Are you tired of seeing a massive chunk of your hard-earned salary disappear into the “Tax” column of your payslip? If you are a salaried professional living in a rented house, you might be sitting on a goldmine of tax savings without even realizing it. According to recent 2025-26 fiscal surveys, nearly 40% of urban Indian employees fail to optimize their House Rent Allowance (HRA), often leaving thousands of rupees on the table.

The House Rent Allowance is not just a line item in your salary break-up; it is a powerful tool designed by the Income Tax Department to ease the burden of high urban rents. However, the calculation isn’t as simple as “rent paid equals tax saved.” It involves a specific three-way formula under Section 10(13A) of the Income Tax Act. In this guide, we will break down the complexities, show you how to use an HRA exemption calculator effectively, and reveal strategies to maximize your take-home pay.

Understanding the Mechanics of Section 10(13A)

Before jumping into the numbers, you need to understand the legal backbone of HRA. The Income Tax Act allows for an exemption on HRA if you live in a rented accommodation and it is a part of your salary structure.

It is important to note that if you opt for the New Tax Regime, HRA exemptions are generally not available. This guide focuses on taxpayers sticking with the Old Tax Regime, which remains popular for those with high investments and high rent outlays.

The Three Golden Rules of HRA Calculation

The amount exempt from tax is the minimum of the following three amounts:

-

The actual HRA received from your employer.

-

Actual rent paid minus 10% of your “salary.”

-

50% of your salary (if you live in a metro city) or 40% of your salary (non-metro).

Pro Tip: In tax terminology, “Salary” for HRA purposes means Basic Salary + Dearness Allowance (DA). Other perks and bonuses are excluded.2. Metro vs. Non-Metro: The Geographic Advantage

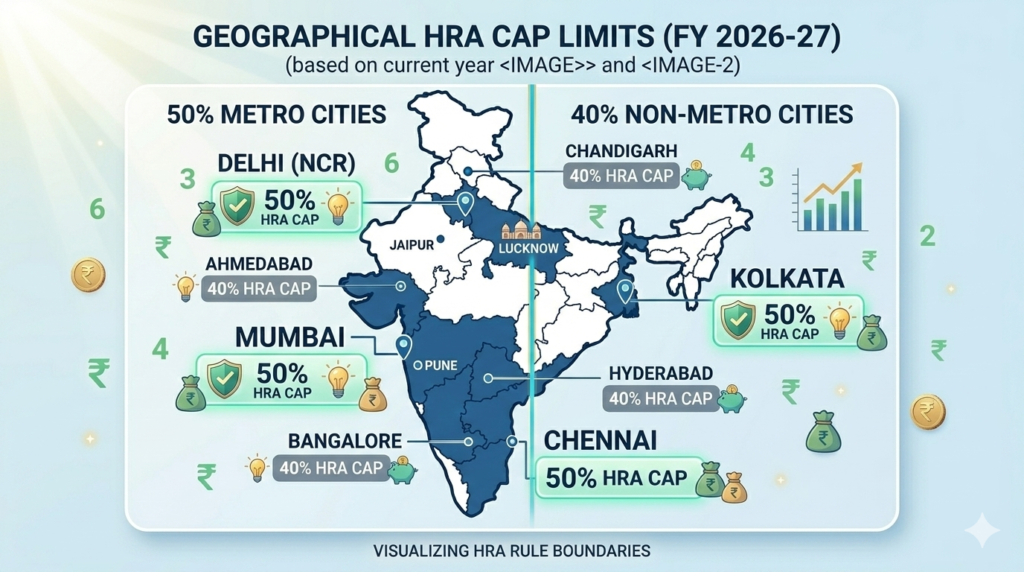

Location plays a pivotal role in how much you can claim. The Income Tax Department classifies only four cities as “Metros” for the 50% rule: Delhi, Mumbai, Kolkata, and Chennai.

If you reside in tech hubs like Bangalore, Hyderabad, or Pune, you technically fall under the 40% category for HRA purposes. This is a common point of confusion for many IT professionals.

How to Use an HRA Exemption Calculator Correctly

Calculating HRA manually can lead to errors, especially when your salary changes mid-year or you move houses. An online HRA Calculator simplifies this by automating the comparison.

Step-by-Step Input Guide:

-

Basic Salary: Enter your monthly or annual basic pay.

-

HRA Received: Found on your Form 16 or monthly payslip.

-

Total Rent Paid: The actual amount transferred to your landlord.

-

City Type: Select Metro or Non-Metro based on where the rented house is located, not where your office is.

Comparison Table: HRA Impact at Different Rent Levels

| Component (Annual) | Scenario A (Low Rent) | Scenario B (High Rent) |

|---|---|---|

| Basic Salary | ₹6,00,000 | ₹6,00,000 |

| Actual HRA Received | ₹3,00,000 | ₹3,00,000 |

| Rent Paid | ₹1,20,000 (10k/mo) | ₹2,40,000 (20k/mo) |

| Tax Exempt HRA | ₹60,000 | ₹1,80,000 |

| Taxable HRA | ₹2,40,000 | ₹1,20,000 |

Documentation: The Key to a Hassle-Free Claim

The Income Tax Department has become increasingly vigilant about “sham” rent claims. To ensure your claim isn’t rejected, you must maintain a paper trail.

-

Rent Agreement: Must be valid and signed. Digital signatures are generally accepted in 2026, but ensure the stamp duty is paid.

-

Rent Receipts: Required for all months. If rent exceeds ₹3,000 per month, a revenue stamp is necessary.

-

Landlord’s PAN: Mandatory if your annual rent exceeds ₹1,00,000.

-

Payment Proof: While cash is legal, banking channels (UPI, IMPS, Cheques) provide the best evidence during an audit.

Can You Pay Rent to Your Parents?

This is a frequently asked question. The answer is Yes, but it must be a genuine transaction. You cannot “gift” the money; you must pay it as rent.

-

The Process: Transfer the money to their account monthly.

-

Tax Impact for Parents: The rent you pay will be considered “Income from House Property” for them. However, they get a standard 30% deduction on that income.

-

The Catch: You cannot pay rent to your spouse and claim HRA, as the law views the marital relationship as a shared living obligation.

Common Pitfalls and How to Avoid Them

Many taxpayers lose out on benefits due to simple mathematical or clerical errors.

-

Sharing a Flat: If you share a flat with friends, you can only claim the portion of the rent you pay. Ensure the rent agreement mentions your name as a co-tenant.

-

Dual Benefit: Can you claim both HRA and Home Loan interest (Section 24)? Yes, if you own a house in one city but work and rent in another.

-

Missing PAN: If your landlord doesn’t have a PAN, you must obtain a written declaration (Form 60) from them to stay compliant.

Strategic Salary Structuring for 2026

As we move further into 2026, many companies offer “Flexible Benefit Plans.” If your rent is high, ask your HR if you can increase the HRA component of your salary while reducing other taxable allowances.

For example, if you pay ₹40,000 in rent but your HRA component is only ₹20,000, you are losing out. Increasing the HRA component (within the 50% basic salary limit) can significantly lower your taxable income.

FAQ Section

Q1: Can I claim HRA if I don’t get HRA in my salary? No, you cannot claim exemption under Section 10(13A). However, you may be eligible for a deduction under Section 80GG, provided you don’t own a house in the city of employment.

Q2: What if I forgot to submit rent receipts to my HR? Don’t worry. You can still claim the HRA exemption directly while filing your Income Tax Return (ITR). Keep the receipts safe in case of a scrutiny notice.

Q3: Is HRA calculated on a monthly or yearly basis? It is calculated monthly if there are changes in salary or rent. If everything remains constant, a yearly calculation suffices.

Q4: Is a revenue stamp mandatory on rent receipts? Only if the cash payment per receipt exceeds ₹5,000. For bank transfers, it is technically not required, but many HR departments still insist on it for uniformity.

Conclusion

Maximizing your HRA exemption is one of the simplest ways to reduce your tax liability in 2026. By understanding the 50/40 rule, maintaining proper documentation, and using a reliable HRA exemption calculator, you can ensure that you keep more of your money where it belongs—in your pocket.

Ready to see how much you can save? Head over to our suite of Tax Tools to calculate your exact exemption and plan your investments for the upcoming quarter. Tax planning isn’t a year-end activity; it’s a year-round strategy. Start today!

Disclaimer: The information provided in this article is for educational purposes only and does not constitute professional tax advice. Tax laws are subject to change. Please consult with a certified tax professional or use the official IndiaTaxTools.com resources for personalized calculations.