Meet Ramesh, who runs a wholesale electronics business in Delhi. Last month, his truck carrying ₹8 lakh worth of goods was stopped at a checkpost in Uttar Pradesh. The e-way bill had expired two hours earlier—he’d forgotten that the 500km trip needed a 5-day validity, not 1 day. Result: ₹40,000 penalty and a 3-day delay.

Then there’s Priya, a Pune-based furniture manufacturer. She generates e-way bills daily but was shocked when her GST registration was suspended—because she’d missed linking her e-way bills to filed GSTR-1. She didn’t know the new 2026 rule.

If you transport goods, e-way bills are your business’s passport. Without a valid one, your goods can be detained, penalties levied, and even your GST registration suspended.

In 2026, significant changes have been made to the e-way bill system:

-

Auto-suspension link: Miss GSTR-3B? No e-way bills for you

-

Revised validity periods: Distance-based, with new rules for multi-vehicle trips

-

Consolidated bills: Simplified for multiple consignments

-

Blocked generation: If Part A and Part B mismatch

-

QR code mandate: For certain consignments

In this comprehensive guide, you’ll discover:

-

What is e-way bill and who needs it (thresholds updated)

-

7 major rule changes for 2026 explained

-

Step-by-step generation process with screenshots

-

Validity calculator by distance

-

Common mistakes that lead to penalties

-

Compliance checklist for traders

-

Real examples of penalties and how to avoid them

Let’s ensure your goods move smoothly across India.

WHAT IS E-WAY BILL AND WHO NEEDS IT?

An e-way bill is an electronic document required for the movement of goods where the consignment value exceeds ₹50,000. It’s mandatory under GST and must be generated on the e-way bill portal before the goods are transported.

When is E-Way Bill Required?

Who Can Generate E-Way Bill?

Key Components

E-Way Bill Number (EBN)

Exemptions (No E-Way Bill Needed)

*Source: GST Act, Rule 138 *

MAJOR E-WAY BILL RULE CHANGES FOR 2026

Seven key updates every trader must know.

Change 1: Auto-Suspension Link with GST Registration

Impact: Can’t generate new e-way bills during suspension period. Goods transport stops.

Change 2: Revised Validity Periods

Over-dimensional cargo: Double the validity period.

Change 3: Consolidated E-Way Bill for Multiple Consignments

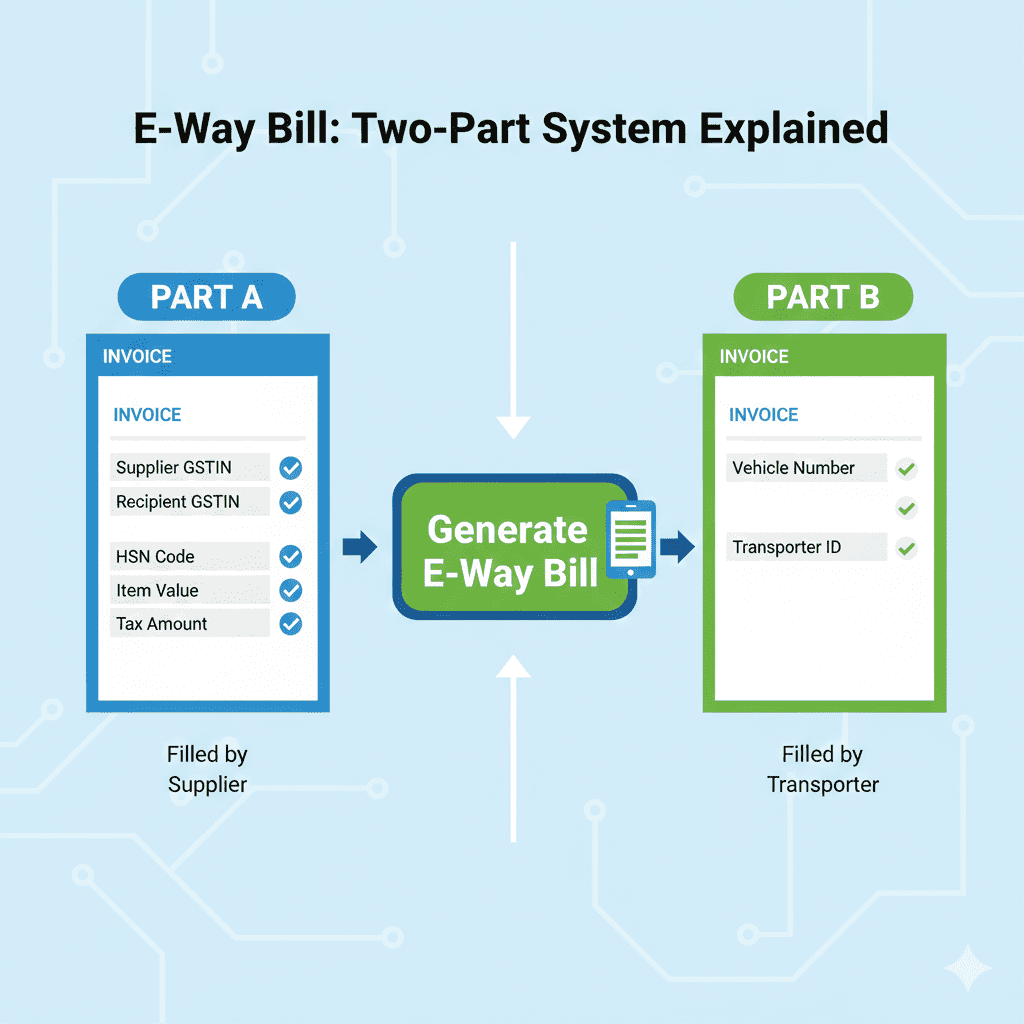

Change 4: Blocked Generation for Part A/Part B Mismatch

If Part A (invoice details) and Part B (vehicle details) don’t match, e-way bill generation is blocked until corrected.

Change 5: QR Code Mandate for High-Value Consignments

Change 6: Mandatory Updating of Vehicle Number for Multimodal Transport

If vehicle changes during transit (e.g., truck to smaller vehicle), Part B must be updated within 24 hours, else e-way bill invalid.

Change 7: Integration with FASTag for Toll/Checkpost

Pilot project in select states: e-way bill linked to FASTag for automatic validation at toll plazas and checkposts.

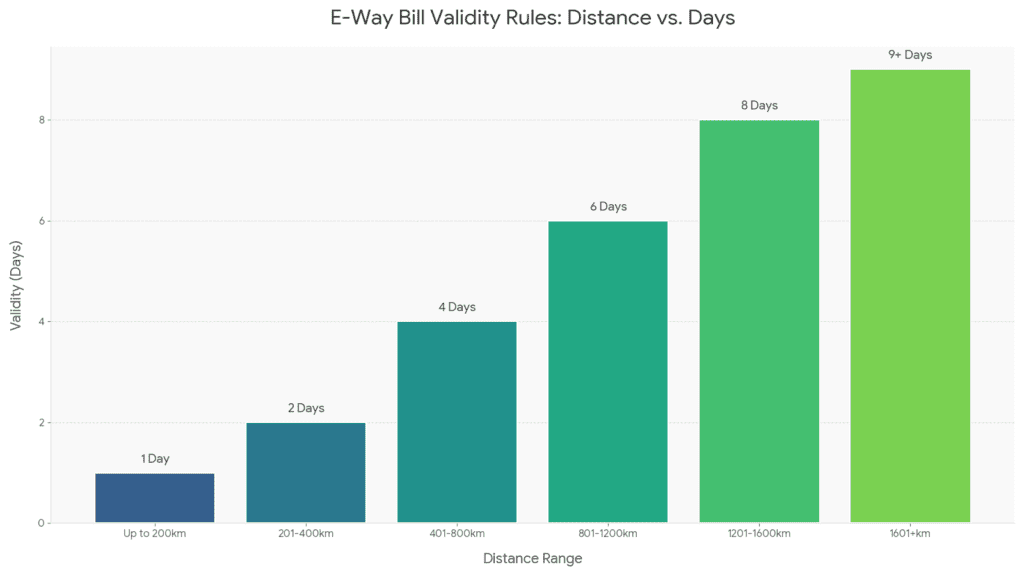

E-WAY BILL VALIDITY CALCULATION (2026 RULES)

Validity Table by Distance

Example Calculations

Example 1: Delhi to Jaipur (280 km)

Example 2: Mumbai to Bangalore (980 km)

Example 3: Chennai to Delhi (2,180 km)

Extension Rules

Over-Dimensional Cargo

HOW TO GENERATE E-WAY BILL: STEP-BY-STEP

Step 1: Login to Portal

Visit https://ewaybillgst.gov.in or use GST portal integration.

Step 2: Fill Part A

Step 3: Generate Part A

Step 4: Fill Part B

Step 5: Generate E-Way Bill

-

Click “Generate E-Way Bill”

-

System generates 12-digit E-Way Bill Number (EBN)

-

Valid for period based on distance

Step 6: Print/Share

Via SMS/Android App

Also possible via:

CONSOLIDATED E-WAY BILL: WHEN AND HOW

What is Consolidated E-Way Bill?

When multiple consignments are transported in the same vehicle, you can generate one consolidated e-way bill instead of separate bills for each invoice.

When to Use

How to Generate

Advantages

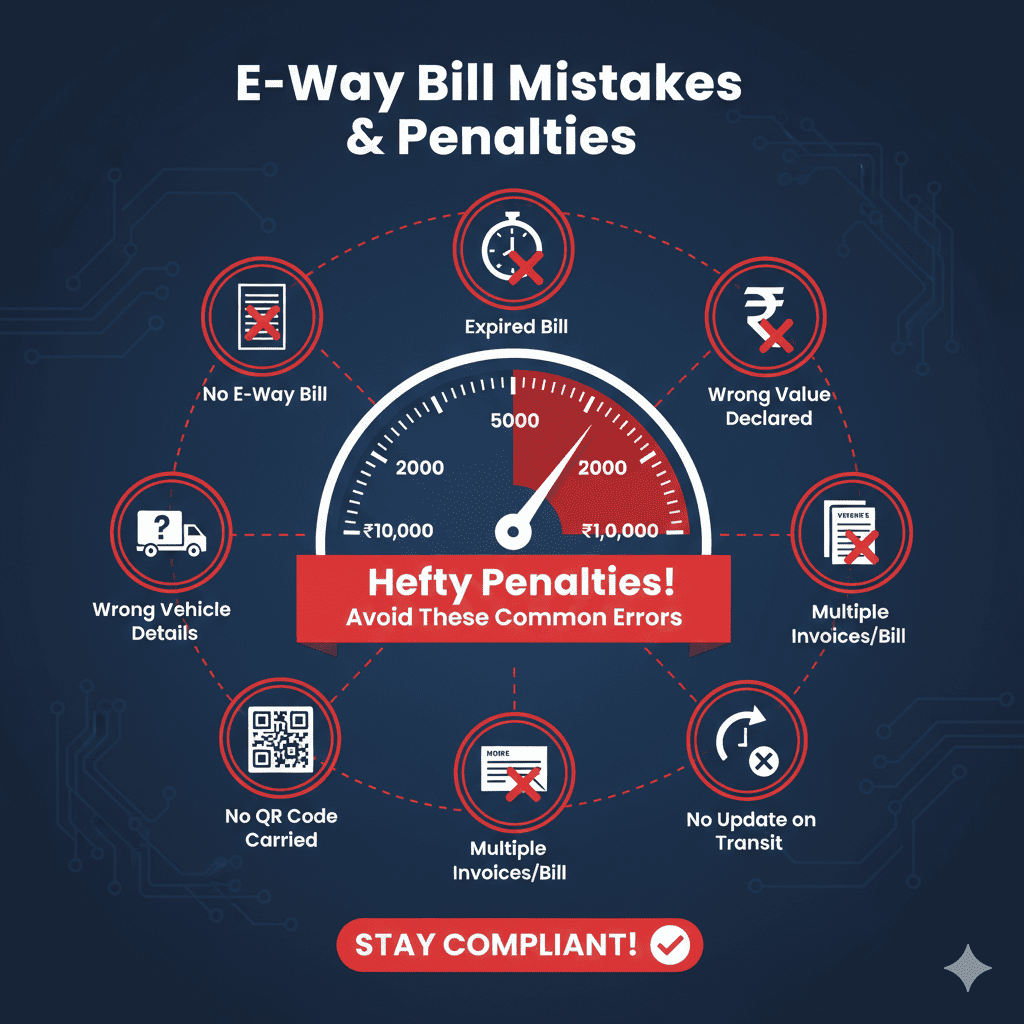

COMMON E-WAY BILL MISTAKES AND PENALTIES

Top 10 Mistakes

Penalty Provisions (Section 129 & 130)

Example

Scenario: Truck with goods worth ₹5 lakh, IGST @18% (₹90,000). No e-way bill.

Plus goods detained until penalty paid.

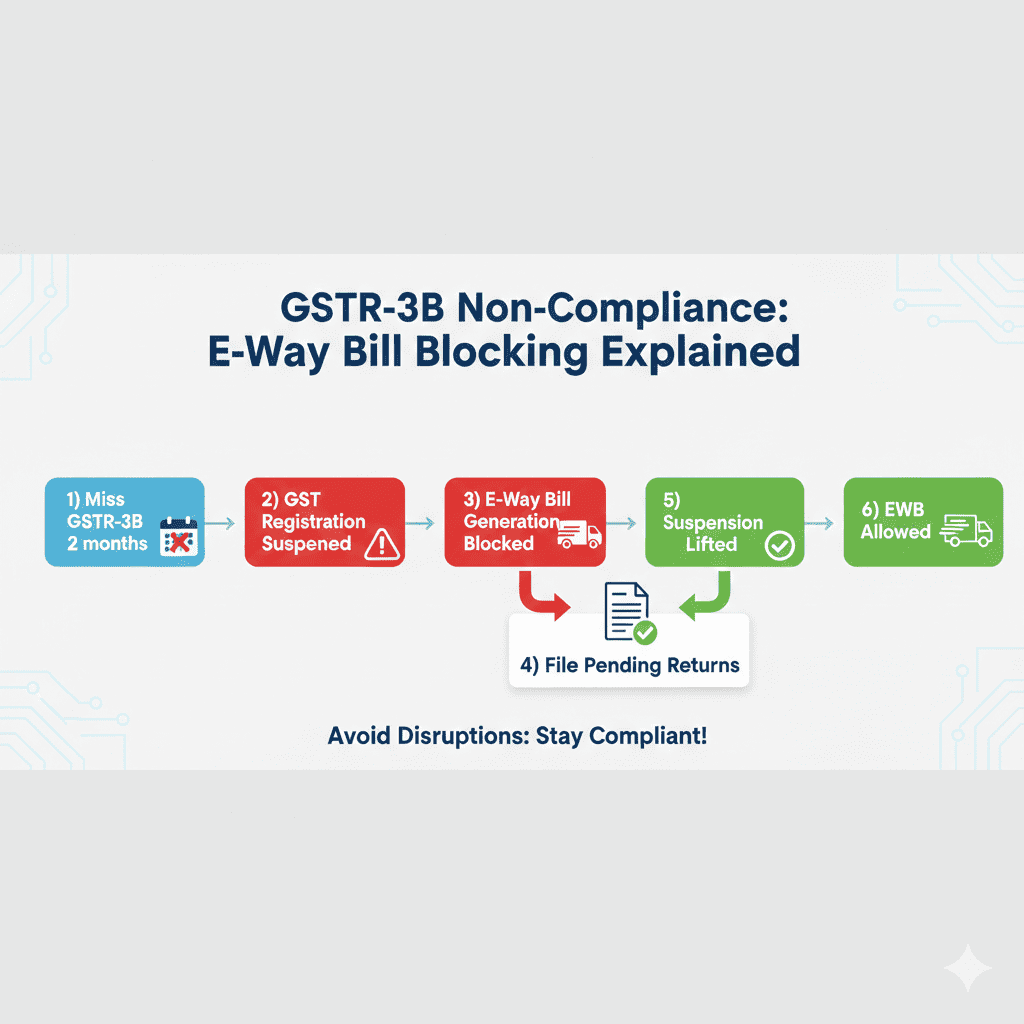

E-WAY BILL AND GST REGISTRATION SUSPENSION LINK

How They Are Linked

From 2026, if your GST registration is suspended (due to non-filing of 2 consecutive GSTR-3B), the e-way bill portal automatically blocks generation of new e-way bills.

What Happens

Reactivation

Example

Scenario: A trader filed GSTR-3B for Jan and Feb 2026, but missed March and April.

Prevention

E-WAY BILL FOR SPECIAL SCENARIOS

Scenario 1: Bill-to-Ship-to (Multiple Locations)

Scenario 2: Goods Returned

Scenario 3: Movement Without Invoice (Sample, Gift)

Scenario 4: Multiple Vehicles for One Consignment

FREQUENTLY ASKED QUESTIONS

Q1: What is the new e-way bill validity for 500 km in 2026?

500 km falls in 401-800 km range, so validity is 4 days (from earlier 1+1 per 100km) .

Q2: Can I generate e-way bill if my GST registration is suspended?

No. From 2026, if your registration is suspended (due to non-filing of returns), e-way bill generation is automatically blocked .

Q3: What is the penalty for no e-way bill?

Penalty under Section 129 is 100% of tax payable on goods or ₹10,000, whichever is higher .

Q4: Do I need e-way bill for intra-state movement?

It depends on your state’s threshold. Most states have notified e-way bill for intra-state movement where consignment value exceeds ₹1 lakh (varies by state).

Q5: What is consolidated e-way bill?

When multiple consignments are transported in the same vehicle, you can generate one consolidated e-way bill listing all invoice numbers instead of separate bills .

Q6: How do I extend an e-way bill?

Before expiry, login to portal, select “Extend Validity”, and generate extension. Can be done multiple times, but total validity cannot exceed prescribed limits without genuine reason.

Q7: What if vehicle changes during transit?

Update Part B with new vehicle number within 24 hours of change. Otherwise, e-way bill becomes invalid .

Q8: Is QR code mandatory on e-way bill?

For consignments valued above ₹5 lakh, QR code must be printed and affixed. For others, optional .

Q9: Can unregistered person generate e-way bill?

No. Unregistered persons cannot generate e-way bill. They must either:

Q10: What documents must accompany goods?

-

E-way bill (print or electronic)

-

Invoice or delivery challan

-

Transporter’s document (LR, if applicable)

ACTIONABLE CHECKLIST: E-WAY BILL COMPLIANCE FOR TRADERS

Before Movement

-

Check if consignment value > ₹50,000 (inter-state) or applicable intra-state threshold

-

Ensure GST registration is active (not suspended)

-

Generate e-way bill before goods leave

-

Verify Part A (invoice details) matches actual invoice

-

Verify Part B (vehicle number) is correct

-

Check validity period based on distance

-

Print e-way bill (2 copies)

-

If multiple consignments, consider consolidated bill

-

If value > ₹5 lakh, generate QR code and affix

During Transit

-

Keep e-way bill copy with goods

-

If vehicle changes, update Part B within 24 hours

-

Monitor expiry – extend before validity ends if needed

-

Ensure e-way bill number matches invoice

After Delivery

Monthly/Quarterly

-

Ensure all GSTR-3B filed (to avoid suspension)

-

Reconcile e-way bills generated vs GSTR-1 filed

-

Check for any pending e-way bill extensions

-

Review any penalties/detentions and address root cause

Tools to Help

REAL CASE STUDY: HOW A TRADER SAVED ₹90,000 BY COMPLIANCE

Profile: Sharma Electronics, Delhi – wholesale electronics distributor

Annual turnover: ₹12 crore

Monthly consignments: 150-200

Their Compliance System

Near-Miss Incident

Scenario: A consignment to Bangalore (2,200 km) – validity 11 days.

Without alert: Bill would have expired on day 11 morning, goods detained at entry, penalty of ₹90,000 (100% of tax).

Result

“The new rules are stricter, but they forced us to systemize. Now we never miss a deadline, and our goods move freely.” – Mr. Sharma, Proprietor

CONCLUSION: STAY COMPLIANT, KEEP GOODS MOVING

E-way bills are the lifeline of goods transport under GST. The 2026 updates—tighter validity, suspension links, consolidated options, and QR mandates—are designed to make the system more robust and fraud-resistant.

For traders, the message is clear:

-

Generate before movement – not after

-

Track validity – set alerts, extend on time

-

Link with GST returns – avoid suspension

-

Use consolidated bills – simplify multiple consignments

-

Verify details – Part A and Part B must match

Your Action Plan

- Set up reminders for GSTR-3B (20th) and e-way bill expiry

- Integrate e-way bill generation with your billing software

- Train team on new validity rules and consolidated options

- Reconcile monthly – e-way bills with GSTR-1

- Use tools like India Tax Tools for error-free generation

Remember

-

Two missed GSTR-3B = no e-way bills

-

Wrong vehicle number = invalid bill

-

Expired bill = detained goods + penalty

-

QR code for high value = mandatory

Stay compliant, and your goods will move smoothly across India.

“An e-way bill isn’t just a number—it’s your goods’ passport across India. Generate it right, track it well, and never let it expire.”

Disclaimer: This article is for informational and educational purposes only. E-way bill rules, validity periods, and penalties are subject to change based on government notifications. Please consult your Chartered Accountant or GST practitioner for advice tailored to your specific business circumstances. The information provided is based on GST updates available as of February 2026.

India Tax ToolsFebruary 24, 20269 Mins read36

India Tax ToolsFebruary 24, 20269 Mins read36

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment