It’s that time of the year again. Your HR department has sent that daunting email: “Declare your tax regime preference for FY 2026-27.” You stare at your salary slip, your PPF statements, your housing loan documents, and wonder: Am I leaving money on the table?

You are not alone. According to recent data from the CBDT, a staggering 88% of individual taxpayers have already moved to the New Tax Regime . Yet, for the remaining 12%—and even for those who have switched—the question remains valid. Is the simplicity of the New Regime worth more than the potential savings of the Old Regime?

Here is the good news: For the Financial Year 2026-27, the government has maintained a status quo on tax slabs . However, the real game-changer lies in the fine print of the draft Income Tax Rules, 2026. Significant hikes in allowances like Hostel Expenditure and Children Education Allowance have quietly tilted the scales for some taxpayers, making the Old Regime suddenly more attractive again .

In this comprehensive guide, we cut through the confusion. We will compare the 2026 slab rates, analyze the impact of the new draft rules, and help you perform a “tax regime audit” to make the best decision for the upcoming financial year.

Key Takeaway: The choice isn’t just about how much you earn; it’s about how much you spend and invest. Let’s find out where you belong.

The 2026 Tax Slabs: A Side-by-Side Comparison

Before diving into complex calculations, you need to see the battlefield. Budget 2026 left the income tax slab structures untouched for both regimes, ensuring stability for the coming fiscal year . Here is how they stack up for a normal individual below 60 years of age.

New Tax Regime Slabs (FY 2026-27)

The government’s preferred choice offers lower rates but asks you to forego most exemptions and deductions.

| Income Slab (₹) | Tax Rate |

|---|---|

| Up to 4,00,000 | Nil |

| 4,00,001 to 8,00,000 | 5% |

| 8,00,001 to 12,00,000 | 10% |

| 12,00,001 to 16,00,000 | 15% |

| 16,00,001 to 20,00,000 | 20% |

| 20,00,001 to 24,00,000 | 25% |

| Above 24,00,000 | 30% |

Key Perk: The rebate under Section 87A ensures that if your taxable income is up to ₹12 lakh, your tax liability is zero . For salaried employees, the standard deduction of ₹75,000 pushes this effective tax-free limit to ₹12.75 lakh .

Old Tax Regime Slabs (FY 2026-27)

The traditional regime with higher rates, but a treasure trove of exemptions if you qualify.

| Income Slab (₹) | Tax Rate |

|---|---|

| Up to 2,50,000 | Nil |

| 2,50,001 to 5,00,000 | 5% |

| 5,00,001 to 10,00,000 | 20% |

| Above 10,00,000 | 30% |

Key Perk: You can claim HRA, LTA, Standard Deduction of ₹50,000, and deductions under Chapter VI-A (like 80C, 80D). The tax rebate under 87A is limited to incomes up to ₹5 lakh.

Beyond the Slabs: Why the 2026 Draft Rules Matter

You might look at the tables above and think the New Regime is a no-brainer. However, tax experts are buzzing about the draft Income Tax Rules, 2026. If finalized, these changes will breathe new life into the Old Regime for specific demographics .

The Allowance Hikes You Can’t Ignore

For years, allowances like Children Education Allowance were stuck at a paltry ₹100 per month—a figure completely detached from reality. The 2026 draft rules propose to fix this:

-

Children Education Allowance: Proposed to jump from ₹100 to ₹3,000 per month per child (max 2 children) .

-

Hostel Expenditure Allowance: Proposed to skyrocket from ₹300 to ₹9,000 per month per child (max 2 children) .

-

Food Meal Vouchers: Exemption limit increased from ₹50 to ₹200 per meal .

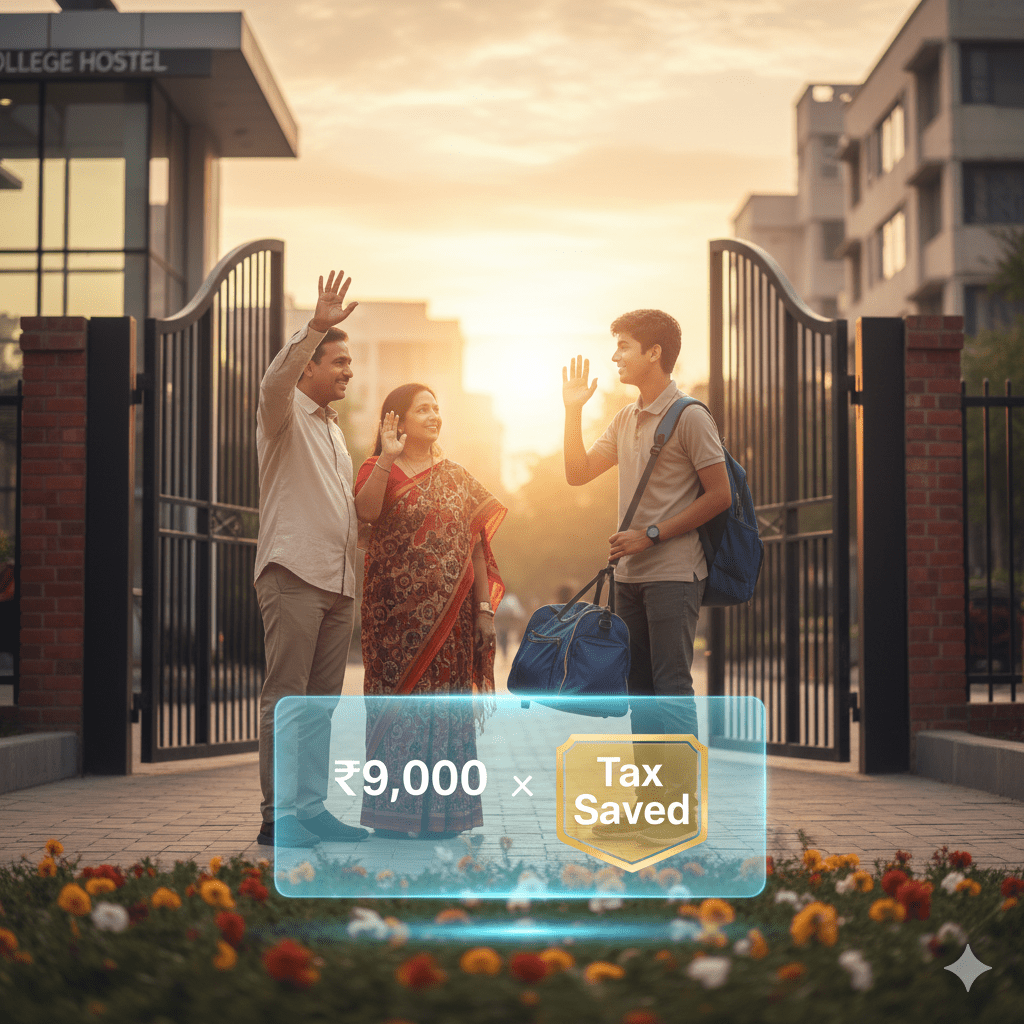

Real-World Impact:

Imagine a senior professional named Rajesh in Pune (a newly added city for 50% HRA eligibility) . He has two children studying in a hostel.

-

Old Calculation (Legacy): Total exemption from these specific allowances was barely ₹9,600 a year.

-

New Calculation (Proposed): Hostel Allowance (₹9,000 x 2 x 12) + Education Allowance (₹3,000 x 2 x 12) = ₹2,88,000 in tax-exempt allowances annually. Just from these two line items!

Add this to a higher HRA exemption (since Pune is now a metro for tax purposes) and Section 80C deductions, and the Old Regime suddenly looks like a powerhouse for Rajesh.

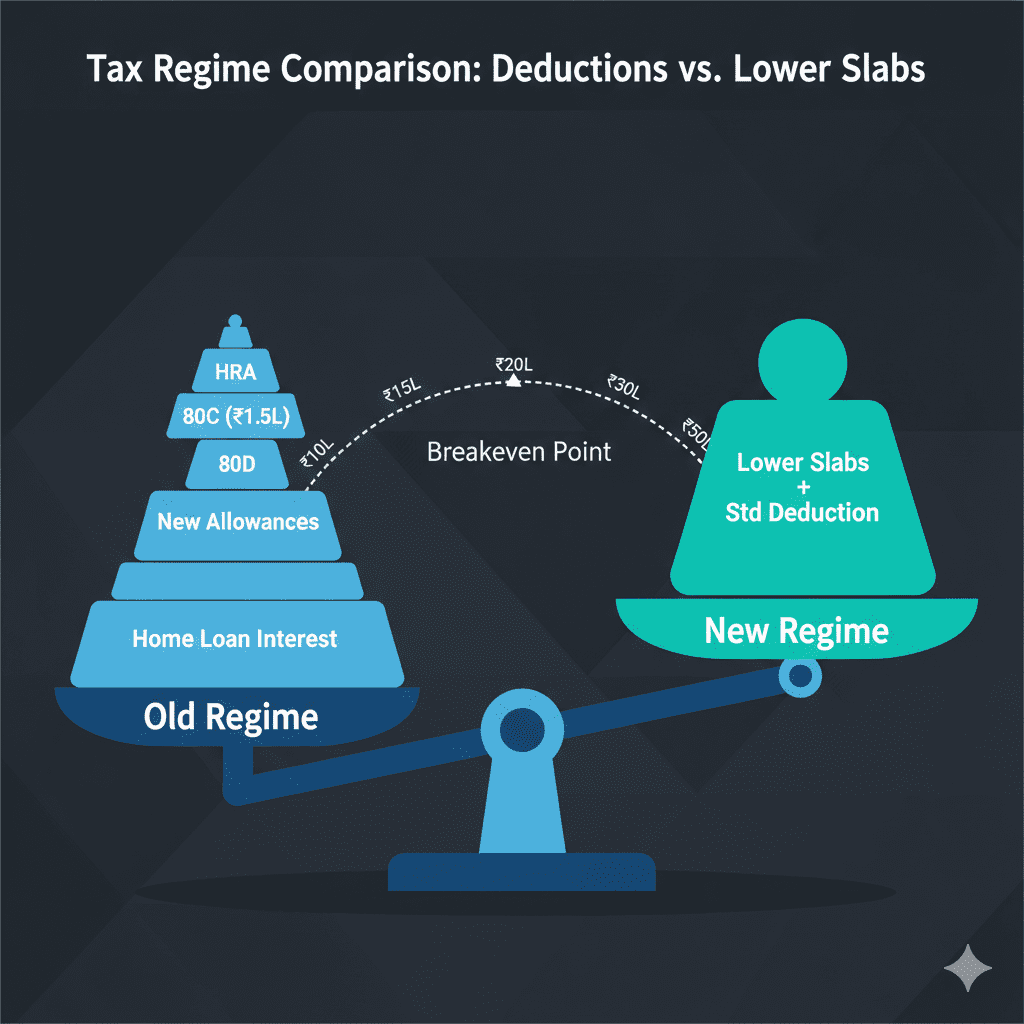

The Breakeven Point: How Much Deduction Do You Really Need?

The core of the “Old Tax Regime vs New Tax Regime” debate boils down to a simple number: your breakeven deduction. This is the minimum amount of deductions/exemptions you must claim in the Old Regime to have a tax liability lower than the New Regime.

According to recent analysis, the required deduction levels are significant :

-

For a salary of ₹15 Lakhs: You need deductions/exemptions of approx. ₹5.45 Lakhs.

-

For a salary of ₹20 Lakhs: You need approx. ₹7 Lakhs in deductions.

-

For a salary of ₹24 Lakhs and above: You need a whopping ₹8 Lakhs+ in deductions to beat the New Regime.

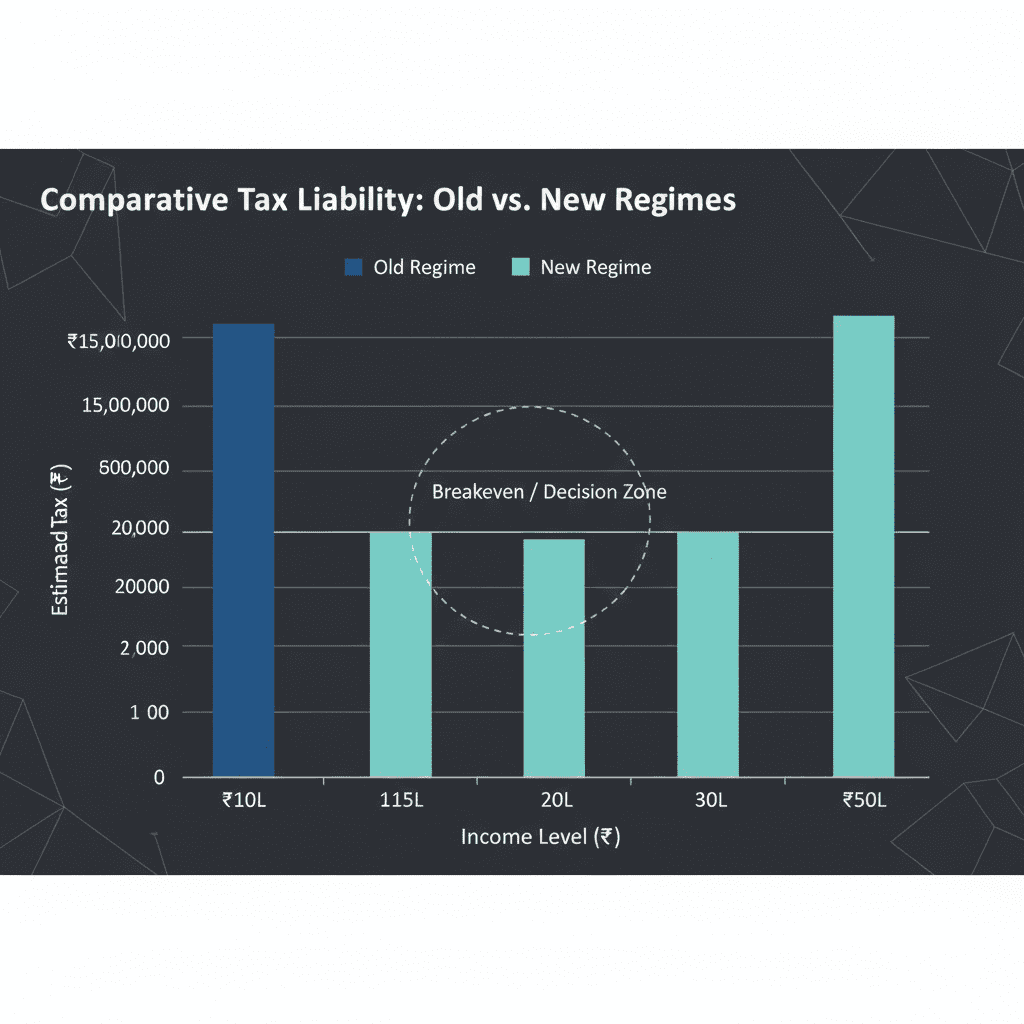

Old Tax Regime vs New Tax Regime: The Detailed Tax Calculator (2026-27)

Let’s get to the numbers. The table below compares tax liability (including cess) across different income levels. This assumes the taxpayer in the Old Regime can claim maximum deductions, including the newly proposed allowances where applicable, to meet the breakeven threshold.

| Gross Income (₹) | New Regime Tax (₹)* | Old Regime Tax (Max Savings) (₹)* | Which Regime Wins? |

|---|---|---|---|

| Up to 12.75 Lakhs | 0 | Varies (5,200 – 50,000+) | New Regime (Clear Winner) |

| 15 Lakhs | ~1,09,200 | ~1,20,000 (if deductions < 5.45L) | New Regime |

| 15 Lakhs | ~1,09,200 | ~90,000 (if deductions > 5.45L) | Old Regime |

| 20 Lakhs | ~2,08,000 | ~2,40,000 (if deductions < 7L) | New Regime |

| 20 Lakhs | ~2,08,000 | ~1,90,000 (if deductions > 7L) | Old Regime |

| 25 Lakhs | ~3,43,200 | ~3,70,000 (if deductions < 8L) | New Regime |

| 25 Lakhs | ~3,43,200 | ~3,10,000 (if deductions > 8L) | Old Regime |

| 1 Crore | ~29,51,519 | ~32,17,500 | New Regime (Wins by ~2.65 Lakhs) |

| *Tax amounts are approximate and include cess where applicable. Calculations assume standard deduction is claimed in the respective regimes . |

Analysis: The New Regime is the default winner for incomes up to ₹12.75 lakhs (thanks to the rebate) and again for very high incomes (over ₹50 lakhs) where the surcharge actually makes the New Regime slightly more efficient due to its different surcharge calculation base . The “grey area” is the middle-income bracket of ₹15 Lakhs to ₹25 Lakhs, where your financial discipline dictates the winner.

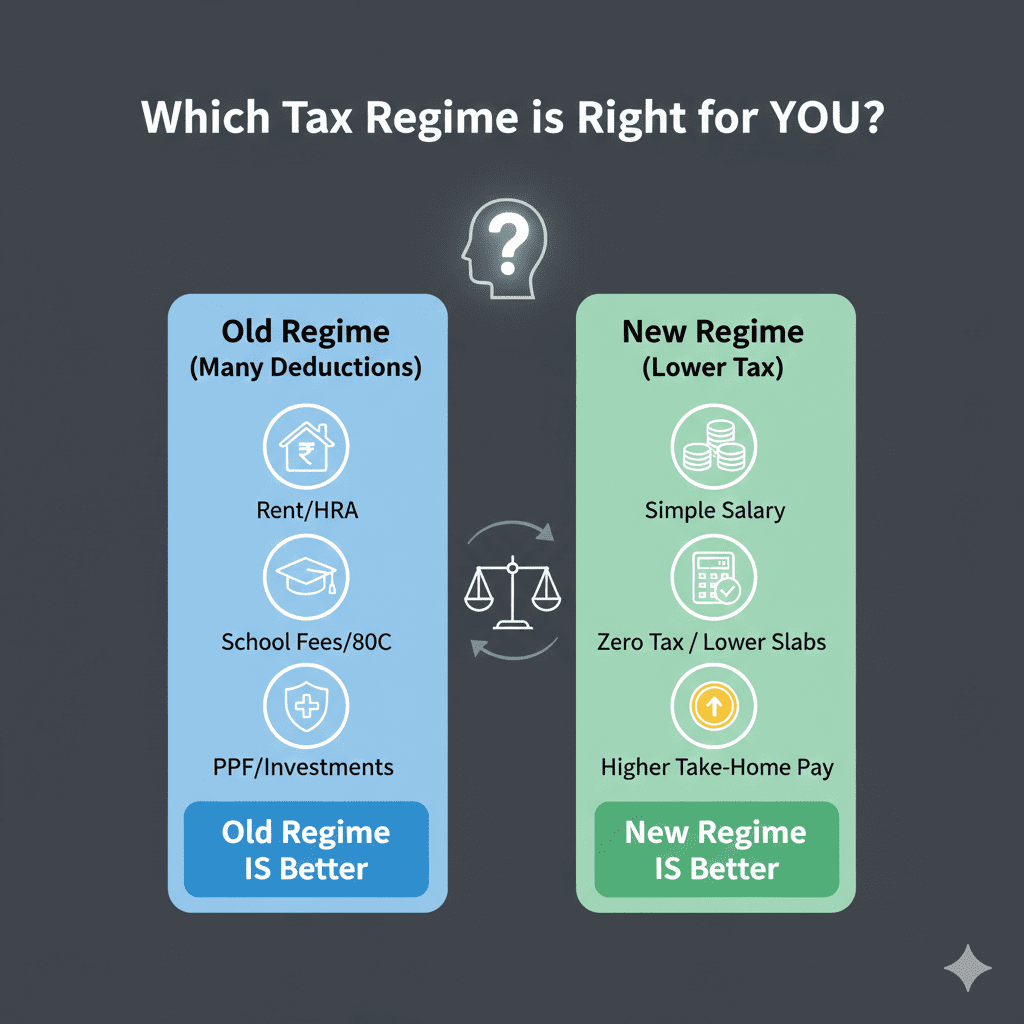

Who Should Choose Which Regime? (A 2026 Perspective)

Generic advice doesn’t work. Here is a breakdown based on who you are.

-

The Salaried Millennial (Income < ₹15 Lakhs):

-

Profile: Lives in a metro on rent, minimal investments beyond PF, spends on health insurance for parents.

-

Recommendation: New Regime. The zero-tax up to ₹12.75L is unbeatable. Trying to save ₹5.45L in deductions to beat the New Regime at a ₹15L salary is an uphill battle that often requires more investment than you can spare .

-

-

The Financially Prudent Parent (Income ₹15 Lakhs – ₹25 Lakhs):

-

Profile: Maximizing Section 80C (PPF, ELSS, Child Tuition), paying hefty school fees, has two children, pays a hefty HRA in a city like Pune or Bengaluru, and has a health insurance premium.

-

Recommendation: Old Regime. The revised allowance limits for hostel and education make a massive difference . If you can cross the ₹7-8 lakh deduction threshold, the Old Regime puts more cash back in your pocket.

-

-

The Homeowner with a Big Loan:

-

Profile: Paying ₹2 lakh+ annually in interest on a home loan, plus principal repayment under 80C.

-

Recommendation: Likely Old Regime. The combination of Section 24(b) (up to ₹2L for self-occupied property) and Section 80C (for principal) gives you a baseline deduction of ₹3.5L before you even add other items like insurance or NPS.

-

-

The High-Net-Worth Individual (Income > ₹50 Lakhs):

-

Profile: Income primarily from salary or business, but deductions are a drop in the ocean compared to total income.

-

Recommendation: New Regime. As the table shows, the tax saving in the New Regime at a ₹1 Crore income is nearly ₹2.65 Lakhs . The administrative ease of not having to prove your exemptions is a bonus.

-

Question to Ponder: Are you currently investing in tax-saving instruments because you need to save tax, or because they align with your long-term financial goals? If it’s the former, the New Regime might simplify your life.

Beyond Tax Rates: Key Compliance Changes in Budget 2026

While the slabs didn’t change, the process of paying tax did. These changes affect everyone, regardless of the regime you choose .

-

Revised Return Deadline Extended: You can now file a revised or belated return until 31st March of the following financial year (e.g., for FY 2026-27, you can file/revise until March 31, 2028). This gives you a massive 12-month window post the original due date to correct mistakes. However, a late fee will apply if filing after December 31st.

-

TCS Rationalized: Planning a foreign trip or education? Tax Collected at Source (TCS) on Liberalised Remittance Scheme (LRS) for education and medical purposes has been reduced to 2% , providing immediate cash flow relief .

-

New Income Tax Act from April 1, 2026: The new Act promises simpler language and fewer sections. Forms are being renumbered (Form 16 becomes Form 130), so be prepared for a new vocabulary when filing next year .

The Big Decision: How to Choose for FY 2026-27

Still confused? Here is a simple 3-step checklist to make your decision.

- Calculate Your “Old Regime” Benefits:

-

Add up HRA exemption (use an online HRA calculator).

-

Add up Section 80C investments (max ₹1.5 Lakhs).

-

Add up Section 80D health insurance premiums.

-

Add up Home Loan Interest (Section 24).

-

Add up the new allowance benefits (Education/Hostel/Food vouchers) if applicable .

-

Total =

A.

-

- Find Your Breakeven Point:

-

For your gross income level, refer to the breakeven numbers above (e.g., for ₹18L income, you need approx. ₹6.5L in deductions).

-

Target =

B.

-

- Compare and Decide:

-

-

If

Ais much greater thanB: Stick with the Old Regime. You are a power-saver. -

If

Ais much less thanB: Switch to the New Regime. Don’t force investments just to save tax. -

If

Ais roughly equal toB: Consider the “peace of mind” factor. The New Regime has zero compliance hassle. Choose New Regime for simplicity.

-

Conclusion

The battle of the Old Tax Regime vs New Tax Regime in 2026 is not a knockout; it’s a points decision. The New Regime remains the undisputed champion for simplicity and for those with incomes up to ₹12.75 lakhs. However, thanks to the proposed updates to decades-old allowance limits, the Old Regime has suddenly gained a second wind for families with specific spending patterns .

Don’t choose a regime based on what your friend chose. Do the math. Use the breakeven method outlined above. Remember, the best tax-saving strategy is the one that aligns with your actual life and financial goals, not the one that forces you to lock away money you need for a down payment or your child’s annual fees.

Your Next Step: Don’t wait for the HR deadline. Download our free “Tax Regime Selector Excel Sheet” below to input your exact numbers and get a personalized recommendation in under 5 minutes.

Frequently Asked Questions (FAQ)

Q1: Can I switch between regimes every year?

A: Yes, salaried individuals can switch between the Old and New Tax Regime every year. You need to inform your employer at the start of the financial year. However, if you have business income, the choice is more restrictive (usually a one-time opt-out per firm).

Q2: I heard the standard deduction is different in both regimes. What is the limit for 2026?

A: Yes, the standard deduction is ₹50,000 for the Old Tax Regime and ₹75,000 for the New Tax Regime . This is already factored into the tax calculations for salaried individuals.

Q3: Is the New Tax Regium really tax-free up to ₹12.75 lakhs?

A: For a salaried individual, yes. The basic exemption plus the rebate under Section 87A makes tax liability zero on taxable income up to ₹12 lakhs. Adding the standard deduction of ₹75,000 effectively means a salary income of up to ₹12.75 lakhs is tax-free .

Q4: Will the old tax regime be abolished soon?

A: While 88% of taxpayers have moved to the new regime, the government has confirmed there are no immediate plans to introduce a sunset clause for the old regime . It continues to coexist for those who can benefit from its exemptions.

Q5: What is the biggest change in the draft Income Tax Rules, 2026?

A: The most significant change for individual taxpayers is the massive increase in the exemption limits for Children Education Allowance (from ₹100 to ₹3,000 per month) and Hostel Expenditure Allowance (from ₹300 to ₹9,000 per month), making the Old Regime far more lucrative for parents .