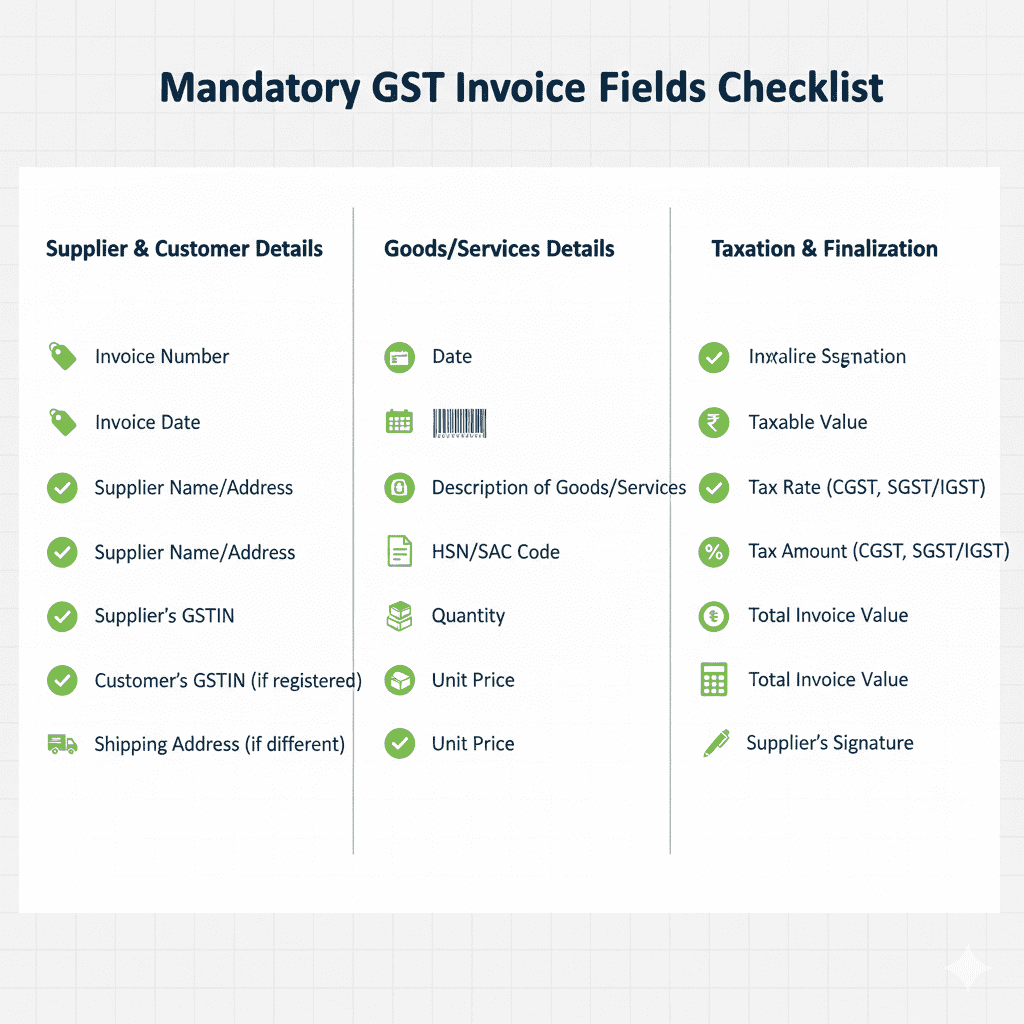

Sample GST Invoice Format

TAX INVOICE

ABC TRADERS

123, MG Road, Pune - 411001

GSTIN: 27ABCDE1234F1Z5

Invoice No: INV/24-25/001 Date: 15-Oct-2024

Buyer (B2B):

XYZ RETAILERS

456, Linking Road, Mumbai - 400001

GSTIN: 27PQRST5678H2Z3

Place of Supply: Maharashtra (27)

| Sr | HSN | Description | Qty | Unit Price | Value | Discount | Taxable |

|----|-----|-------------|-----|------------|-------|----------|---------|

| 1 | 8517 | Smartphone | 10 | 15,000 | 1,50,000 | 5,000 | 1,45,000 |

Tax Calculation:

CGST @ 9%: ₹13,050

SGST @ 9%: ₹13,050

Total Tax: ₹26,100

Invoice Total: ₹1,71,100

Bank Details: HDFC Bank, A/c: 50100234567890, IFSC: HDFC0001234

For ABC Traders

(Authorised Signatory)

B2B VS B2C INVOICES: KEY DIFFERENCES

The rules differ based on who your customer is.

B2B Invoice (Registered Customer)

Critical: If customer provides wrong GSTIN, their ITC gets blocked, and they’ll reject your invoice. Always verify GSTIN on GST portal before invoicing.

B2C Invoice (Unregistered Customer)

Special Rule: For inter-state B2C supplies exceeding ₹2.5 lakh in value, you must collect customer’s address and PIN code to determine place of supply .

Example Scenarios

HSN/SAC CODES: GETTING THEM RIGHT

HSN (Harmonized System of Nomenclature) for goods and SAC (Service Accounting Codes) for services determine tax rates. Wrong codes = wrong tax = notices.

HSN/SAC Digit Requirements by Turnover

*Source: Notification No. 12/2024 – Central Tax *

Common HSN/SAC Mistakes

How to Find Correct Codes

Use India Tax Tools’ HSN/SAC Code Finder:

- Search by product/service name

- Get accurate 4/6/8 digit codes

- View applicable tax rates

- Download product master with codes

Pro Tip: Maintain a product master in your accounting software with HSN/SAC codes mapped to each item. This prevents manual entry errors.

E-INVOICING RULES FOR 2026

E-invoicing isn’t about generating invoices electronically—it’s about reporting them to the government’s Invoice Registration Portal (IRP) for a unique Invoice Reference Number (IRN).

Who Must Comply in 2026?

*Source: CBIC Notification 01/2025 *

E-Invoice Process

- Generate invoice in your accounting software (with mandatory fields)

- Upload JSON to IRP (GST portal or authorized GSP)

- IRP validates and generates:

-

IRN (unique hash)

-

Signed QR code

-

Download validated invoice with IRN and QR code

-

Share this with customer

E-Invoice Mandatory Fields

Same as regular invoice PLUS:

Benefits of E-Invoicing

QR Code Requirements

For B2C invoices from e-invoice-enabled businesses, QR code must contain:

-

GSTIN of supplier

-

Invoice number and date

-

Total taxable value

-

Total IGST/CGST/SGST

SPECIAL INVOICING SCENARIOS

Scenario 1: Composition Scheme Dealers

Composition dealers cannot charge GST. They issue Bill of Supply instead of tax invoice.

Bill of Supply Features:

-

No tax amount shown

-

No ITC available to recipient

-

Must mention “composition taxable person”

-

Still requires most other fields

Scenario 2: Exports

Export invoices are zero-rated but require:

-

Shipping Bill number and date (for goods)

-

Let Export Order (LEO) reference

-

IGST shown as 0% (with “supply meant for export” declaration)

-

Place of supply: Location outside India

Scenario 3: Reverse Charge Mechanism (RCM)

When recipient is liable to pay GST (e.g., goods transport, specified services):

-

Supplier issues invoice without charging GST

-

Invoice must mention: “Tax payable under reverse charge”

-

Recipient uses this to pay tax and claim ITC

Scenario 4: Multiple GST Registrations

If you have separate GSTINs for different states:

-

Issue separate invoices from each GSTIN

-

Cannot issue one invoice covering multiple states

-

Interstate supply between own branches is taxable

BEST PRACTICES FOR GST-COMPLIANT INVOICING

Do’s ✅

- Use sequential numbering – No gaps, unique for financial year

- Verify customer GSTIN – Check on GST portal before invoicing

- Maintain product master – With correct HSN/SAC and tax rates

- Show discounts separately – Reduces disputes on taxable value

- Include bank details – Faster payments, proof for reconciliation

- Mention place of supply – Especially for inter-state

- Generate invoices promptly – Within 30 days (goods) / 45 days (services)

- Backup invoices digitally – 6 years mandatory retention

Don’ts ❌

- Don’t issue invoice without GSTIN if registered

- Don’t mix taxable and exempt supplies in one line

- Don’t round tax amounts – Calculate precisely

- Don’t use informal names – Legal names only

- Don’t forget reverse charge declarations

- Don’t issue duplicate numbers

- Don’t invoice before goods dispatched (for goods)

Monthly Checklist

-

All invoices have unique numbers

-

GSTINs verified for all B2B customers

-

HSN/SAC codes match product master

-

Tax rates checked (CGST/SGST/IGST)

-

Place of supply correct for inter-state

-

E-invoice IRN generated (if applicable)

-

Invoices match GSTR-1 entries

COMMON INVOICING MISTAKES & THEIR CONSEQUENCES

Real Example

A Mumbai-based trader issued an invoice to a Delhi customer but mentioned “Maharashtra” as place of supply. He charged CGST+SGST instead of IGST. Result:

Total cost of one wrong field: ₹63,100 + customer relationship damage.

DIGITAL TOOLS FOR ERROR-FREE INVOICING

Manual invoicing is risky and time-consuming. Leverage technology.

India Tax Tools for GST Invoicing

Features of India Tax Tools Invoice Generator

-

Auto-population of mandatory fields

-

Tax calculation (CGST/SGST/IGST)

-

HSN/SAC lookup integrated

-

Multiple formats (B2B, B2C, exports)

-

Download as PDF/Excel

-

100% free – no registration required

-

Privacy safe – all calculations in browser

Try it now: Create your GST invoice in 30 seconds

FREQUENTLY ASKED QUESTIONS

Q1: What is the time limit for issuing a GST invoice?

*Source: Section 31, CGST Act *

Q2: Can I issue a consolidated invoice for multiple deliveries?

Yes, for continuous supply of goods/services, you can issue a consolidated invoice at the end of each month (or sooner if payment received). Each delivery must be documented separately.

Q3: Is digital signature mandatory on GST invoices?

No for most businesses. Digital signature is required only for:

Physical signature or stamped signature is acceptable for others.

Q4: What is the penalty for incorrect GST invoices?

Penalties under Section 122 of CGST Act:

-

₹10,000 per invoice for issuing incorrect invoice

-

100% tax amount (if tax evasion involved)

-

Suspension/cancellation of GSTIN for repeated offenses

Q5: Can I amend an invoice after issuing?

No. Once issued, an invoice cannot be amended. Corrections must be made through:

-

Credit note (for reducing value/tax)

-

Debit note (for increasing value/tax)

-

Revised invoice (only within 1 month of registration)

Q6: What is the difference between tax invoice and bill of supply?

Q7: Do I need to mention HSN code on every invoice?

HSN/SAC code requirement depends on turnover (see Section 5). However, it’s best practice to include HSN even if optional, as it prevents rate errors and helps customers.

Q8: How long should I keep GST invoices?

6 years from the due date of annual return for that year . Store digitally to save space and enable easy retrieval during audits.

Q9: Can I issue invoice in a language other than English/Hindi?

Yes, but you must provide a translation in English or Hindi if required by tax authorities.

Q10: What is the rule for interstate B2C invoices above ₹2.5 lakh?

For interstate supplies to unregistered persons exceeding ₹2.5 lakh:

-

Collect customer’s name, address, and PIN code

-

Mention place of supply (based on PIN code)

-

Charge IGST (not CGST+SGST)

-

Issue invoice with all B2B-like fields except GSTIN

ACTIONABLE CHECKLIST: BEFORE YOU ISSUE AN INVOICE

Daily/Per Invoice Checks

-

Invoice number unique and sequential

-

Date is current (not future-dated)

-

Your GSTIN is correct and active

-

Customer GSTIN verified (for B2B) using GSTIN Verification Tool

-

HSN/SAC code matches product/service (use Code Finder)

-

Place of supply correctly mentioned (for inter-state)

-

Tax rate applied correctly (CGST+SGST or IGST)

-

Tax amounts calculated accurately

-

Total matches item values + tax

-

Bank details included

-

Signature/stamp applied

Monthly Reconciliation Checks

-

All invoices entered in GSTR-1

-

Invoice totals match GSTR-1 summary

-

E-invoice IRNs generated (if applicable)

-

No gaps in invoice numbering

-

Credit/debit notes issued for corrections

-

ITC claimed by customers not rejected (check GSTR-2B)

Quarterly/Annual Checks

-

HSN/SAC code summary matches returns

-

Export invoices have shipping bill references

-

Reverse charge invoices correctly documented

-

All invoices backed up digitally

-

Obsolete product codes updated

CONCLUSION: MASTER YOUR GST INVOICES

The GST-compliant invoice is more than a piece of paper—it’s the foundation of your tax compliance, customer trust, and business efficiency. A correct invoice ensures:

-

Smooth ITC claims for your customers

-

Accurate GST returns with no mismatches

-

Faster payments (no rejections)

-

Peace of mind during audits

The rules are detailed, but they’re not complicated when broken down:

- Include all mandatory fields (use the checklist)

- Get codes right (HSN/SAC, GSTIN, place of supply)

- Follow format rules (B2B vs B2C, e-invoice if applicable)

- Use technology to eliminate manual errors

Your Next Steps

-

Bookmark this guide and use the checklist before every invoice

-

Try India Tax Tools’ Invoice Generator for error-free invoices in 30 seconds

-

Verify customer GSTINs using the free verification tool

-

Set up product master with correct HSN/SAC codes

-

Share this guide with your accounts team and fellow business owners

Remember: Every correct invoice is a step toward stress-free compliance. Start today.

“Your invoice is your business’s handshake with the tax department. Make it firm, clear, and legally perfect—or pay the price of a weak grip.”

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice. GST laws, rules, and formats are subject to change based on government notifications and GST Council decisions. Please consult a qualified Chartered Accountant or GST practitioner for advice tailored to your specific business circumstances. The information provided is based on GST rules and updates available as of February 2026.