Meet Priya, a 34-year-old senior software engineer in Pune earning ₹14.5 lakh annually. She received her salary hike letter this month and is wondering: “How much tax will I actually pay in FY 2026-27? And what’s this standard deduction everyone talks about?” Like millions of salaried Indians, Priya wants clarity—not confusing jargon.

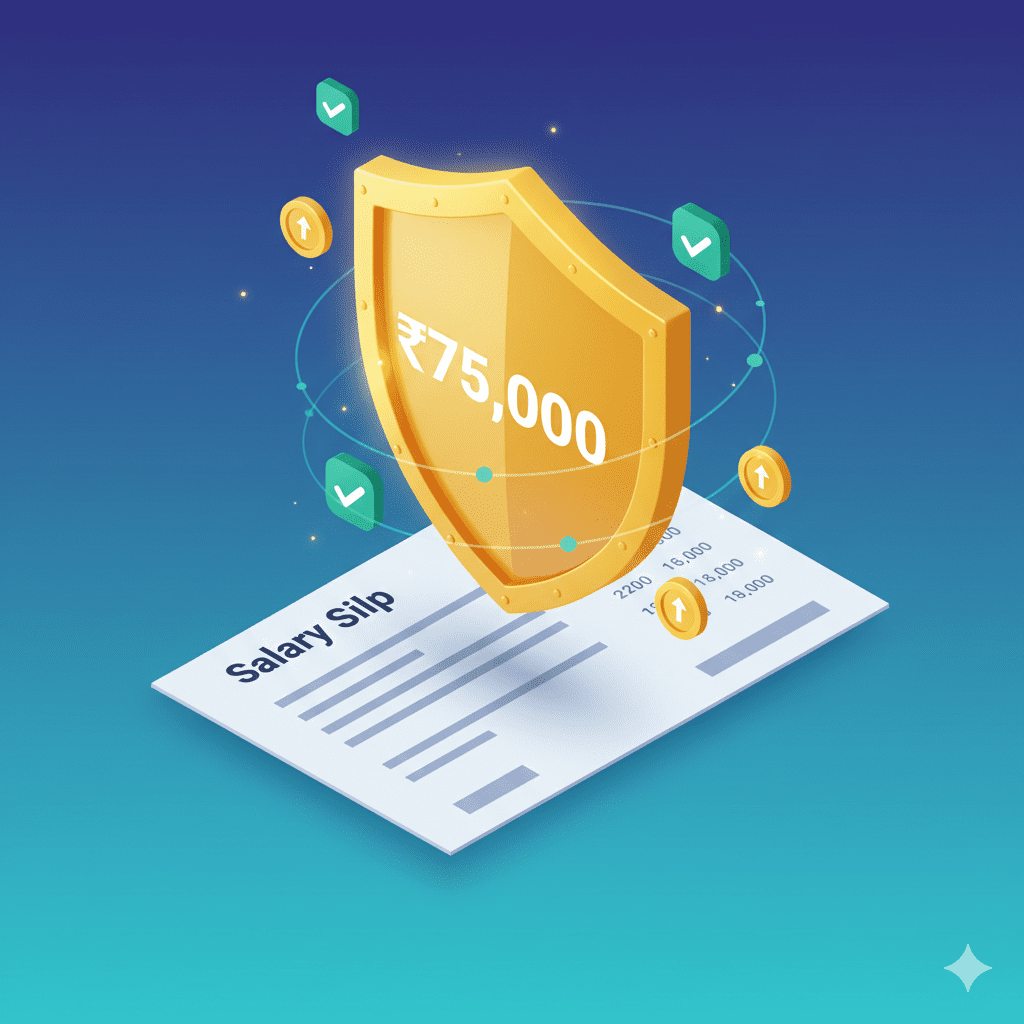

Here’s the good news. If your salary is up to ₹12.75 lakh in FY 2026-27, you will pay zero tax. Yes, zero. And if you earn more, the standard deduction of ₹75,000 is your best friend for reducing that tax bill .

The Union Budget 2026, presented by Finance Minister Nirmala Sitharaman, brought major reforms including a new Income Tax Act effective from April 1, 2026 . But here’s what surprised many: the standard deduction remained unchanged at ₹75,000 under the new tax regime and ₹50,000 under the old regime .

In this complete guide, you’ll learn:

-

Exactly how standard deduction works in 2026 (with real examples)

-

Who can claim it—and who cannot

-

The magic of ₹12.75 lakh zero-tax formula

-

Critical rules for pensioners and those with multiple employers

-

How to choose between old and new tax regimes

Let’s decode Standard Deduction 2026 together—no jargon, just practical clarity.

WHAT IS STANDARD DEDUCTION? THE ₹75,000 GIFT EXPLAINED

Standard deduction is essentially a “free gift” from the government to salaried employees and pensioners . It’s a fixed amount you can subtract from your total salary before calculating tax—without providing any bills, receipts, or investment proofs.

Think of it this way: If you earn ₹10 lakh, the tax department kindly ignores the first ₹75,000 of that income. You’re taxed only on the remaining ₹9.25 lakh.

Standard Deduction Limits for FY 2026-27

| Tax Regime | Standard Deduction Amount | Who Can Claim |

|---|---|---|

| New Tax Regime (Default) | ₹75,000 | Salaried employees & pensioners |

| Old Tax Regime | ₹50,000 | Salaried employees & pensioners |

Why Was Standard Deduction Introduced?

Before 2018, salaried employees could claim transport allowance (₹19,200) and medical reimbursement (₹15,000) separately—but this required submitting bills. The government simplified things by combining these into a single standard deduction of ₹40,000, later increased to ₹50,000, and then to ₹75,000 under the new regime in 2024 .

Key Insight: Standard deduction is not an “investment” benefit like Section 80C. You get it automatically—no ELSS, no PPF, no LIC premiums required. Just being salaried qualifies you.

STANDARD DEDUCTION 2026: THE OFFICIAL CONFIRMATION

Let’s address the question everyone’s asking: Did Budget 2026 increase standard deduction?

The short answer: No. Budget 2026 retained the existing limits .

According to multiple authoritative sources, including The Economic Times and Motilal Oswal, Finance Minister Nirmala Sitharaman announced several major reforms—including a new Income Tax Act from April 1, 2026—but standard deduction and income tax slabs remain unchanged for FY 2026-27 .

Why No Increase? Expert Insights

Tax experts suggest the government prefers stability. Deloitte India’s Sudhakar Sethuraman explains: “Standard deduction was recently enhanced to ₹75,000 in Finance Act, 2024. Given stable inflation and the policy intent of keeping the new regime simple and predictable, the Government may prefer stability in the near term” .

Neeraj Agarwala of Nangia & Co LLP adds another perspective: “Tax laws are framed uniformly for the country and do not provide for deductions based on geographic location. While living costs are higher in metropolitan cities, they remain lower in many regions. A revision solely for urban costs is unlikely” .

Was an Increase Expected?

Yes—many taxpayers hoped for a hike to ₹1,00,000 . An increase of ₹25,000 would have saved up to ₹7,500–₹10,000 annually depending on the tax slab. However, the government prioritized other reforms like:

-

Reduced TCS on overseas tour packages (now flat 2%)

-

Extended revised ITR deadline to March 31

-

New foreign asset disclosure scheme for small taxpayers

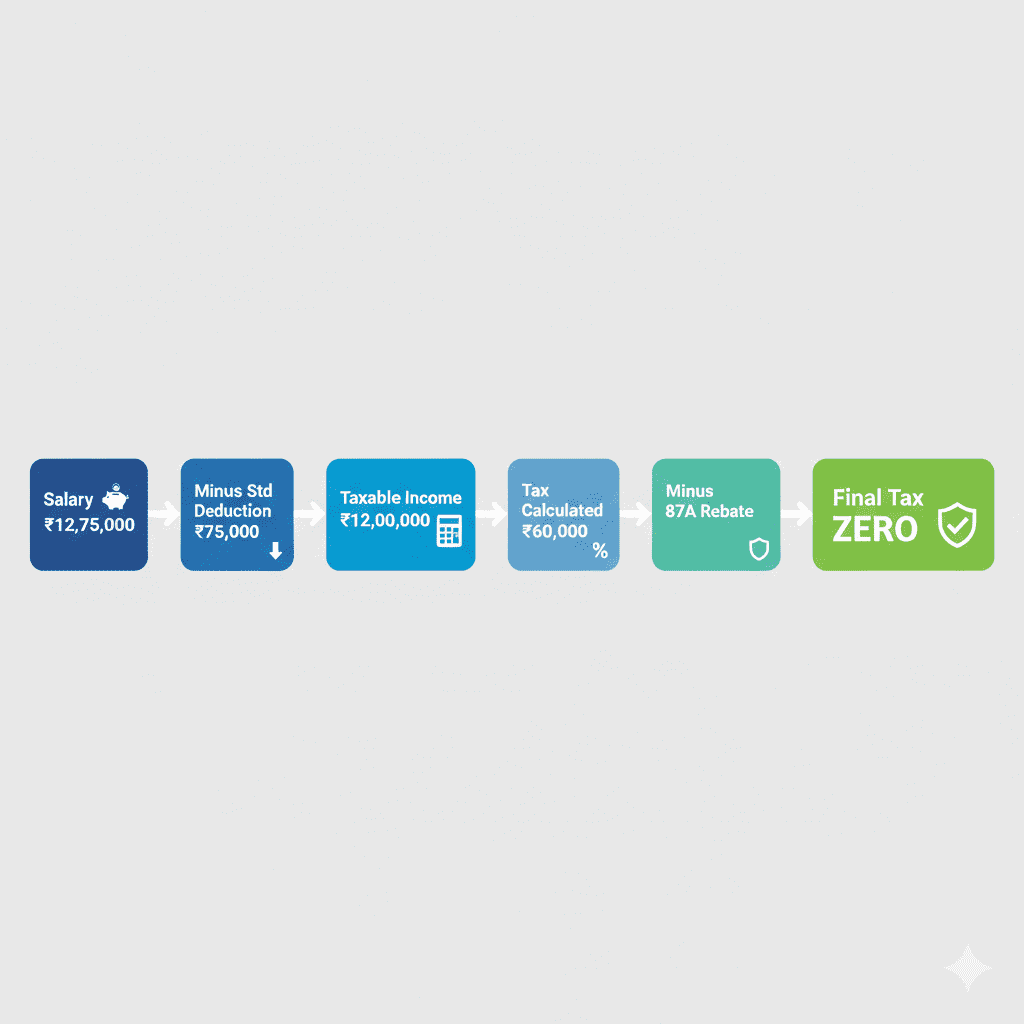

THE MAGIC OF ₹12.75 LAKH: HOW STANDARD DEDUCTION CREATES ZERO TAX

This is the most exciting part for middle-class taxpayers. Under the new tax regime, if your total salary is up to ₹12.75 lakh, you pay ZERO income tax .

Here’s the math:

The Zero-Tax Formula

| Component | Amount |

|---|---|

| Your Annual Salary | ₹12,75,000 |

| Less: Standard Deduction | (₹75,000) |

| Taxable Income | ₹12,00,000 |

| Tax Payable (as per slabs) | ₹60,000 |

| Less: Section 87A Rebate | (₹60,000) |

| Final Tax | ₹0 |

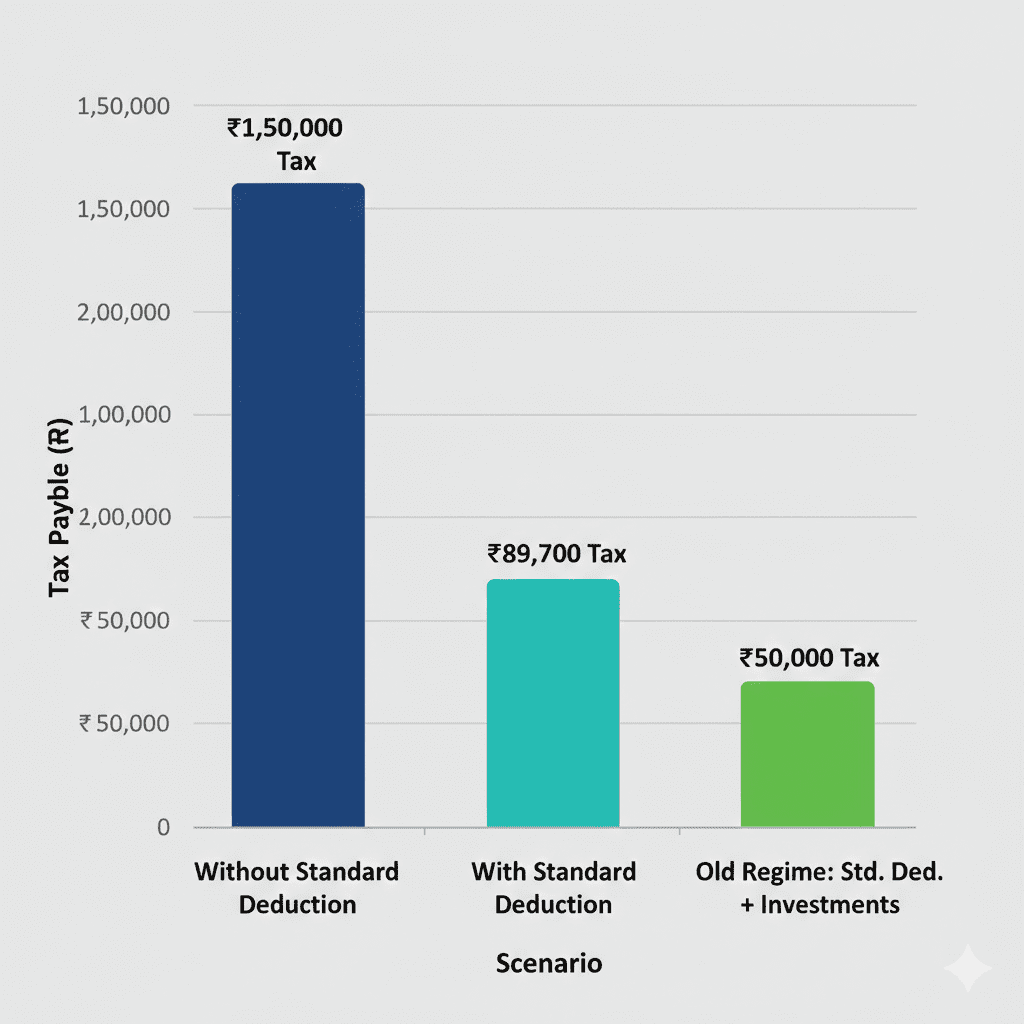

Real-Life Example: Priya’s Tax Calculation

Remember Priya, our software engineer earning ₹14.5 lakh? Let’s calculate her actual tax:

Scenario A: New Tax Regime (Default)

| Salary & Deductions | Amount |

|---|---|

| Annual Salary | ₹14,50,000 |

| Less: Standard Deduction | (₹75,000) |

| Taxable Income | ₹13,75,000 |

Tax Calculation:

-

Up to ₹4,00,000: Nil

-

₹4,00,001–₹8,00,000 (₹4,00,000 @ 5%): ₹20,000

-

₹8,00,001–₹12,00,000 (₹4,00,000 @ 10%): ₹40,000

-

₹12,00,001–₹13,75,000 (₹1,75,000 @ 15%): ₹26,250

-

Total Tax: ₹86,250

-

Less: Rebate under 87A? Not eligible (income exceeds ₹12 lakh)

-

Tax Payable: ₹86,250 + 4% cess ≈ ₹89,700

Key Takeaway: Priya’s effective tax rate is just about 6.2% on her ₹14.5 lakh salary—thanks to the ₹75,000 standard deduction and the new regime’s lower rates.

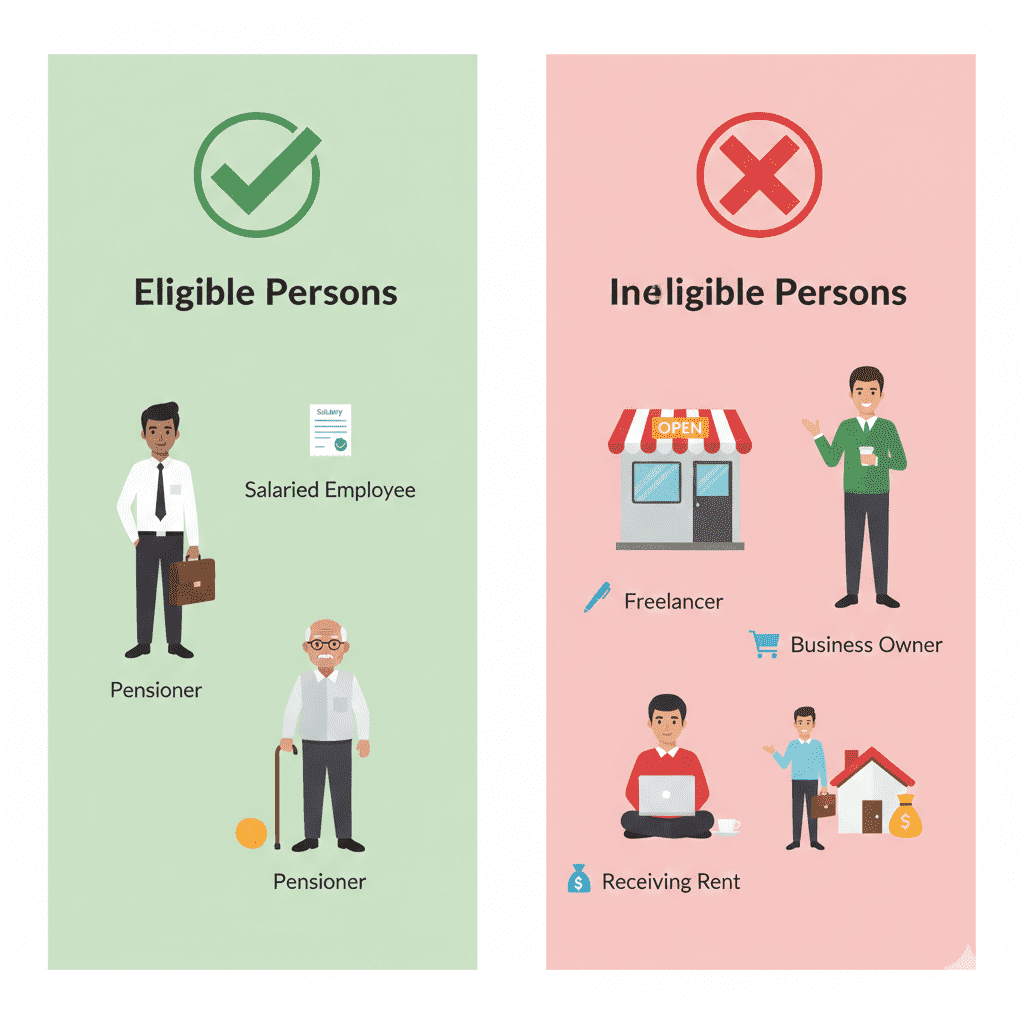

WHO CAN CLAIM STANDARD DEDUCTION? ELIGIBILITY RULES

Not everyone can claim this benefit. Here’s the complete eligibility breakdown:

✅ Eligible: Salaried Employees & Pensioners

According to Chartered Accountant Abhishek Soni, co-founder of Tax2Win: “The standard deduction can be claimed by individuals receiving salary and pension. Section 16 of the Income Tax Act provides relief to pensioners by allowing them to claim a standard deduction of up to ₹50,000/₹75,000 per annum or the actual amount of the pension, whichever is less” .

Pensioners: Even if you’re a senior citizen receiving pension from your former employer, this income is treated as “salaries” for tax purposes. You’re fully eligible for standard deduction .

❌ Not Eligible:

| Category | Reason |

|---|---|

| Freelancers | Income from business/profession, not salary |

| Business Owners | No salary income |

| Property Rent Earners | Rental income is under “House Property” head |

| Capital Gains Investors | Investment income, not salary |

| Interest Income Recipients | Savings/FD interest under “Other Sources” |

Special Case: Multiple Employers

If you changed jobs during the year and received salary from two employers, can you claim standard deduction twice?

No. Standard deduction is taxpayer-specific, not employer-specific. Chartered Accountant Suresh Surana clarifies: “Even if salary is received from more than one employer, the deduction is restricted to ₹75,000 under the new regime or ₹50,000 under the old regime for the entire year” .

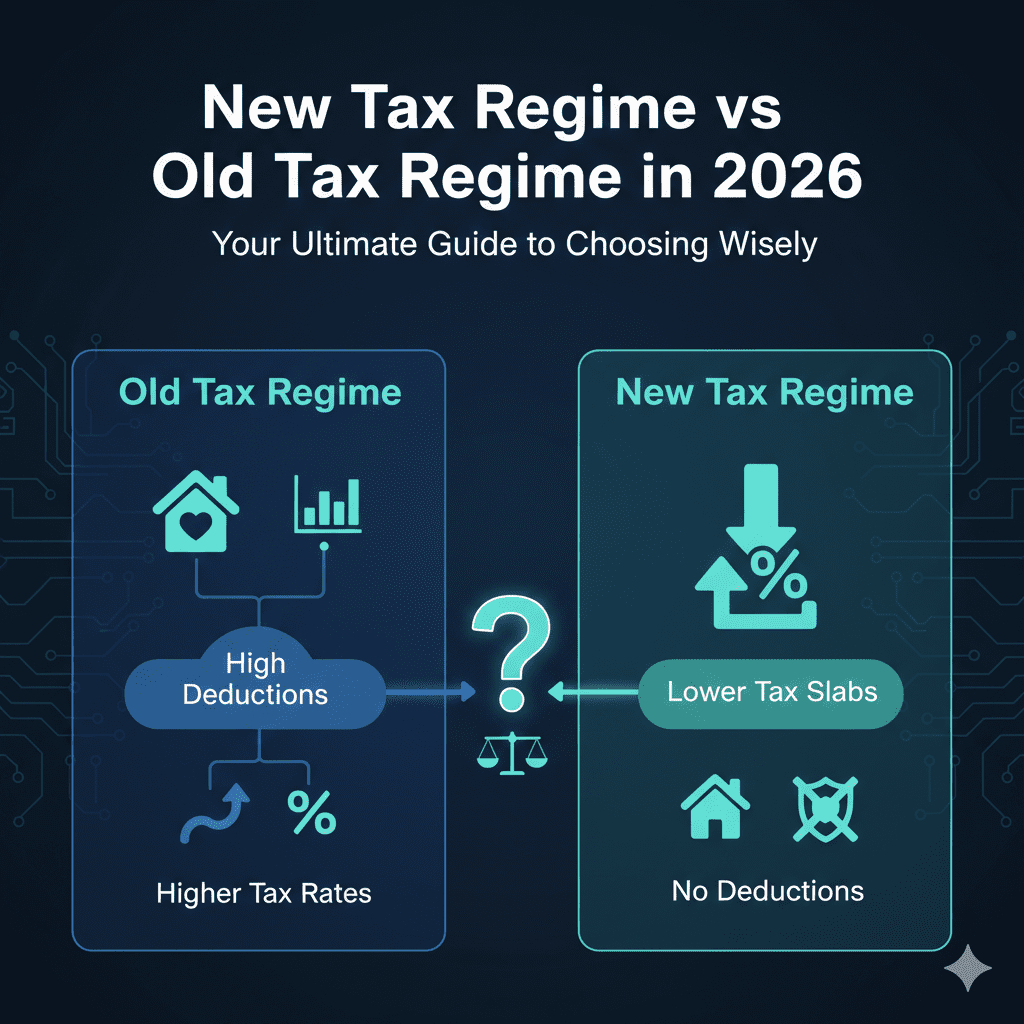

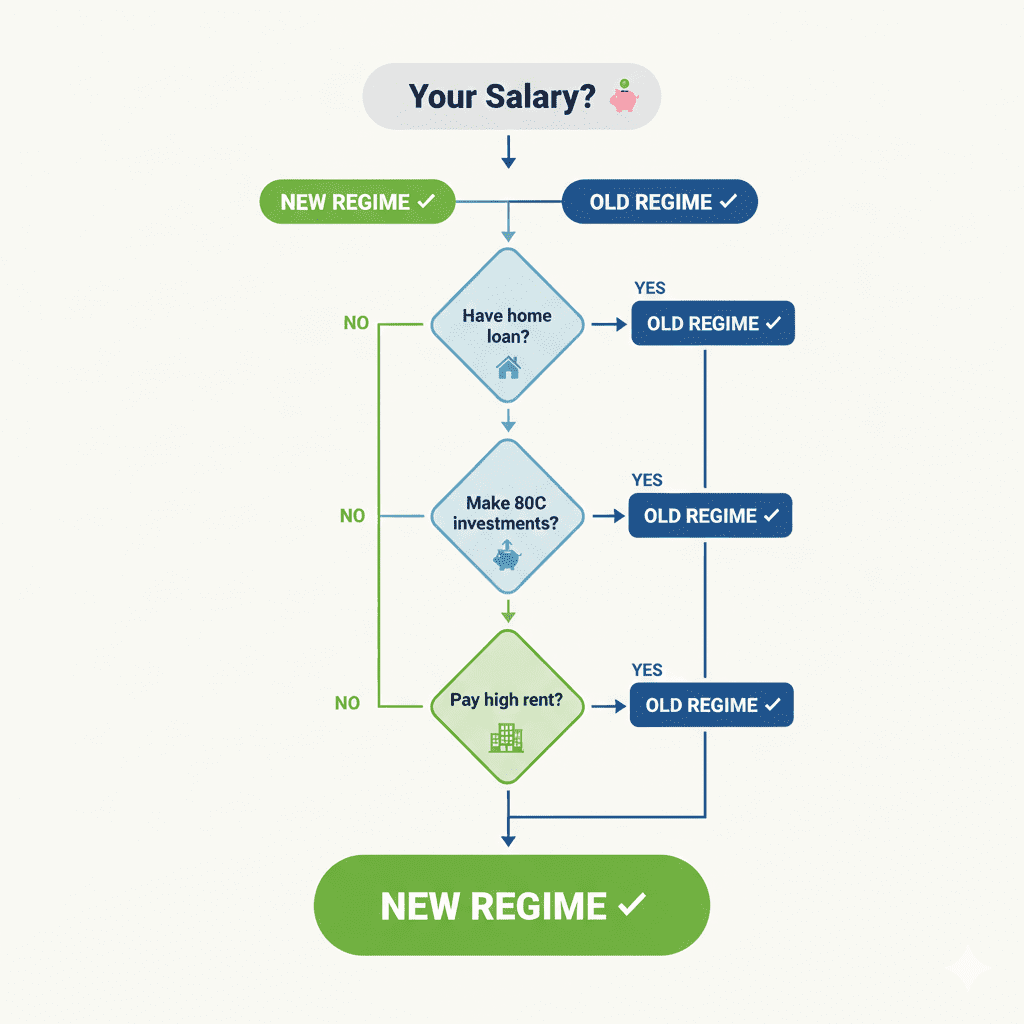

NEW TAX REGIME VS OLD TAX REGIME: WHICH IS BETTER IN 2026?

With standard deduction of ₹75,000 in the new regime versus ₹50,000 in the old regime, which one should you choose?

Side-by-Side Comparison

| Feature | New Tax Regime | Old Tax Regime |

|---|---|---|

| Standard Deduction | ₹75,000 | ₹50,000 |

| Tax Slabs | Lower rates (0-30%) | Higher rates (0-30%) |

| Section 80C Deduction | Not available | Up to ₹1.5 lakh |

| HRA Exemption | Not available | Available |

| Home Loan Interest | Not available | Up to ₹2 lakh |

| 80D (Health Insurance) | Not available | Up to ₹25,000/₹50,000 |

| Default Option? | Yes, automatic | Must opt-in |

Decision Matrix: Which Regime Saves You More?

| Your Situation | Likely Better Regime |

|---|---|

| No home loan, minimal investments | New Regime (lower rates + higher standard deduction) |

| Large home loan (₹2 lakh+ interest) | Old Regime (claim interest deduction) |

| High HRA with rent payments | Old Regime (HRA exemption) |

| Significant 80C investments (PPF, ELSS, LIC) | Old Regime (claim all deductions) |

| Income under ₹12.75 lakh | New Regime (zero tax with standard deduction) |

| Senior citizen with medical needs | Old Regime (higher 80D limits + senior benefits) |

Can You Switch Every Year?

Yes—if you’re a salaried employee. You can choose whichever regime is cheaper each year when filing your return. However, business owners and professionals have restrictions .

HOW STANDARD DEDUCTION WORKS WITH OTHER TAX BENEFITS

Interaction with Section 87A Rebate

The ₹12.75 lakh zero-tax benefit combines standard deduction with Section 87A rebate. Here’s how:

-

Standard deduction reduces your salary to taxable income

-

If taxable income ≤ ₹12 lakh, Section 87A rebate eliminates all tax

-

Result: Salary up to ₹12.75 lakh = zero tax

Marginal Relief Explained

What if you earn ₹12.80 lakh—just ₹5,000 above the threshold?

A rule called Marginal Relief ensures you don’t pay more tax than the extra income you earned. You’ll pay only a small amount, not the full slab rate .

New Tax Regime Slabs for FY 2026-27

| Taxable Income | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Source: Budget 2026 announcements

COMMON MISTAKES TO AVOID WITH STANDARD DEDUCTION

Mistake 1: Claiming Standard Deduction Twice

As discussed, if you had multiple employers, you can claim standard deduction only once in your ITR. Your Form 16 from each employer might show the deduction, but when combining incomes, ensure you don’t double-count.

Mistake 2: Assuming It’s Automatic in Old Regime

Under the new regime, standard deduction is indeed automatic. But in the old regime, you must explicitly claim it while filing. Some taxpayers forget and end up overpaying tax.

Mistake 3: Pensioners Not Claiming It

Many pensioners assume standard deduction is only for current employees. Wrong. If you receive pension, you’re eligible. Claim it .

Mistake 4: Freelancers Trying to Claim It

If you’re a freelancer or professional with business income, standard deduction is not available—even if you have a salary component. The deduction applies only to income taxed under the “Salaries” head.

Mistake 5: Not Re-evaluating Regime Choice Annually

Your financial situation changes. Maybe this year you took a home loan, or perhaps your investments decreased. Re-evaluate old vs new regime every year—don’t assume last year’s choice is still optimal.

FREQUENTLY ASKED QUESTIONS

Q1: Is standard deduction increased in Budget 2026?

No. The standard deduction remains at ₹75,000 under the new tax regime and ₹50,000 under the old regime for FY 2026-27. Budget 2026 focused on other reforms like a new Income Tax Act, reduced TCS rates, and extended ITR deadlines .

Q2: I earn ₹10 lakh. How much tax do I actually pay?

Zero rupees. Here’s why: ₹10,00,000 salary minus ₹75,000 standard deduction = ₹9,25,000 taxable income. Since this is below ₹12 lakh, you get full Section 87A rebate. Your tax liability is completely eliminated .

Q3: I’m a pensioner. Can I claim standard deduction?

Absolutely. Pension received from your former employer is treated as “salaries” under the Income Tax Act. You can claim standard deduction of up to ₹75,000 (new regime) or ₹50,000 (old regime), or the actual pension amount—whichever is lower .

Q4: I changed jobs twice this year. Can I claim standard deduction from each employer?

No. Standard deduction is allowed only once per taxpayer per financial year, regardless of how many employers you had. When combining salaries from multiple Form 16s, ensure you claim only one standard deduction .

Q5: Which tax regime is better for me—old or new?

It depends on your deductions. New regime is better if you have minimal investments and no home loan (plus you get ₹75,000 standard deduction). Old regime may be better if you have significant 80C investments, HRA, or home loan interest. Use the decision tree above to decide .

Q6: Is standard deduction available to freelancers or professionals?

No. Standard deduction is specifically for income taxed under the head “Salaries.” Freelancers, professionals, and business owners cannot claim it, even if they have high business income .

Q7: Does standard deduction apply to family pension received by nominees?

Special rule: Family pension received by nominees after the pensioner’s death is taxable under “Income from Other Sources,” not “Salaries.” For family pension, a separate deduction is available under Section 57(iia)—33⅓% of the pension or ₹15,000, whichever is less. This is different from standard deduction.

Q8: Will standard deduction increase in future budgets?

Possibly. Tax experts note strong demand to raise it to ₹1,00,000 to reflect inflation and rising living costs . However, the government currently prioritizes stability and predictability in the new tax regime framework .

ACTIONABLE CHECKLIST: OPTIMIZE YOUR STANDARD DEDUCTION BENEFIT

Before March 31, 2026 (End of Financial Year)

-

Confirm your eligibility: If you’re salaried or a pensioner, you qualify

-

Estimate total salary: Include all employers if you switched jobs

-

Calculate tax under both regimes: Use online calculator with ₹75,000 standard deduction

-

If choosing old regime: Ensure you have investment proofs ready (80C, 80D, HRA)

-

If choosing new regime: Enjoy the higher standard deduction with zero paperwork

During ITR Filing (July 2026 onwards)

-

Download Form 16: Verify standard deduction is correctly shown

-

Check Form 26AS: Ensure no TDS mismatches

-

Select regime wisely: New regime is default; opt for old only if beneficial

-

Claim standard deduction once: Even with multiple Form 16s

-

Verify zero-tax eligibility: If salary ≤ ₹12.75L, ensure rebate applied

Year-Round Strategy

-

Re-evaluate annually: Your financial situation changes—so should your regime choice

-

Plan investments based on regime: Don’t lock into 80C if new regime suits you better

-

For pensioners: Always claim standard deduction—it’s automatic but verify

CONCLUSION: YOUR ₹75,000 TAX SAVING PARTNER

Standard deduction 2026 remains one of the simplest and most valuable tax benefits for salaried employees and pensioners. At ₹75,000 under the new tax regime, it directly reduces your taxable income without any paperwork, investments, or proof submission.

The best part? Combined with the Section 87A rebate, it creates a zero-tax zone up to ₹12.75 lakh—putting real money back in your pocket .

While Budget 2026 didn’t increase the limit, it brought something perhaps more valuable: certainty and stability. The new Income Tax Act from April 1, 2026 promises simpler rules, clearer forms, and easier compliance . And with standard deduction firmly in place, you can plan your finances with confidence.

Your Next Steps

- Calculate your tax using the ₹75,000 standard deduction

- Decide between old and new regimes based on your home loan, investments, and rent

- If earning under ₹12.75 lakh, celebrate—you’re in the zero-tax club

- Share this guide with colleagues who still find tax confusing

Remember: Standard deduction isn’t just a number on a form. It’s ₹75,000 of your hard-earned money that the government kindly ignores. Use it wisely.

“Standard deduction is the government’s gift to salaried employees—₹75,000 of your income that simply disappears from the taxman’s view. No receipts. No proofs. Just pure tax savings.”

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice. Tax laws are subject to change, and individual situations vary. Please consult a qualified Chartered Accountant for advice tailored to your specific circumstances. The information provided is based on Budget 2026 announcements and current tax provisions as of February 2026.