Did you know that over 58% of Indian salaried employees might be paying more tax than necessary simply because they chose the wrong tax regime? As we step into the financial year 2024-25 (assessment year 2025-26), the choice between India’s New Tax Regime and Old Tax Regime has become more complex—and more consequential—than ever before. With the government making the New Regime the default option and introducing significant changes in Budget 2023 and subsequent updates, taxpayers are facing a crucial decision that could impact their annual take-home pay by lakhs of rupees.

This isn’t just about checking a box on your ITR form. It’s about understanding a fundamental shift in India’s tax philosophy: fewer deductions in exchange for lower rates. Whether you’re a fresh graduate filing for the first time, a mid-career professional with home loan EMIs, or someone planning retirement, choosing the right regime requires careful calculation tailored to your unique financial life.

In this comprehensive guide, we’ll break down both regimes with clear 2026-specific data, provide real-case scenarios, and give you a simple framework to make the optimal choice. By the end, you’ll have the clarity and confidence to select the regime that puts more money back in your pocket.

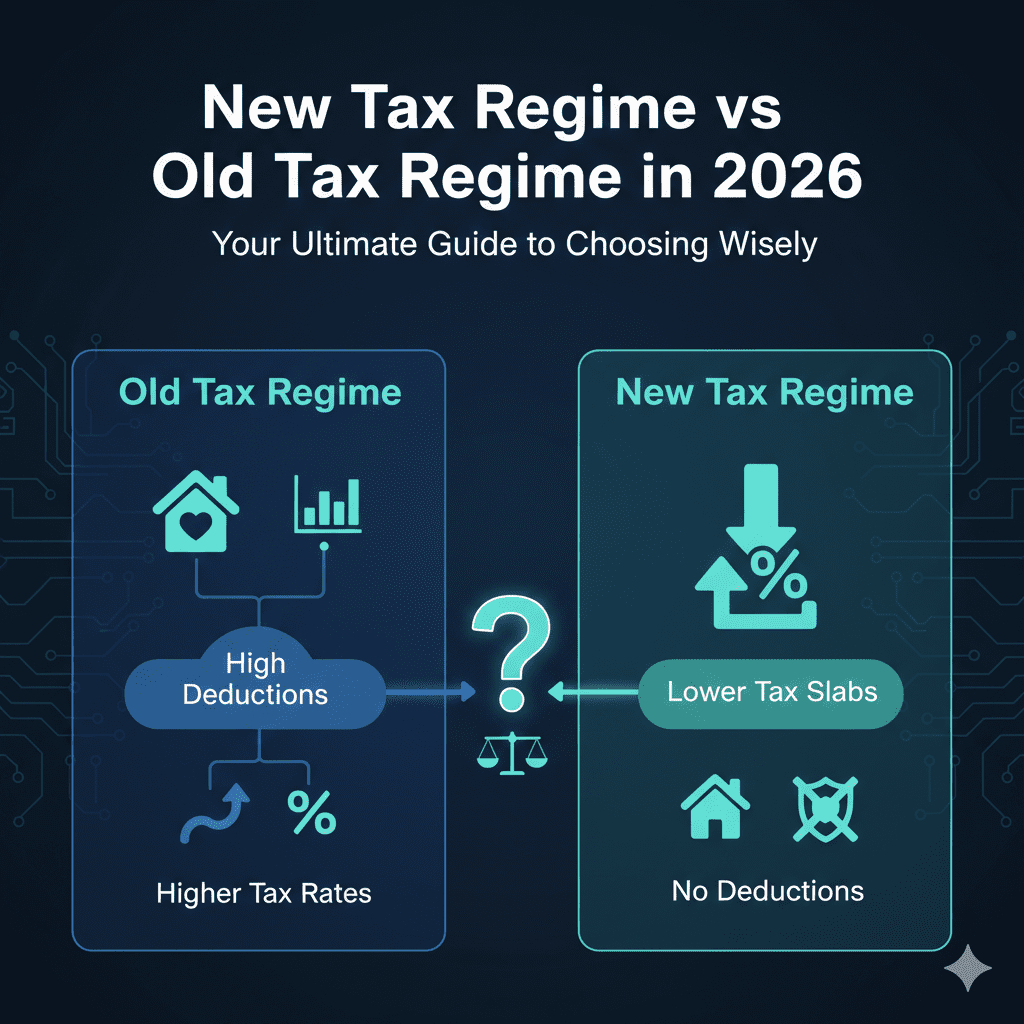

The Fundamental Difference: A Shift in Tax Philosophy

When the New Tax Regime was introduced in Budget 2020, it wasn’t just another tax bracket adjustment—it represented a philosophical pivot in how India approaches personal taxation. The Old Regime operates on a principle of “incentivized compliance.” The government encourages specific financial behaviors—buying insurance, investing in equity, purchasing a home, donating to charity—by offering tax deductions and exemptions under various sections like 80C, 80D, 24(b), and 80G.

The New Regime, conversely, follows a principle of “simplified taxation.” It dramatically pares down these incentives (with a few exceptions introduced later) in exchange for lower slab rates. Think of it as the government saying: “We’ll charge you less upfront, but we won’t give you as many ways to reduce your bill.”

Why This Matters for You in 2026:

The “default status” change is critical. Unless you actively opt-out by filing Form 10IE (or informing your employer via declaration), you will be taxed under the New Regime. This passive choice could cost you dearly if your financial profile is better suited to the Old Regime.

💡 Pro Tip: Don’t let inertia decide your tax liability. Make this an active, informed decision every year, as your financial situation evolves.

Old Tax Regime in 2026: Deductions, Discipline, and Detail

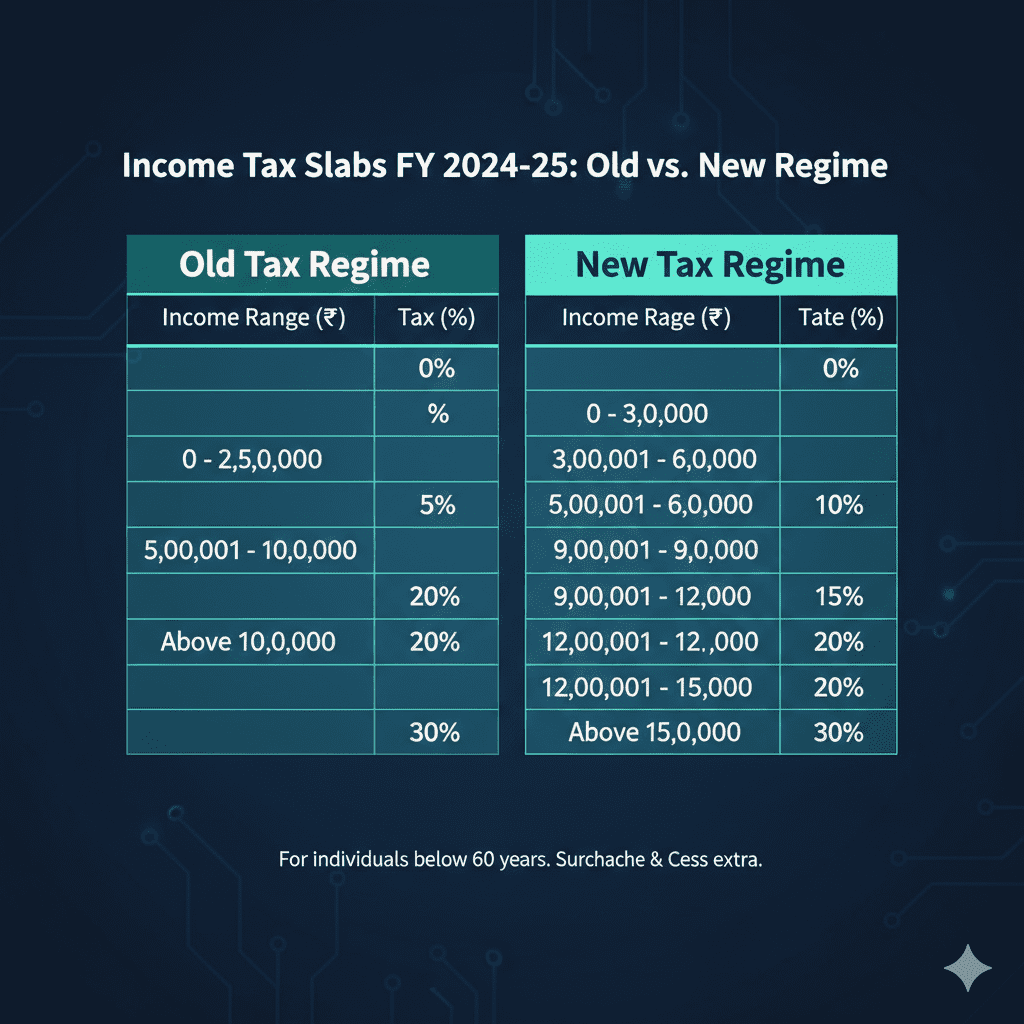

The Old Regime remains a powerful tool for disciplined investors and those with significant deductible expenses. Here’s what it looks like for FY 2024-25 (AY 2025-26):

Tax Slabs (Old Regime):

-

Up to ₹3,00,000: Nil

-

₹3,00,001 – ₹5,00,000: 5%

-

₹5,00,001 – ₹10,00,000: 20%

-

Above ₹10,00,000: 30%

*(+ applicable surcharge & 4% cess)*

Key Deductions & Exemptions Available:

-

Section 80C (₹1.5 Lakh): EPF, PPF, ELSS, Life Insurance Premium, Principal Repayment of Home Loan, NSC, Tuition Fees, etc.

-

Section 80D (₹25,000 – ₹75,000): Health Insurance Premium for self, family, and parents.

-

Section 24(b) (₹2 Lakh): Interest on Home Loan for self-occupied property.

-

HRA Exemption: For salaried individuals living in rented accommodation.

-

LTA/LTC: Leave Travel Allowance/Concession.

-

Standard Deduction: ₹50,000 for salaried individuals.

-

Other Sections: 80E (Education Loan), 80G (Donations), 80TTA/TTB (Savings Account Interest), etc.

The Verdict: The Old Regime rewards a long-term, goal-oriented financial approach. If you are already maximizing your 80C investments, paying health insurance, and servicing a home loan, this regime is likely still your champion.

New Tax Regime in 2026: Simplicity, Lower Rates, and Fewer Headaches

The New Regime has been made more attractive with revised slabs. It is now the default option.

Tax Slabs (New Regime – Default for FY 2024-25):

-

Up to ₹3,00,000: Nil

-

₹3,00,001 – ₹7,00,000: 5%

-

₹7,00,001 – ₹10,00,000: 10%

-

₹10,00,001 – ₹12,00,000: 15%

-

₹12,00,001 – ₹15,00,000: 20%

-

Above ₹15,00,000: 30%

*(+ applicable surcharge & 4% cess)*

What You CAN Claim (Limited List):

-

Standard Deduction of ₹50,000 (for salaried) and deduction for family pension (₹15,000).

-

Employer’s contribution to NPS, Agniveer Fund, and deductions under Section 80CCD(2).

-

Deduction for interest on home loan for let-out properties (not for self-occupied).

What You CANNOT Claim: Most major chapters are closed—Sections 80C, 80D, 80G, HRA, LTA, and deduction for interest on self-occupied home loan (Section 24(b)).

The Verdict: This regime is a boon for young professionals, freelancers with variable income, or those who haven’t yet built a portfolio of deductible investments. If your total potential deductions are less than ₹3-4 lakhs, the New Regime’s lower slabs often work out better.

Side-by-Side Comparison: A 2026 Reality Check

Let’s move beyond theory. The decision almost always boils down to a number. Use the table below as a starting point for your calculation.

Table 1: Tax Regime Feature Comparison (2026)

| Feature | Old Tax Regime | New Tax Regime (Default) |

|---|---|---|

| Default Status | Must actively choose via form/declaration | Automatic. Must opt-out. |

| Basic Exemption | ₹2.5 Lakh | ₹3 Lakh |

| Tax Slabs | Higher rates kick in earlier (20% at >₹5L) | Lower rates for longer (20% only at >₹12L) |

| Standard Deduction | ₹50,000 (Salaried) | ₹50,000 (Salaried) |

| Section 80C | ✅ Up to ₹1.5 Lakh | ❌ Not Available |

| HRA Exemption | ✅ Available | ❌ Not Available |

| Home Loan Interest (Self-occupied) | ✅ Up to ₹2 Lakh (Sec 24) | ❌ Not Available |

| Health Insurance (80D) | ✅ Up to ₹75,000 | ❌ Not Available |

| Simplicity | Complex, requires proof | Very simple, minimal documentation |

Table 2: Case Study – Who Should Choose What? (Taxable Income after Standard Deduction)

| Persona | Annual Income | Key Financial Details | Likely Better Regime | Why? |

|---|---|---|---|---|

| Rohan, Early Professional | ₹9 Lakh | No major investments, rents a house, minimal insurance. | New Regime | Deductions would be low; benefits more from extended lower slabs. |

| Priya, Mid-Career Planner | ₹15 Lakh | Invests ₹1.5L in 80C, pays ₹25k health insurance, has home loan. | Old Regime | High total deductions (₹1.5L+₹25k+₹2L interest) outweigh slab benefit. |

| Arun, NRI Returning to India | ₹20 Lakh | Building investments, may not have HRA/80C fully optimized yet. | New (Temporarily) | Use New for simplicity now, switch to Old after building deductible portfolio. |

| Family with Senior Parents | ₹18 Lakh | High health insurance (₹1L+), home loan, 80C investments. | Old Regime | Very high total deductible amount under sections 80C, 80D, and 24(b). |

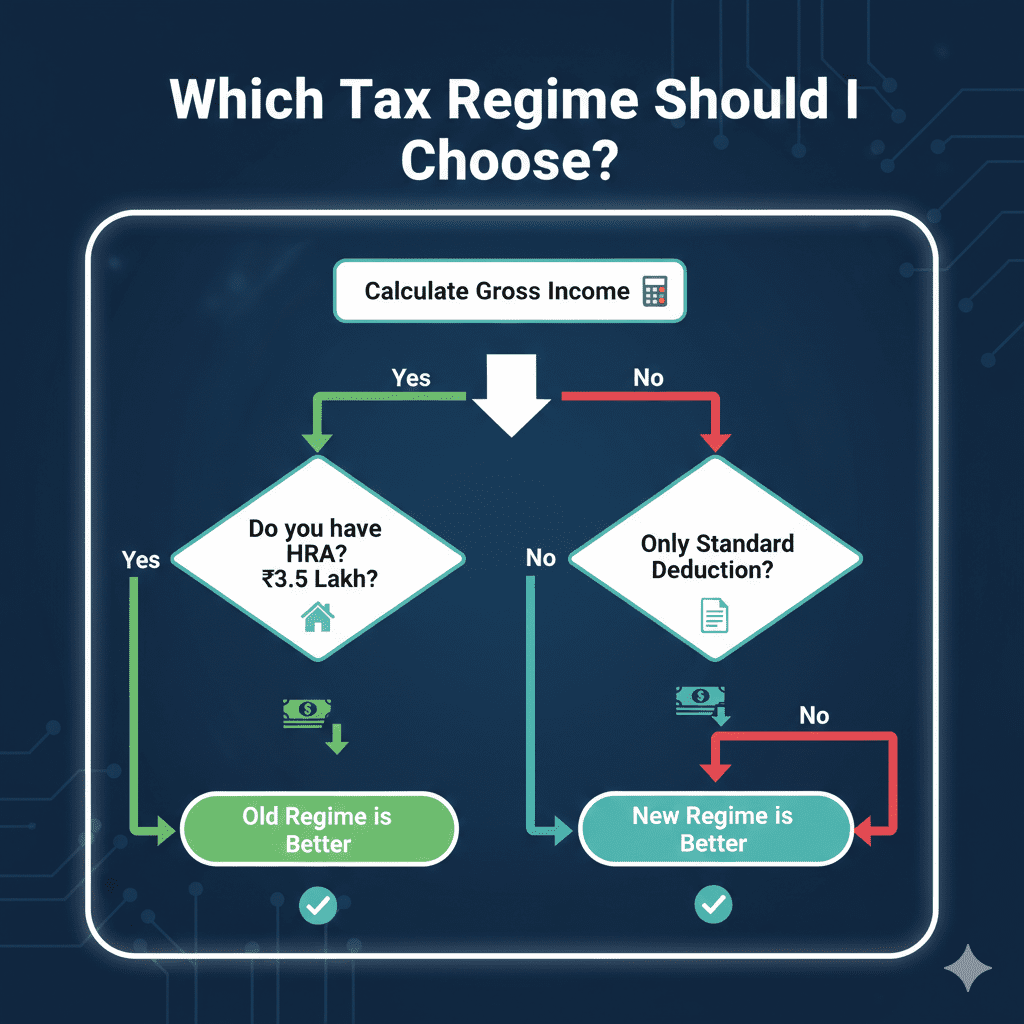

Your Personal Decision Matrix: A Step-by-Step Guide

Stop guessing. Follow this actionable 5-step checklist to find your answer.

Step 1: Calculate Your Gross Taxable Income.

(Include salary, house property income, other sources, etc.)

Step 2: List ALL Potential Deductions/Exemptions (Old Regime).

-

Standard Deduction: ₹50,000

-

HRA Exemption: Calculate based on salary, rent paid, and city.

-

Section 80C Investments: (EPF, PPF, ELSS, etc.) Max: ₹1,50,000

-

Home Loan Interest (Sec 24): Up to ₹2,00,000

-

Health Insurance (80D): Up to ₹75,000

-

Others (80E, 80G, etc.): _________

-

TOTAL (A): _________ (This is your “Deduction Shield”)

Step 3: Calculate Tax Under Both Regimes.

-

Old Regime Tax: (Gross Income – TOTAL A) → Apply Old Regime Slabs.

-

New Regime Tax: (Gross Income – ₹50,000 Std Deduction) → Apply New Regime Slabs.

(Use our Advanced Tax Calculator to automate this in seconds.)

Step 4: Consider Non-Financial Factors.

-

Simplicity vs Optimization: Do you value time over maximum savings?

-

Future Planning: Are you about to buy a house or increase insurance?

-

Lifestyle: Will your HRA claim be significant this year?

Step 5: Decide and Communicate.

-

If Old Regime is better → Inform your employer now via declaration & ensure you file Form 10IE at the time of ITR filing.

-

If New Regime is better → You need do nothing. It’s the default.

Common Pitfalls and Pro Advice for 2026

❌ The “Set-and-Forget” Mistake: Your optimal regime can change year-to-year. A new home loan, a job change with different HRA, or increased investments warrant a fresh calculation.

✅ Our Advice: Conduct this “regime check-up” every November/December (Q3 of the financial year). This gives you time to make strategic investments if switching to the Old Regime makes sense.

❌ The Employer Declaration Blunder: Many assume telling their HR is enough. You MUST also file Form 10IE on the income tax portal while filing your ITR to formally opt-out of the New Regime. Missing this means the tax department will process your return under the New Regime, potentially leading to a demand notice.

✅ Our Advice: Set a calendar reminder for July: “File ITR & Form 10IE (if applicable).”

❌ Overlooking the “Middle-Income Trap”: Individuals with taxable incomes between ₹7.5 lakh and ₹15 lakh are often in the closest zone. A difference of one deduction can flip the answer. Precision is key.

Conclusion: It’s About Your Money, Your Choice

The New versus Old Tax Regime debate doesn’t have a universal winner—only a personal champion based on your unique financial fingerprint. The Old Regime remains a potent tool for strategic wealth builders, while the New Regime offers genuine simplicity and value for those starting out or with uncomplicated finances.

As we look toward 2026, the trend is clear: the government is incentivizing the New Regime. However, true financial wisdom lies in running the numbers for yourself, not following the default path. Use the matrix, calculators, and checklist provided here. The few minutes you spend today could translate into tens of thousands of rupees saved this year, and a stronger, more intentional financial foundation for years to come.

Your Next Step: Don’t just read—act. Head to our Advanced Tax Calculator, input your numbers, and get a definitive answer in 60 seconds. Then, share this guide with a colleague who might be leaving money on the table.

FAQ Section

Q1: Can I switch between regimes every year?

A: Yes, absolutely. You can choose a different regime each financial year. This flexibility allows you to adapt to life changes—like taking a home loan one year or having a year with lower income.

Q2: I am a senior citizen. Which regime is better for me?

A: Senior citizens often have higher health insurance premiums (80D) and interest income deductions (80TTB). These are not available under the New Regime. Therefore, the Old Regime is typically more beneficial for seniors, but a calculation with your specific income and deductions is still essential.

Q3: If I choose the New Regime, should I stop my PPF/ELSS investments?

A: No. You should never stop prudent investments just for tax saving. PPF, ELSS, NPS, and health insurance are pillars of long-term financial health and security. Choose investments for their returns and purpose first; tax benefit is a secondary, albeit valuable, perk.

Q4: How do I inform my employer about my regime choice?

A: At the start of the financial year (usually around April), your employer’s HR or finance department will ask for an investment declaration. In that form, there will be an option to select your preferred tax regime. Submit this in writing and keep a copy. Remember, you still need to file Form 10IE later.

Q5: What if I make the wrong choice? Can I change it later?

A: Once you file your Income Tax Return (ITR) for a financial year, your choice for that year is locked in. However, you can switch when filing for the next year. This underscores the importance of getting it right before the July 31st (or extended) deadline.

Q6: Are there any hidden benefits in the New Regime?

A: The main “hidden” benefit is reduced compliance burden. You don’t need to collect or submit proof for most deductions (except salaried individuals need proof for standard deduction to employer). This saves time and minimizes scrutiny on your investment claims.

Disclaimer: The information provided in this article is for general informational and educational purposes only, based on the tax laws applicable for the Financial Year 2024-25 (Assessment Year 2025-26) and subsequent updates known at the time of writing. Tax laws, slabs, and regulations are subject to change by the Government of India. The content here should not be construed as professional tax or legal advice. You should consult with a qualified Chartered Accountant or tax professional to understand how the tax laws apply to your specific financial situation before making any decisions. We do not accept any liability for any loss or damage incurred by reliance on the information contained in this article.