Latest Changes in GST Rules 2026 – 7 Major Changes Every Business Must Know

Then there’s Priya, a Pune-based consultant who just registered for GST. She was surprised when the portal asked her to visit the GST Seva Kendra for biometric verification. “I thought everything was online now,” she wondered.

Welcome to GST in 2026. The government has introduced major automation and enforcement changes that affect every registered taxpayer. From automatic suspension for non-filing to mandatory biometric verification for high-risk applicants, the rules are stricter—but also more streamlined.

In 2025, over 1.4 crore GST returns were filed monthly, but so were thousands of non-compliance notices . The new rules aim to reduce fraud, ensure timely compliance, and make the system truly self-policing.

In this comprehensive guide, you’ll discover:

-

Auto-suspension of registration—how missing two returns can stop your business

-

Bank account updates—now mandatory, with strict deadlines

-

Biometric verification—who must visit GST Seva Kendra

-

Invoice Management System (IMS)—new way to manage ITC

-

Return filing blocks—ledger mismatches now prevent GSTR-3B

-

Three-year return filing rule—older returns permanently blocked

-

Multi-factor authentication—mandatory for portal access

-

Practical checklists to stay compliant

Let’s ensure your business stays ahead of these changes.

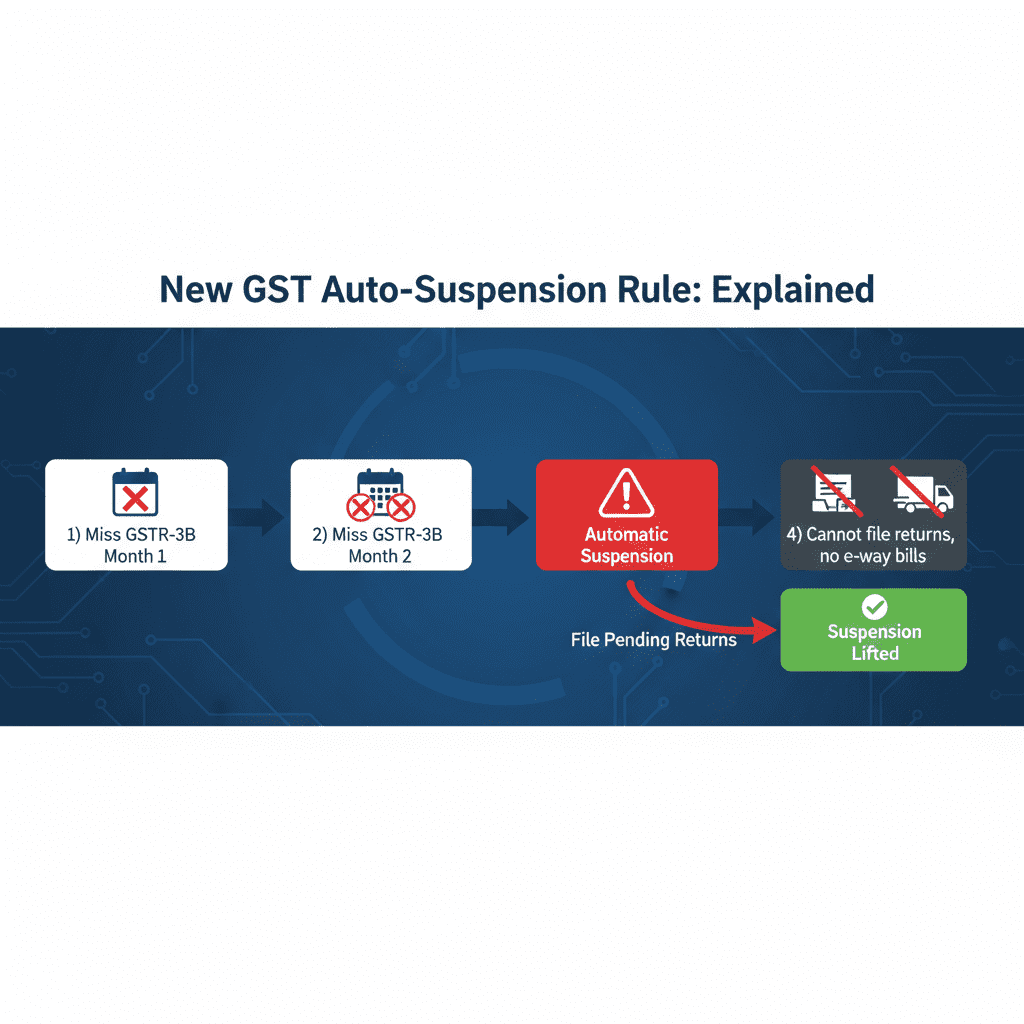

RULE 1: AUTOMATIC SUSPENSION OF REGISTRATION FOR NON-FILING

This is perhaps the most impactful change for regular taxpayers.

What Changed?

From January 2026, if a taxpayer fails to file GSTR-3B for two consecutive months (or one quarter for quarterly filers), the GST portal will automatically suspend their registration .

What Happens When Suspended?

| Impact | Consequence |

|---|---|

| Cannot file future returns | All pending returns must be filed first |

| Cannot generate e-way bills | Goods transport stops |

| ITC blocked for recipients | Your customers cannot claim ITC on your invoices |

| No new invoices | Invoices issued during suspension may be invalid |

| Public visibility | Suspension status visible to all on portal |

How to Reactivate

| Step | Action |

|---|---|

| 1 | File all pending GSTR-3B returns |

| 2 | Pay any outstanding tax, interest, and late fees |

| 3 | System automatically revokes suspension |

| 4 | Can resume normal business |

Example

Scenario: A Mumbai trader filed GSTR-3B for January and February 2026, but missed March and April.

| Month | Action | Status |

|---|---|---|

| March | Missed filing | First miss |

| April | Missed filing | Second consecutive miss |

| May 1 | Portal automatically suspends registration | Cannot file returns or generate e-way bills |

| May 5 | Files March and April returns with late fees | Suspension lifted automatically |

Prevention Tips

-

Set monthly calendar reminders for 20th of each month

-

File even if nil return—late fee applies for non-filing

-

Use India Tax Tools’ Due Date Tracker for alerts

RULE 2: BANK ACCOUNT DETAILS MANDATORY – AUTOMATIC SUSPENSION

What Changed?

Earlier, the GST portal didn’t strictly enforce bank account updates. Now, if you don’t furnish bank account details within 30 days of registration (or within prescribed timeline), the portal will automatically suspend your registration .

Why This Matters

| Without Bank Details | Consequence |

|---|---|

| Cannot file returns | All returns blocked |

| No refunds | Cannot receive GST refunds |

| Verification incomplete | Registration considered incomplete |

| Suspension | Automatic after 30 days |

What to Do

| Action | Timeline |

|---|---|

| Open a bank account for business | Immediately after GST registration |

| Update details on GST portal | Within 30 days of registration |

| Verify with cancelled cheque | Upload clear document |

| Keep details updated | Any change requires amendment within 15 days |

Example

Scenario: A new registrant got GSTIN on 1st February 2026 but didn’t update bank details.

| Date | Event |

|---|---|

| 1 Feb 2026 | GST registration granted |

| 3 Mar 2026 | 30 days passed, bank details not updated |

| 4 Mar 2026 | Portal automatically suspends registration |

| 5 Mar 2026 | Business owner cannot file returns or generate e-way bills |

| 6 Mar 2026 | Updates bank details → suspension lifted |

Prevention Tips

-

Add bank details immediately after receiving GSTIN

-

Keep scanned cancelled cheque ready

RULE 3: BIOMETRIC VERIFICATION FOR HIGH-RISK APPLICANTS

What Changed?

To prevent fraudulent registrations, the government has introduced biometric-based Aadhaar authentication for applicants identified as “high-risk” based on data analytics .

Who Must Undergo Biometric Verification?

| Risk Category | Verification Required |

|---|---|

| Low-risk (based on PAN/Aadhaar history) | Online Aadhaar OTP only |

| Medium-risk | May be asked for biometric |

| High-risk (new businesses, certain profiles) | Must visit GST Seva Kendra |

The Process

| Step | Action |

|---|---|

| 1 | Apply for GST registration online |

| 2 | Portal assesses risk profile |

| 3 | If flagged, receive appointment for GST Seva Kendra |

| 4 | Visit with original documents |

| 5 | Provide fingerprints and photograph |

| 6 | Registration processed after verification |

Documents to Carry

-

Original PAN card

-

Original Aadhaar card

-

Business address proof

-

Photographs

-

Authorization letter (if representative)

Why This Matters

| Benefit | Impact |

|---|---|

| Fraud prevention | Reduces fake registrations used for ITC fraud |

| Faster processing for genuine | Low-risk applicants get auto-approval within 3 days |

| Stronger compliance | Identity verified physically |

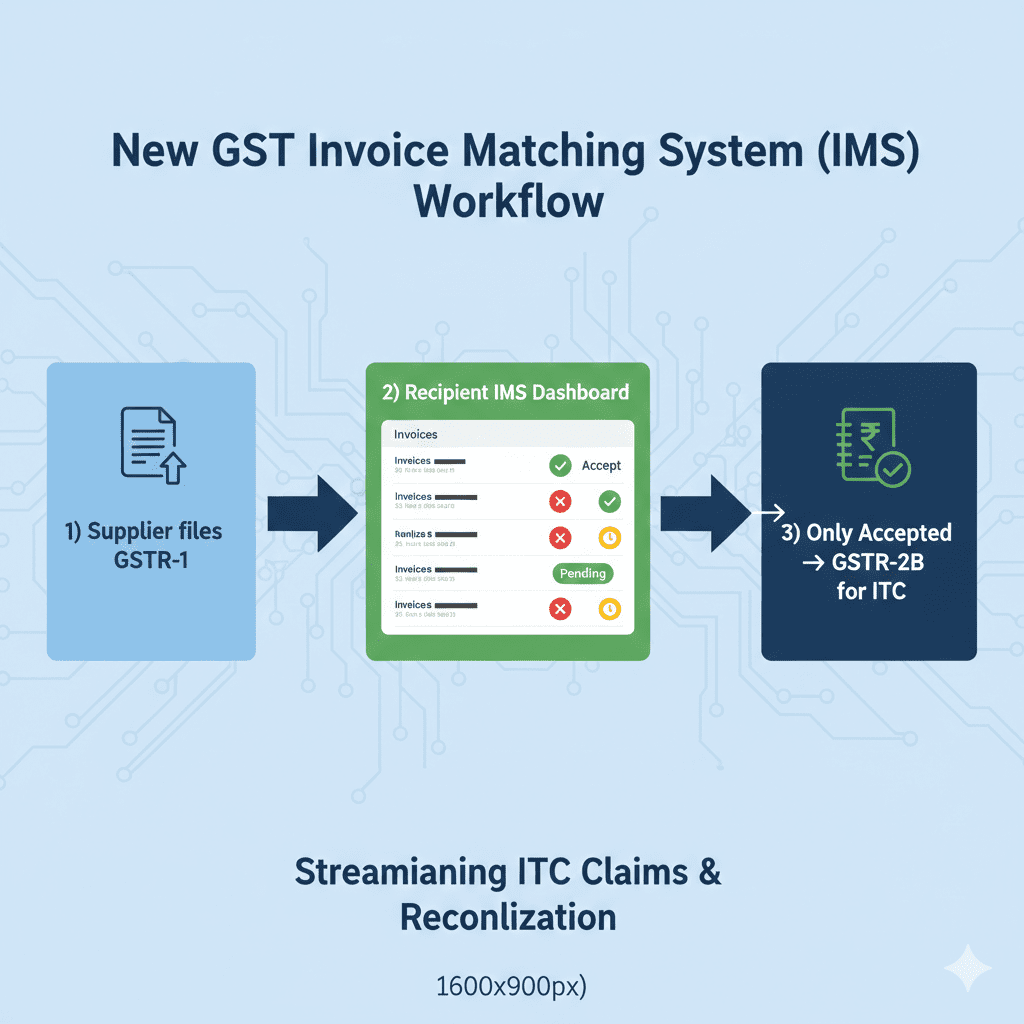

RULE 4: INVOICE MANAGEMENT SYSTEM (IMS) INTRODUCED

What Changed?

From January 2026, the new Invoice Management System (IMS) changes how Input Tax Credit (ITC) is claimed.

How IMS Works

| Step | Action |

|---|---|

| 1 | Supplier files GSTR-1 with invoices |

| 2 | Invoices appear in recipient’s IMS dashboard |

| 3 | Recipient must Accept, Reject, or Keep Pending each invoice |

| 4 | Only accepted invoices flow into GSTR-2B for ITC |

| 5 | Rejected invoices don’t give ITC; supplier gets notified |

New Form: GSTR-1A

Suppliers can now amend invoices based on recipient feedback through GSTR-1A .

| Scenario | Action |

|---|---|

| Recipient rejects invoice | Supplier can amend/cancel in GSTR-1A |

| Recipient keeps pending | ITC deferred; can be accepted later |

| Mismatch in details | Supplier can correct and re-report |

Impact on Businesses

| For Suppliers | For Recipients |

|---|---|

| Must ensure accurate invoices | Must actively reconcile monthly |

| Will know if ITC is being claimed | No automatic ITC—must accept |

| Can correct mistakes quickly | Reject incorrect invoices |

Example

Scenario: A Delhi supplier issues invoice to Mumbai buyer with wrong GSTIN.

| Step | Action |

|---|---|

| 1 | Invoice appears in buyer’s IMS |

| 2 | Buyer rejects (wrong GSTIN) |

| 3 | Supplier gets notification |

| 4 | Supplier issues corrected invoice in GSTR-1A |

| 5 | Buyer accepts → ITC claimed |

Prevention Tips

-

Verify customer GSTIN before invoicing (use GSTIN Verification Tool)

-

Reconcile purchase invoices with IMS monthly

-

Don’t assume ITC—actively accept

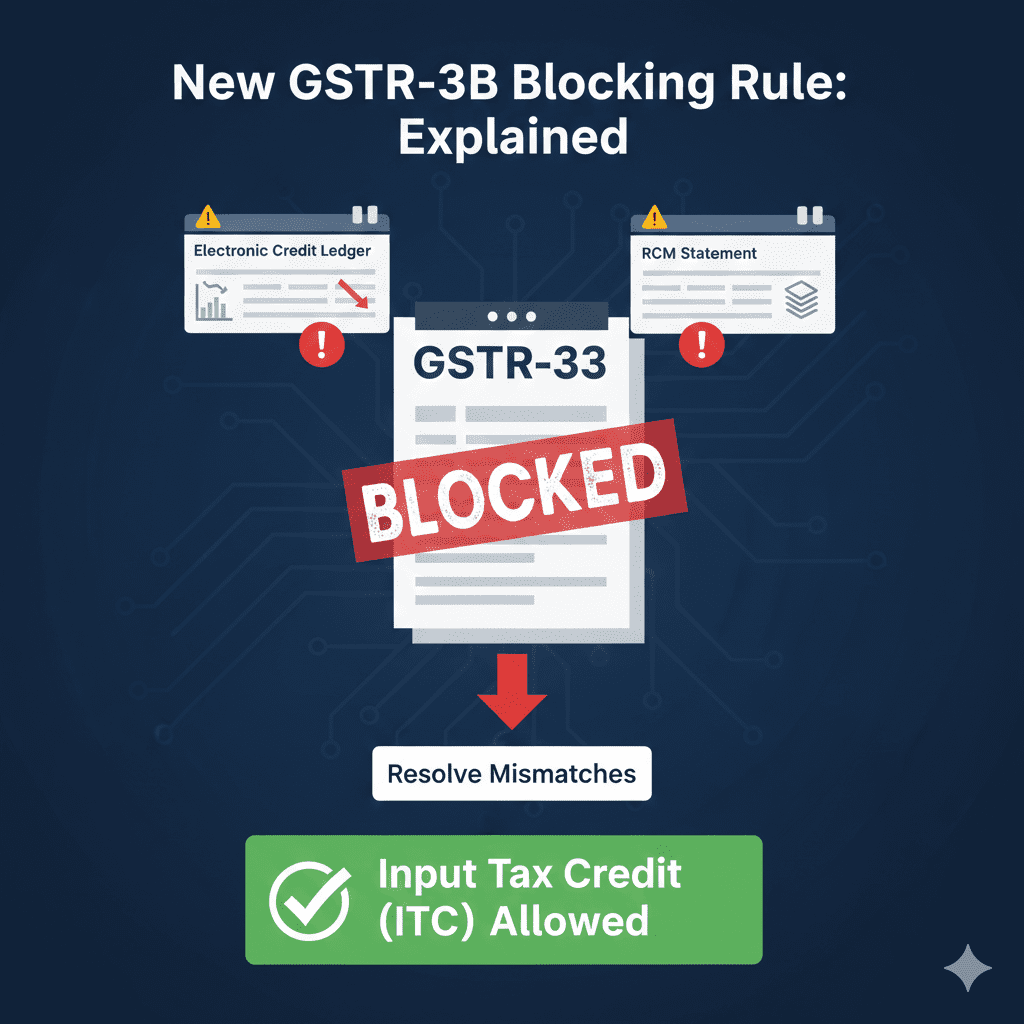

RULE 5: GSTR-3B FILING BLOCKED FOR LEDGER MISMATCHES

What Changed?

From January 2026, the GST portal checks two ledgers before allowing GSTR-3B filing:

| Ledger | What It Tracks |

|---|---|

| Electronic Credit Re-claim and Reversal Statement | ITC reversals and re-claims |

| RCM Liability / ITC Statement | Reverse charge transactions |

If these show negative balance or mismatches, GSTR-3B filing is blocked until resolved.

Common Mismatches

| Issue | Cause |

|---|---|

| Negative balance in credit ledger | Excess ITC claimed earlier and reversed |

| RCM mismatch | Tax payable under RCM not reported correctly |

| Duplicate ITC claims | Same invoice claimed in multiple periods |

How to Resolve

| Step | Action |

|---|---|

| 1 | Check error message in portal |

| 2 | Review relevant ledgers |

| 3 | Make necessary adjustments |

| 4 | File corrective return if needed |

| 5 | Only then GSTR-3B allowed |

Prevention Tips

-

Reconcile ITC monthly with GSTR-2B

-

Track RCM transactions separately

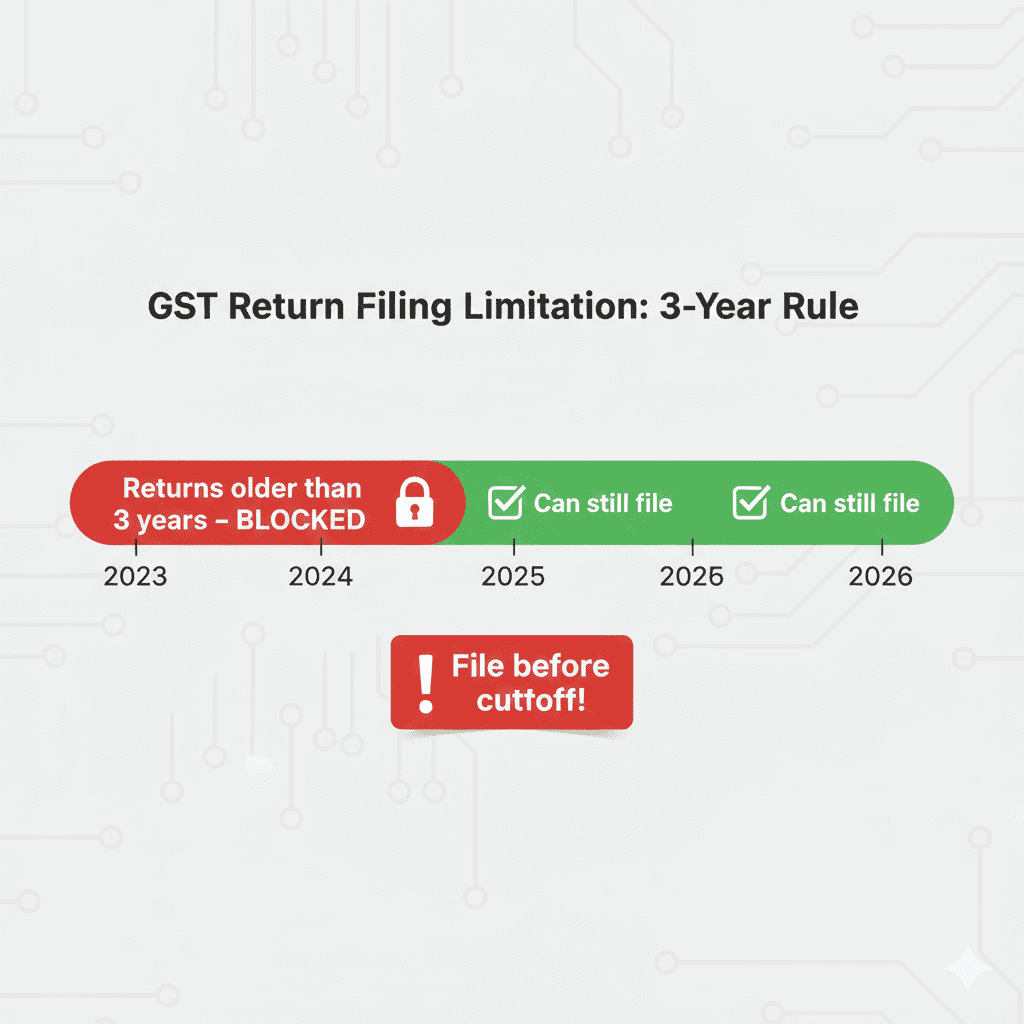

RULE 6: THREE-YEAR RETURN FILING RULE – STRICTLY ENFORCED

What Changed?

Returns older than three years from the due date are now permanently blocked from filing .

Impact

| Scenario | Consequence |

|---|---|

| Missed filing for FY 2021-22 or earlier | Cannot file now |

| ITC from old invoices | Cannot claim if not filed |

| Compliance gap | Permanent record |

Example

Scenario: A business missed filing GSTR-3B for March 2022 (due April 2022). In 2026, they try to file.

| Year | Due Date | Can they file in 2026? |

|---|---|---|

| 2022 | April 2022 | No (more than 3 years ago) |

| 2023 | April 2023 | No (more than 3 years ago) |

| 2024 | April 2024 | Yes (within 3 years) |

Why This Matters

-

Loss of ITC – Can’t claim credit for those periods

-

Penalties may still apply – Non-compliance attracts interest

-

Future registrations – History affects risk rating

Prevention Tips

-

File all returns on time

-

Set up system to track due dates

RULE 7: MULTI-FACTOR AUTHENTICATION (MFA) MANDATORY

What Changed?

All taxpayers accessing the GST portal must now use Multi-Factor Authentication (MFA) for enhanced security .

How It Works

| Step | Authentication |

|---|---|

| 1 | Enter username/password |

| 2 | OTP sent to registered mobile |

| 3 | Enter OTP to complete login |

For Taxpayers with Multiple Users

-

Each user (proprietor, partner, authorized signatory) must have separate login

-

MFA applies to all

-

No more shared logins

Impact

| Benefit | Concern |

|---|---|

| Enhanced security | Extra step each time |

| Prevents unauthorized access | Need to keep mobile accessible |

| Audit trail of who accessed | Multiple logins to manage |

9. COMPARISON TABLE: GST RULES 2025 VS 2026

| Rule | 2025 Position | 2026 Position |

|---|---|---|

| GSTR-3B non-filing | Notices issued | Auto-suspension after 2 misses |

| Bank account details | Recommended | Mandatory within 30 days |

| New registration verification | Mostly online | Biometric for high-risk |

| ITC management | Auto from GSTR-2B | IMS – Accept/Reject/Pending |

| GSTR-3B filing | Always allowed | Blocked for ledger mismatches |

| Old returns filing | Allowed (with fees) | Blocked after 3 years |

| Portal login | Password only | Multi-factor authentication |

IMPACT ON BUSINESSES: WHAT YOU MUST DO NOW

Immediate Actions

| Action | Deadline |

|---|---|

| Update bank account details on portal | Immediately (if not done) |

| Ensure all GSTR-3B filed (no pending) | Before next due date |

| Review registration risk profile | Check portal for any flags |

| Set up MFA for all users | Already implemented |

| Train team on IMS | Before next GSTR-2B |

Monthly Actions

| Task | Purpose |

|---|---|

| Reconcile sales with GSTR-1 before filing | Avoid mismatches |

| Check IMS dashboard – accept/reject invoices | Control ITC |

| Verify no negative balances in ledgers | Ensure smooth GSTR-3B |

| File GSTR-3B by 20th | Avoid auto-suspension |

| Monitor bank account details | Stay updated |

Quarterly Actions

| Task | Purpose |

|---|---|

| Review all pending invoices in IMS | Clear backlog |

| Check if any old returns need filing | Before 3-year cutoff |

| Verify compliance for all GSTINs | Avoid surprises |

FREQUENTLY ASKED QUESTIONS

Q1: What happens if I miss GSTR-3B for two months in 2026?

Your GST registration will be automatically suspended. You cannot file returns, generate e-way bills, or issue valid invoices. Reactivation requires filing all pending returns with late fees .

Q2: Is biometric verification mandatory for all new GST registrations?

No. Only applicants identified as “high-risk” based on data analytics must visit GST Seva Kendra for biometric verification. Low-risk applicants continue with online Aadhaar OTP .

Q3: What is the Invoice Management System (IMS)?

IMS is a new system where recipients must Accept, Reject, or Keep Pending each invoice reported by suppliers. Only accepted invoices flow into GSTR-2B for ITC claims. Suppliers can amend rejected invoices via GSTR-1A .

Q4: Can I file old GST returns now?

Only if they are within 3 years of the due date. Returns older than 3 years are permanently blocked from filing .

Q5: Why is my GSTR-3B filing blocked?

Possible reasons:

-

Negative balance in Electronic Credit Ledger

-

Mismatch in RCM Liability/ITC Statement

-

Pending previous returns

-

Suspended registration

Check the error message on portal and resolve accordingly.

Q6: What is the deadline to update bank account details?

Within 30 days of registration. Failure leads to automatic suspension. For existing registrants, ensure details are always updated .

Q7: Is multi-factor authentication mandatory?

Yes. All users accessing GST portal must use MFA (password + OTP) for login .

Q8: How does auto-suspension affect my customers?

During suspension, your customers cannot claim ITC on invoices issued by you. This may lead to payment delays and disputes.

Q9: Can I challenge auto-suspension?

Suspension is automatic based on non-filing. Once you file pending returns, suspension is automatically lifted. No separate application needed.

Q10: What are the late fees for delayed filing under new rules?

Late fees remain:

-

GSTR-3B: ₹50 per day (₹25 CGST + ₹25 SGST)

-

GSTR-1: ₹50 per day

-

Maximum ₹5,000 per return

Plus interest at 18% p.a. on tax liability.

ACTIONABLE CHECKLIST: PREPARE FOR GST 2026

Immediate (Before Next Filing)

-

Verify bank account details on GST portal – update if needed

-

Ensure no GSTR-3B pending for more than one month

-

Check if any returns older than 3 years need attention (file immediately)

-

Set up MFA for all users

-

Train accounts team on IMS (accept/reject invoices)

Monthly Compliance

-

File GSTR-1 by 11th (monthly) / 13th (quarterly)

-

Review IMS dashboard – accept/reject all invoices

-

Reconcile ITC with GSTR-2B

-

Check ledgers for negative balances

-

File GSTR-3B by 20th

-

Generate e-way bills for all goods movement

Quarterly/Annual

-

Review all pending invoices in IMS

-

Verify no registration risk flags

-

Ensure all amendments done via GSTR-1A

-

Prepare for annual return (GSTR-9)

Tools to Help

-

Use India Tax Tools’ GST Calculator for accurate tax computation

-

Invoice Generator for compliant invoices

-

GSTIN Verification Tool to validate customer GSTIN before invoicing

-

ITC Reconciliation Tool to match purchase invoices

-

GST Due Date Calendar for reminders

CONCLUSION: STAY COMPLIANT, STAY AHEAD

The GST rules for 2026 represent a significant shift toward automated enforcement and stricter compliance. The system is now designed to act instantly—suspending registrations, blocking returns, and preventing ITC claims without manual intervention.

But these changes also bring benefits:

-

Faster processing for genuine taxpayers

-

Reduced fraud (biometric verification)

-

Clearer ITC (IMS ensures only valid claims)

-

Better compliance culture

Your Action Plan

- Understand the new rules – especially auto-suspension and IMS

- Update your systems – bank details, MFA, return tracking

- Train your team – on IMS acceptance/rejection workflow

- File on time – every month, without fail

- Use technology – leverage tools like India Tax Tools to automate compliance

Remember

-

Two missed GSTR-3B = automatic suspension

-

Bank details must be updated within 30 days

-

IMS puts you in control of your ITC

-

Three-year rule means no old returns later

-

MFA keeps your account secure

Stay compliant, stay ahead, and let these rules work for your business.

“GST in 2026 is automated, strict, and unforgiving. File on time, update your bank details, and embrace IMS—or watch your business grind to a halt.”

Disclaimer: This article is for informational and educational purposes only. GST rules, notifications, and due dates are subject to change based on government and GST Council decisions. Please consult your Chartered Accountant or GST practitioner for advice tailored to your specific business circumstances. The information provided is based on GST updates available as of February 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment