IGST/CGST/SGST)

- In GSTR-3B, verify Table 3.1(a) matches these totals

-

If mismatch, check for:

-

Advances reported in GSTR-1 but not in GSTR-3B

-

Debit/credit notes affecting liability

-

Export/international supplies treated differently

-

-

Use India Tax Tools Reconciliation Tool for automated matching

Q5: What if my vendor hasn’t filed GSTR-3B? Can I still claim ITC?

No. From January 2026, ITC is automatically blocked in GSTR-2B if vendor hasn’t filed GSTR-3B for that period . You cannot claim ITC on such invoices until vendor files. Follow up with vendor immediately.

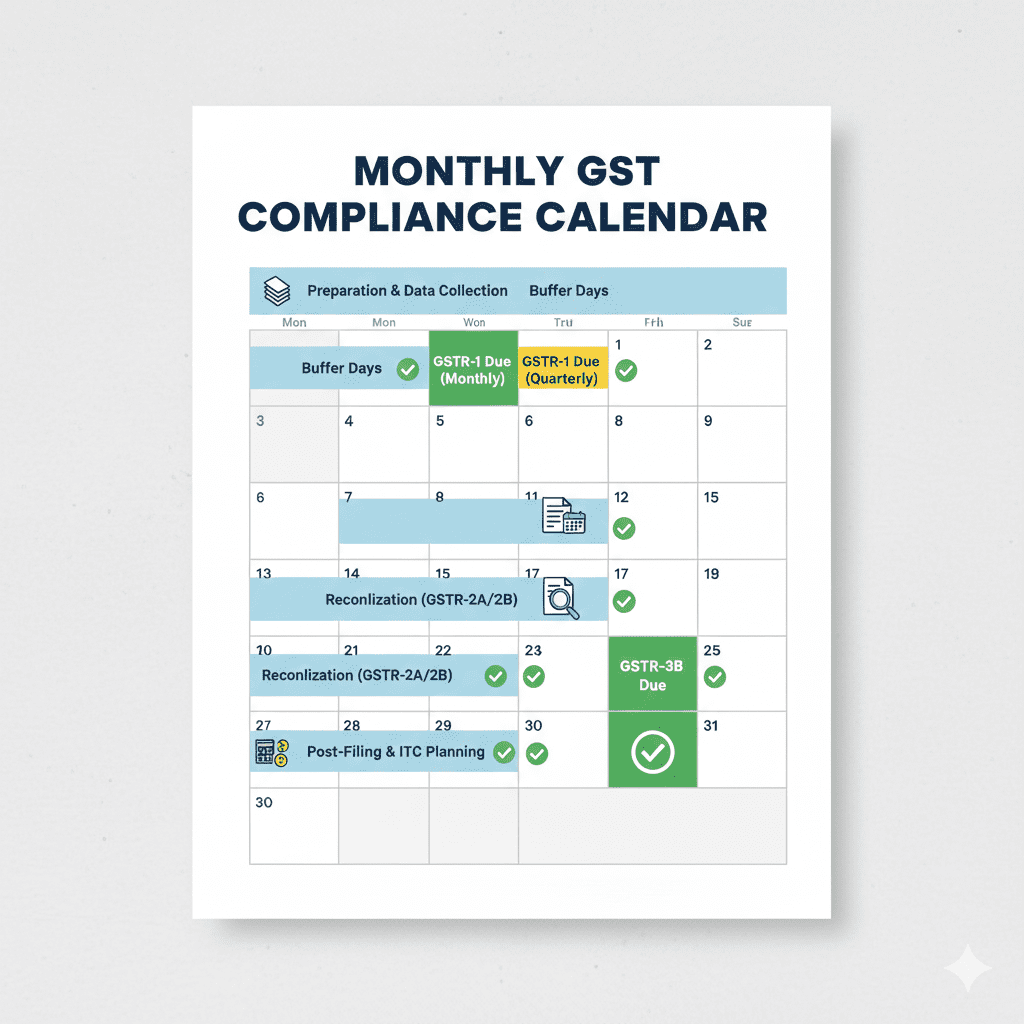

Q6: What is the due date for GSTR-1 and GSTR-3B?

| Return Type | Frequency | Due Date |

|---|---|---|

| GSTR-1 | Monthly | 11th of next month |

| GSTR-1 | Quarterly (QRMP) | 13th of month after quarter |

| GSTR-3B | Monthly | 20th of next month |

| GSTR-3B | Quarterly (QRMP) | 22nd/24th of month after quarter (with GST PMT-08 payment) |

*Note: QRMP taxpayers pay tax monthly (PMT-08 by 25th) but file returns quarterly *

Q7: How can I check if my GSTR-1 and GSTR-3B match?

On the GST portal:

- Go to Services > Returns > Track Return Status

- Select financial year and month

- View both GSTR-1 and GSTR-3B status

- Click “View” to see filed details

- Compare total tax liability

Alternatively, use the GST Return Comparison Tool on India Tax Tools for automated mismatch detection.

Q8: What happens if I file GSTR-3B late?

Late fees apply:

-

₹50 per day (₹25 CGST + ₹25 SGST) if tax is payable

-

₹20 per day (₹10 + ₹10) for nil returns

-

Maximum ₹5,000 per return

Additionally, if you miss two consecutive months, the portal blocks future filings and e-way bill generation until pending returns are filed .

CONCLUSION: MASTER YOUR GST RETURNS, AVOID PENALTIES

GSTR-1 and GSTR-3B filing doesn’t have to be a source of anxiety. The seven mistakes we’ve covered—from simple mismatches to missed deadlines—account for the vast majority of GST notices issued today. And with the new 2026 automation rules, these errors now have immediate consequences: blocked returns, suspended e-way bills, and automatic ITC reversals.

But here’s the empowering truth: every single one of these mistakes is preventable.

Your Action Plan

- Reconcile monthly – Before filing, verify GSTR-1 liability matches GSTR-3B

- Check GSTR-2B – Only claim ITC that appears here

- Track deadlines – Set calendar alerts; don’t wait until last day

- Maintain records – Sales register, ITC tracker, advance receipt log

- Use technology – Leverage tools like India Tax Tools for automated reconciliation and error checking

Your Next Steps

-

Bookmark this guide and use the checklist before every filing

-

Share with your accounts team – ensure everyone understands these pitfalls

-

Set up monthly reconciliation using India Tax Tools GST Reconciliation Suite

-

If you received a notice, don’t panic—use the reconciliation steps above to prepare your response

Remember: GST compliance isn’t just about avoiding penalties. It’s about building a business that’s trusted by vendors, valued by customers, and respected by the tax department. Start with accurate returns—everything else follows.

“In GST, accuracy isn’t expensive—but inaccuracy is. A 15-minute monthly reconciliation saves lakhs in penalties, interest, and sleepless nights. Make it non-negotiable.”

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice. GST laws, rules, and deadlines are subject to change based on government notifications and GST Council decisions. Please consult a qualified Chartered Accountant or GST practitioner for advice tailored to your specific business circumstances. The information provided is based on GST rules and updates available as of February 2026.