Meet Priya, a freelance graphic designer in Bangalore who just crossed ₹12 lakh in annual income. She’s been so focused on delivering projects that she hasn’t thought about taxes. Now, with a tax notice looming, she’s panicking. Then there’s Rajesh, a management consultant in Mumbai earning ₹45 lakh annually. He pays a CA but wonders if he’s missing deductions that could save him lakhs.

If you’re a freelancer or consultant, tax planning is different from salaried employees. You don’t have an employer deducting TDS and giving Form 16. You’re responsible for everything—tracking income, claiming expenses, paying advance tax, and filing returns.

The good news? The tax laws actually favor freelancers in many ways. You can claim deductions that salaried people can’t. With proper planning, you can legally reduce your tax by 30-40% .

In this 2026 guide, you’ll discover:

-

Presumptive taxation under Section 44ADA – the freelancer’s best friend

-

Expenses you can claim (even things you didn’t know)

-

GST registration and compliance for freelancers

-

TDS on professional fees – how to handle it

-

Tax-saving investments (80C, 80D, NPS)

-

Advance tax due dates and how to calculate

-

Common mistakes that trigger notices

-

Free tools to calculate your tax and track expenses

Let’s turn your freelance income into tax-smart wealth.

SECTION 44ADA: THE FREELANCER’S SUPERPOWER

If you’re a freelancer or consultant, Section 44ADA is the most important tax provision you need to know.

What is Section 44ADA?

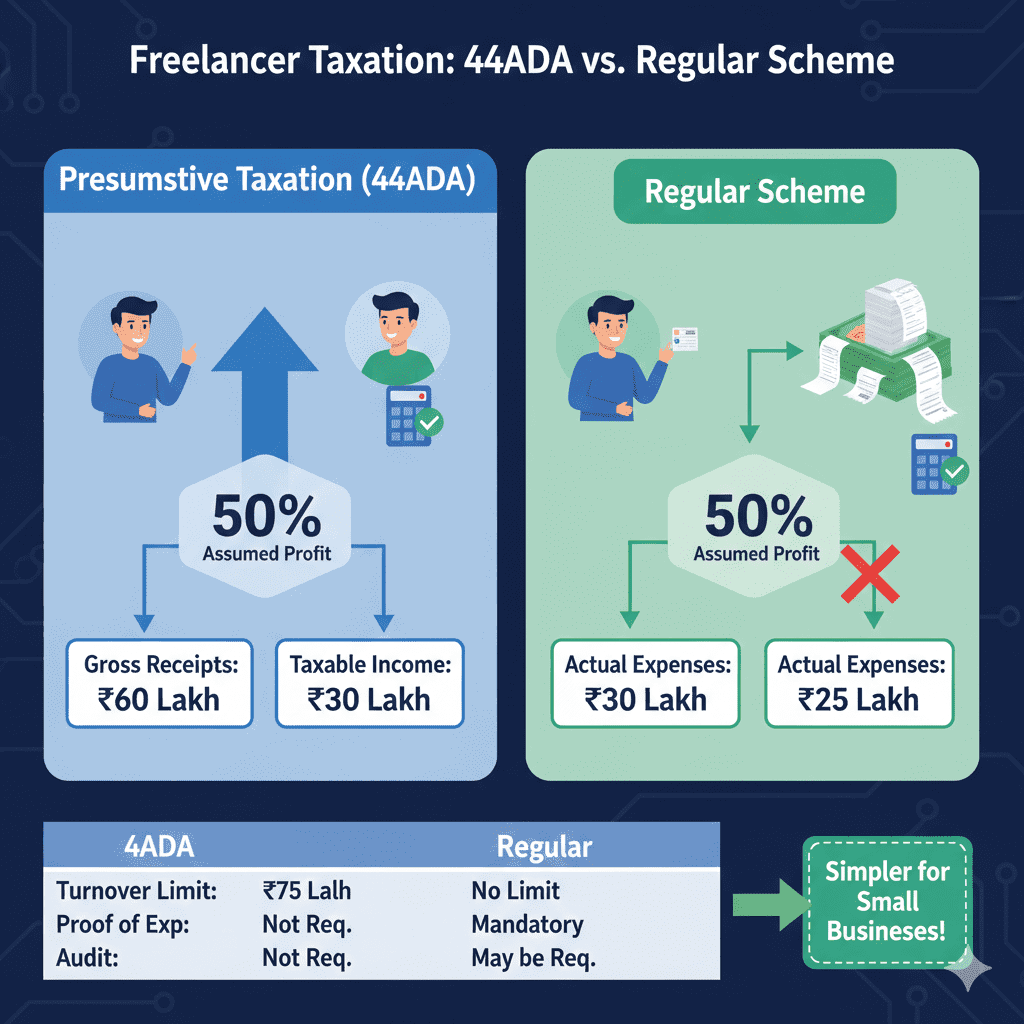

Section 44ADA is a presumptive taxation scheme for specified professionals. Instead of maintaining detailed books and getting accounts audited, you can declare 50% of your gross receipts as profit.

| Feature | Details |

|---|---|

| Who qualifies | Professionals in specified fields (legal, medical, engineering, architecture, accountancy, interior decoration, technical consultancy, etc.) |

| Eligibility limit | Gross receipts up to ₹75 lakh |

| Presumed profit | 50% of gross receipts |

| Audit required? | No (if profit declared at 50% or more) |

| Books required? | No (simplified) |

*Source: Income Tax Act, Section 44ADA, as amended by Finance Act 2026 *

How It Works

Example: Priya, freelance graphic designer, has gross receipts of ₹60 lakh.

| Calculation | Amount |

|---|---|

| Gross receipts | ₹60,00,000 |

| Presumed profit (50%) | ₹30,00,000 |

| Tax on ₹30 lakh (old regime, after deductions) | ~₹6.2 lakh |

| Tax without presumptive (if actual profit 40%) | ~₹7.8 lakh + audit cost |

Savings: ₹1.6 lakh + audit fees

When NOT to Use Section 44ADA

| Situation | Better to Use Regular Scheme |

|---|---|

| Actual profit less than 50% | Claim lower profit with audit |

| Have business losses to carry forward | Need books to track losses |

| Need loans (banks prefer audited books) | Regular books help |

| Gross receipts > ₹75 lakh | Not eligible for presumptive |

Key Points to Remember

- No deduction for expenses – The 50% profit rate is deemed to cover all expenses

- Can still claim 80C, 80D – Those are separate from business income

- Must file ITR-4 (not ITR-3)

- Can opt out any year, but then can’t re-enter for 5 years

EXPENSES YOU CAN CLAIM (IF NOT UNDER 44ADA)

If you don’t opt for presumptive taxation, you can claim actual business expenses. This is beneficial if your actual profit is less than 50% of receipts.

Allowable Business Expenses

| Expense Category | Examples | Documentation Needed |

|---|---|---|

| Office rent | Co-working space, home office portion | Rent agreement, receipts |

| Equipment | Laptop, computer, printer, phone | Invoices, proof of payment |

| Software/subscriptions | Design software, CRM, cloud storage | Subscription receipts |

| Internet/phone | Monthly bills (business portion) | Bills in business name |

| Travel | Client meetings, conferences, site visits | Tickets, hotel bills |

| Meals/entertainment | Client meals (reasonable) | Bills with client name |

| Professional fees | CA fees, legal expenses | Invoices, receipts |

| Marketing | Website, ads, business cards, portfolio | Invoices, payment proof |

| Insurance | Professional indemnity, health insurance | Policy documents |

| Depreciation | On assets like laptop, furniture | Calculate as per IT rules |

| Education/training | Courses, workshops, books related to work | Receipts, certificates |

What NOT to Claim

| Expense | Reason |

|---|---|

| Personal expenses | Not business-related |

| Family members’ expenses | Unless genuinely employed |

| Capital expenses (fully) | Claim depreciation instead |

| Expenses without bills | No proof = disallowed |

Home Office Deduction

If you work from home, you can claim a portion of:

| Expense | How to Calculate |

|---|---|

| Rent | % of house area used exclusively for business |

| Electricity | Proportionate to business area |

| Internet | Reasonable business portion |

| Maintenance | Society charges, repairs (proportionate) |

Example: 2 rooms of a 4-room house used exclusively for work → claim 50% of eligible expenses.

GST FOR FREELANCERS AND CONSULTANTS

When is GST Registration Mandatory?

| Situation | GST Required? |

|---|---|

| Annual turnover > ₹20 lakh (services) | Yes |

| Annual turnover > ₹10 lakh (special category states) | Yes |

| Inter-state services | Yes (regardless of turnover) |

| Selling on e-commerce platforms | Yes |

| Voluntary registration | Optional (can be beneficial) |

*Source: CGST Act, 2017 *

GST Rates for Freelancers

| Type of Service | GST Rate |

|---|---|

| Most professional services (consulting, design, IT, legal, accounting) | 18% |

| Some specified services (like training, coaching) | 18% |

| Exports | 0% (with ITC refund) |

GST Compliance for Freelancers

| Requirement | Frequency | Due Date |

|---|---|---|

| GSTR-1 (outward supplies) | Monthly/Quarterly | 11th/13th of next month |

| GSTR-3B (return + payment) | Monthly/Quarterly | 20th/22nd/24th of next month |

| GSTR-9 (annual return) | Annually | 31st December |

Composition Scheme for Freelancers?

Not available for service providers. Composition scheme is only for goods suppliers and restaurants.

GST on Exports

If you serve clients outside India:

-

Export of services is zero-rated (no GST)

-

You can claim refund of Input Tax Credit (GST paid on expenses)

-

Must have proper documentation (export of services declaration)

Common GST Mistakes

| Mistake | Consequence |

|---|---|

| Not registering when turnover exceeds limit | Penalty of 10% of tax or ₹10,000 |

| Charging GST but not filing returns | Interest, late fees, suspension |

| Wrong SAC code | Wrong rate, notices |

| Not issuing proper invoices | ITC denied to client |

| Missing TDS on rent/contractor payments | Disallowance under Section 40(a)(ia) |

TDS ON PROFESSIONAL FEES

When is TDS Deducted?

| Payer Type | TDS Section | Rate (2026) |

|---|---|---|

| Companies/Partnerships paying fees to you | 194J | 10% |

| Individuals/HUF (if audit required) | 194J | 10% |

| Government departments | 194J | 10% |

| Payment for technical services | 194J | 10% |

What to Do When TDS is Deducted

| Step | Action |

|---|---|

| 1 | Provide your PAN to payer |

| 2 | Ensure TDS is deposited (check Form 26AS) |

| 3 | Include TDS amount in your income |

| 4 | Claim credit while filing ITR |

If TDS is Not Deducted

| Situation | What Happens |

|---|---|

| Payer was supposed to deduct but didn’t | You must still pay tax (advance tax/self-assessment) |

| Payer faces penalty | Not your concern, but coordinate for certificate |

TDS on Your Own Payments

As a freelancer, you may need to deduct TDS when you pay:

| Payment To | Section | Rate | Threshold |

|---|---|---|---|

| Contractors (for work) | 194C | 1-2% | ₹30,000 per invoice / ₹1,00,000 annually |

| Rent (if > ₹2.4L/year) | 194I | 10% | ₹2,40,000 annually |

| Professional fees (to another freelancer) | 194J | 10% | ₹30,000 per invoice |

TAX-SAVING INVESTMENTS FOR FREELANCERS

Even as a freelancer, you can claim deductions under Chapter VI-A.

Section 80C: Up to ₹1.5 Lakh

| Investment | Lock-in | Suitable For |

|---|---|---|

| PPF (Public Provident Fund) | 15 years | Long-term safety |

| ELSS (Equity Linked Savings Scheme) | 3 years | Higher returns |

| Life Insurance Premium | Policy term | Insurance + savings |

| NSC (National Savings Certificate) | 5 years | Guaranteed returns |

| Tax-saving FD | 5 years | Risk-free |

| Sukanya Samriddhi Yojana | 21 years | Girl child benefit |

Section 80D: Health Insurance

| Who | Maximum Deduction |

|---|---|

| Self + family | ₹25,000 |

| Parents (below 60) | ₹25,000 |

| Parents (above 60) | ₹50,000 |

| Total possible | ₹75,000 |

Section 80CCD(1B): NPS Additional

-

Extra ₹50,000 deduction for investing in National Pension System

-

Over and above 80C limit

-

Ideal for retirement planning

Section 80E: Education Loan Interest

-

Deduction for interest paid on education loan

-

No upper limit

-

Available for 8 years

Section 80G: Donations

-

50% or 100% deduction on donations to eligible charities

-

Must be made to approved funds

ADVANCE TAX FOR FREELANCERS

What is Advance Tax?

Unlike salaried employees whose TDS is deducted monthly, freelancers must pay tax in installments during the year itself. This is called advance tax.

Who Must Pay?

| Tax Liability | Advance Tax Required? |

|---|---|

| ₹10,000 or more in a year | Yes |

| Less than ₹10,000 | No |

Advance Tax Due Dates

| Installment | Due Date | % of Tax Payable |

|---|---|---|

| 1st | 15th June | 15% |

| 2nd | 15th September | 45% |

| 3rd | 15th December | 75% |

| 4th | 15th March | 100% |

How to Calculate Advance Tax

| Step | Action |

|---|---|

| 1 | Estimate your income for the year |

| 2 | Subtract estimated expenses |

| 3 | Calculate tax on estimated income |

| 4 | Deduct TDS already credited |

| 5 | Pay balance in installments |

Example: Priya’s Advance Tax

| Parameter | Amount |

|---|---|

| Estimated receipts | ₹60,00,000 |

| Estimated expenses (actual) | ₹24,00,000 |

| Net income | ₹36,00,000 |

| Tax on ₹36 lakh (old regime) | ~₹8.5 lakh |

| TDS to be deducted by clients | ₹2.5 lakh |

| Advance tax payable | ₹6 lakh |

| Due Date | % | Amount |

|---|---|---|

| 15th June | 15% | ₹90,000 |

| 15th Sep | 45% (cumulative) | ₹1,80,000 |

| 15th Dec | 75% (cumulative) | ₹1,80,000 |

| 15th Mar | 100% (cumulative) | ₹1,50,000 |

Penalty for Non-Payment

Interest under Section 234B and 234C:

-

234B: 1% per month on shortfall if <90% paid by year-end

-

234C: 1% per month for delayed installments

COMMON TAX MISTAKES FREELANCERS MAKE

| Mistake | Consequence | How to Avoid |

|---|---|---|

| Not paying advance tax | Interest under 234B/234C | Estimate and pay quarterly |

| Ignoring GST registration | Penalty up to 10% of tax | Register when turnover exceeds limit |

| Not claiming legitimate expenses | Pay more tax than needed | Track all business expenses |

| Mixing personal and business | Disallowed expenses | Separate bank account |

| Not issuing proper invoices | Payment delays, TDS issues | Use professional invoices |

| Missing TDS on own payments | Disallowance under 40(a)(ia) | Deduct TDS on eligible payments |

| Choosing wrong tax regime | Higher tax liability | Calculate both before deciding |

| Not filing on time | Late fee ₹5,000-10,000 | File by 31st July |

| Not reconciling Form 26AS | TDS credit mismatch | Download and verify before filing |

| Forgetting 80C/80D | Missed tax savings | Plan investments early |

FREQUENTLY ASKED QUESTIONS

Q1: What is Section 44ADA and who can use it?

Section 44ADA is a presumptive taxation scheme for specified professionals (doctors, lawyers, architects, accountants, engineers, interior decorators, technical consultants, etc.) with gross receipts up to ₹75 lakh. You can declare 50% of receipts as profit and avoid maintaining books .

Q2: Can I claim both 44ADA and actual expenses?

No. Under 44ADA, the 50% profit rate is deemed to cover all expenses. You cannot claim separate deductions for expenses. However, you can still claim 80C, 80D, etc. (personal investments).

Q3: Do freelancers need to pay GST?

If your annual turnover exceeds ₹20 lakh (₹10 lakh for special category states), GST registration is mandatory. Even below threshold, you may voluntarily register to claim ITC or work with corporate clients who require GST invoices .

Q4: What expenses can freelancers claim?

Common deductible expenses include: office rent, laptop/equipment, software subscriptions, internet/phone bills, client travel, professional fees, marketing, insurance, depreciation, and home office portion (if applicable) .

Q5: What is the TDS rate on freelance income?

TDS on professional fees under Section 194J is 10% (if payment exceeds ₹30,000). For contracts under 194C, rate is 1-2% .

Q6: When should freelancers pay advance tax?

If your estimated tax liability exceeds ₹10,000 in a year, you must pay advance tax in installments by 15th June, 15th September, 15th December, and 15th March .

Q7: Which ITR form should freelancers file?

-

ITR-3: If you maintain regular books and claim actual expenses

-

ITR-4: If you opt for presumptive taxation under Section 44ADA

Q8: Can freelancers invest in 80C to save tax?

Yes. Investments in PPF, ELSS, LIC, etc. up to ₹1.5 lakh are deductible under Section 80C, regardless of whether you use presumptive taxation .

Q9: What is the penalty for late filing of ITR?

Late filing fee under Section 234F:

-

₹5,000 if filed by 31st December

-

₹10,000 if filed after 31st December

-

₹1,000 if total income ≤ ₹5 lakh

Q10: How do I reconcile TDS with my income?

Download Form 26AS from the income tax portal. Ensure all TDS deducted by clients matches the amounts shown. Report all such income in your ITR.

ACTIONABLE CHECKLIST: FREELANCER TAX PLANNING

Throughout the Year

-

Maintain separate bank account for business

-

Track all income (with invoices)

-

Keep all expense bills (scan/digitize)

-

Reconcile TDS credits in Form 26AS quarterly

-

Set aside 20-30% of income for taxes

April-June (Start of Year)

-

Estimate income for the year

-

Decide: Presumptive (44ADA) or regular scheme?

-

Calculate advance tax liability

-

Pay 1st installment by 15th June (if applicable)

July-September

-

Review income against estimate

-

Pay 2nd advance tax by 15th September

-

Check if GST turnover nearing threshold

October-December

-

Pay 3rd advance tax by 15th December

-

Review 80C investments – on track for ₹1.5L?

-

Ensure health insurance premium paid (80D)

January-March (Year-End)

-

Pay final advance tax by 15th March

-

Make any remaining 80C investments

-

Compile all income and expense records

-

Generate GST invoices for March transactions

July-August (Filing Time)

-

Download Form 26AS and AIS

-

Calculate total income and tax

-

File ITR (ITR-3 or ITR-4)

-

E-verify immediately

Tools to Help

-

Use India Tax Tools’ Advanced Tax Calculator to compare regimes

-

GST Calculator for correct tax on invoices

-

Invoice Generator for professional bills

-

TDS Calculator to compute TDS on your payments

-

80C Calculator to plan investments

-

Due Date Tracker for advance tax and filing

SUCCESS STORY: HOW A FREELANCER SAVED ₹2.1 LAKH

Profile: Ananya, 32, freelance content writer and strategist in Mumbai

Annual receipts: ₹48 lakh

Before optimization: Paid tax on full income with minimal planning

Her Tax-Smart Moves

| Strategy | What She Did | Tax Saved |

|---|---|---|

| Section 44ADA | Opted for presumptive (50% profit) vs actual (65% after expenses) | ₹65,000 |

| Expense tracking | Started claiming home office (30%), laptop, software, internet | ₹42,000 (lower profit) |

| 80C investments | ₹1.5L in ELSS + PPF | ₹45,000 |

| 80D health insurance | ₹25,000 premium for self | ₹7,500 |

| GST compliance | Registered voluntarily, claimed ITC on expenses | ₹18,000 |

| Advance tax planning | Avoided interest under 234B/234C | ₹12,000 |

| TDS reconciliation | Claimed all TDS credits (earlier missed ₹25,000) | ₹25,000 |

Total tax saved: ₹2,14,500

“I used to dread taxes. Now I plan for them. The Section 44ADA option alone saved me over ₹60,000 without any extra work. Every freelancer should understand these rules.” – Ananya

CONCLUSION: YOUR FREELANCE TAX SUCCESS

Tax planning for freelancers isn’t complicated—it’s about knowing the rules and applying them consistently. The key takeaways:

- Use Section 44ADA if your profit margin is >50% – simplifies compliance

- Track every expense – if not under presumptive, claim them all

- Understand GST – register when threshold crossed, charge correctly

- Pay advance tax – avoid interest penalties

- Invest in 80C/80D – reduce taxable income

- Reconcile TDS – ensure all credits claimed

- File on time – avoid late fees

Your Next Steps

-

Calculate your tax using India Tax Tools’ Advanced Tax Calculator

-

Decide on 44ADA – is it right for you?

-

Set up expense tracking – use an app or spreadsheet

-

Plan advance tax payments – mark those dates

-

Review GST position – are you crossing the threshold?

-

Invest wisely – use 80C and 80D to save more

Remember: Every rupee saved in tax is a rupee earned. With smart planning, you can keep more of what you work so hard for.

“As a freelancer, you’re not just selling your skills—you’re running a business. Treat your taxes the same way: plan, track, and optimize. Every rupee saved is your hard-earned money, staying with you.”

Disclaimer: This article is for informational and educational purposes only. Tax laws, rates, and thresholds are subject to change based on government notifications. Please consult a qualified Chartered Accountant for advice tailored to your specific situation. The information provided is based on Budget 2026 announcements and current provisions as of February 2026. India Tax Tools calculators are free tools for estimation and should not be considered as professional tax advice.