Meet Priya, who runs a small handmade jewelry business in Jaipur with ₹35 lakh annual turnover. She’s heard about “MSME benefits” but isn’t sure what applies to her. Then there’s Ramesh, a Pune-based auto component manufacturer with 25 employees and ₹8 crore turnover, struggling with cash flow and wondering if government schemes can help. Both are asking: “What tax benefits can MSMEs really claim in 2026?”

You’re not alone. India has over 6.3 crore MSMEs, contributing 30% to GDP and employing 11 crore people . Yet a 2025 survey found that 62% of small business owners were unaware of at least three major tax benefits they qualified for .

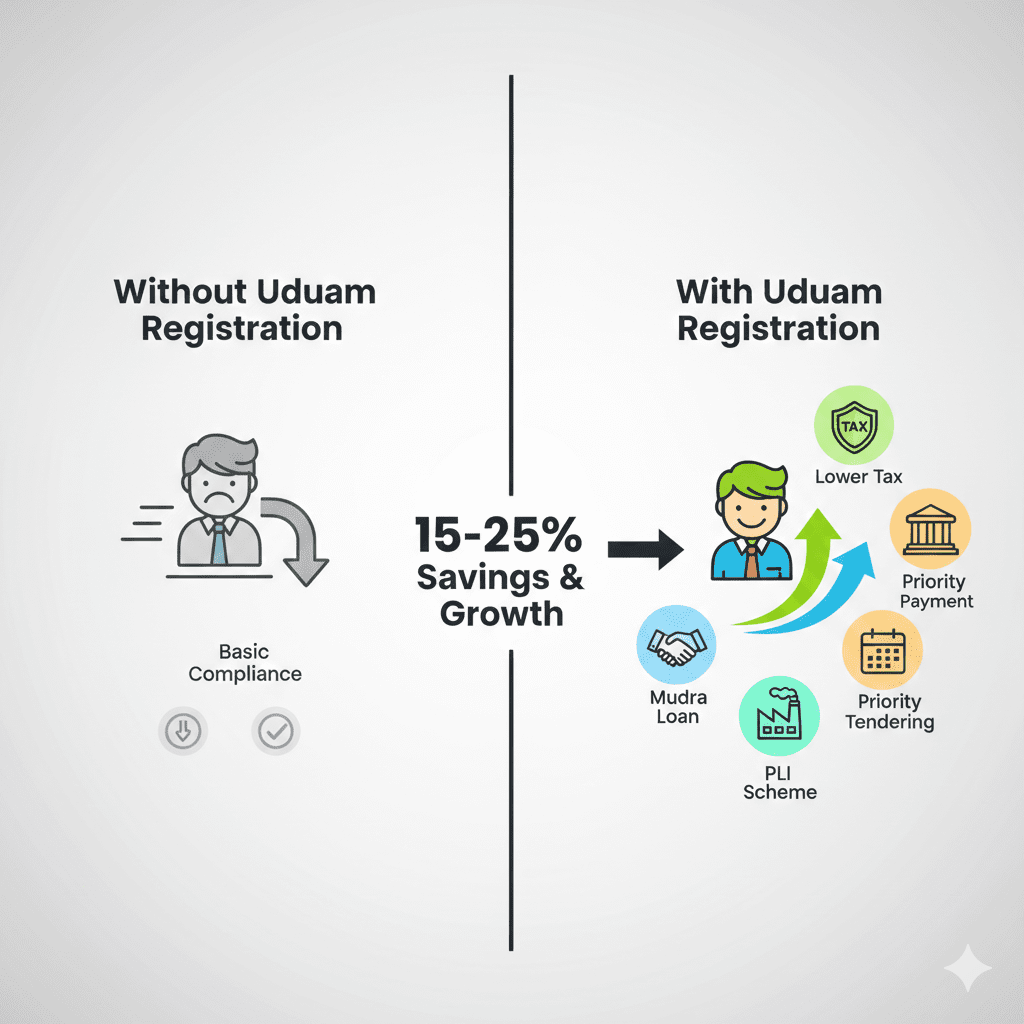

Here’s the good news: Budget 2026 and recent MSME announcements have expanded benefits significantly—higher presumptive taxation limits, extended producer credit periods, and new manufacturing incentives. A properly structured MSME can save 15-25% on effective tax rate compared to regular businesses .

In this complete guide, you’ll discover:

-

Updated MSME classification for 2026 (investment + turnover criteria)

-

8 major tax benefits available (with real savings examples)

-

New schemes: presumptive taxation limit ₹3 crore, 45-day payment rule

-

Step-by-step eligibility checklist

-

Common mistakes that disqualify benefits

-

How to use tools like India Tax Tools’ MSME Benefits Calculator to optimize

Let’s unlock your business’s tax-saving potential.

WHO IS AN MSME IN 2026? UPDATED CLASSIFICATION

Before claiming benefits, you must know whether your business qualifies as an MSME. The classification was revised in 2020 and remains applicable for 2026, with minor clarifications.

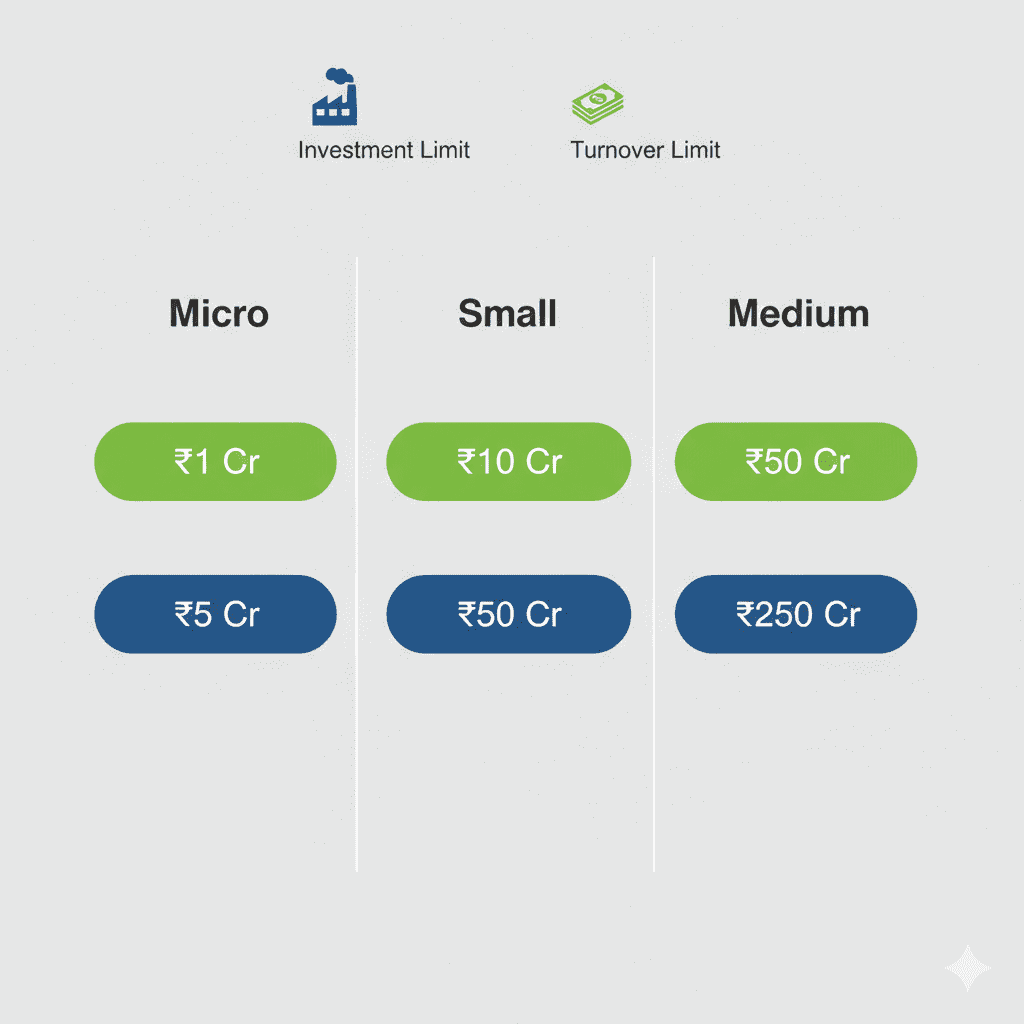

MSME Classification Criteria (As per MSMED Act, 2006 amended 2020)

| Enterprise Type | Investment in Plant & Machinery/Equipment | Annual Turnover |

|---|---|---|

| Micro | Not exceeding ₹1 crore | Not exceeding ₹5 crore |

| Small | Not exceeding ₹10 crore | Not exceeding ₹50 crore |

| Medium | Not exceeding ₹50 crore | Not exceeding ₹250 crore |

*Source: Ministry of MSME, Government of India *

Key Points to Understand

- Composite Criteria: Both investment and turnover are considered. Exceeding either limit moves you to next category

- Investment Calculation: Includes cost of plant, machinery, and equipment (excluding land and building)

- Turnover Calculation: Based on total business turnover, not profit

- Export Exclusion: Export turnover is excluded for classification purposes

- Udyam Registration: Mandatory for claiming benefits—registration is free on Udyam portal

Example

| Business | Investment | Turnover | MSME Category |

|---|---|---|---|

| Priya’s Jewelry | ₹45 lakh | ₹35 lakh | Micro (both under limits) |

| Ramesh’s Auto Parts | ₹8 crore | ₹45 crore | Small (investment under ₹10cr, turnover under ₹50cr) |

| A unit crossing both limits | ₹12 crore | ₹60 crore | Medium |

Important: Classification determines which benefits apply. Micro units get higher presumptive taxation limits, while medium units qualify for PLI schemes.

Udyam Registration: Your Gateway to Benefits

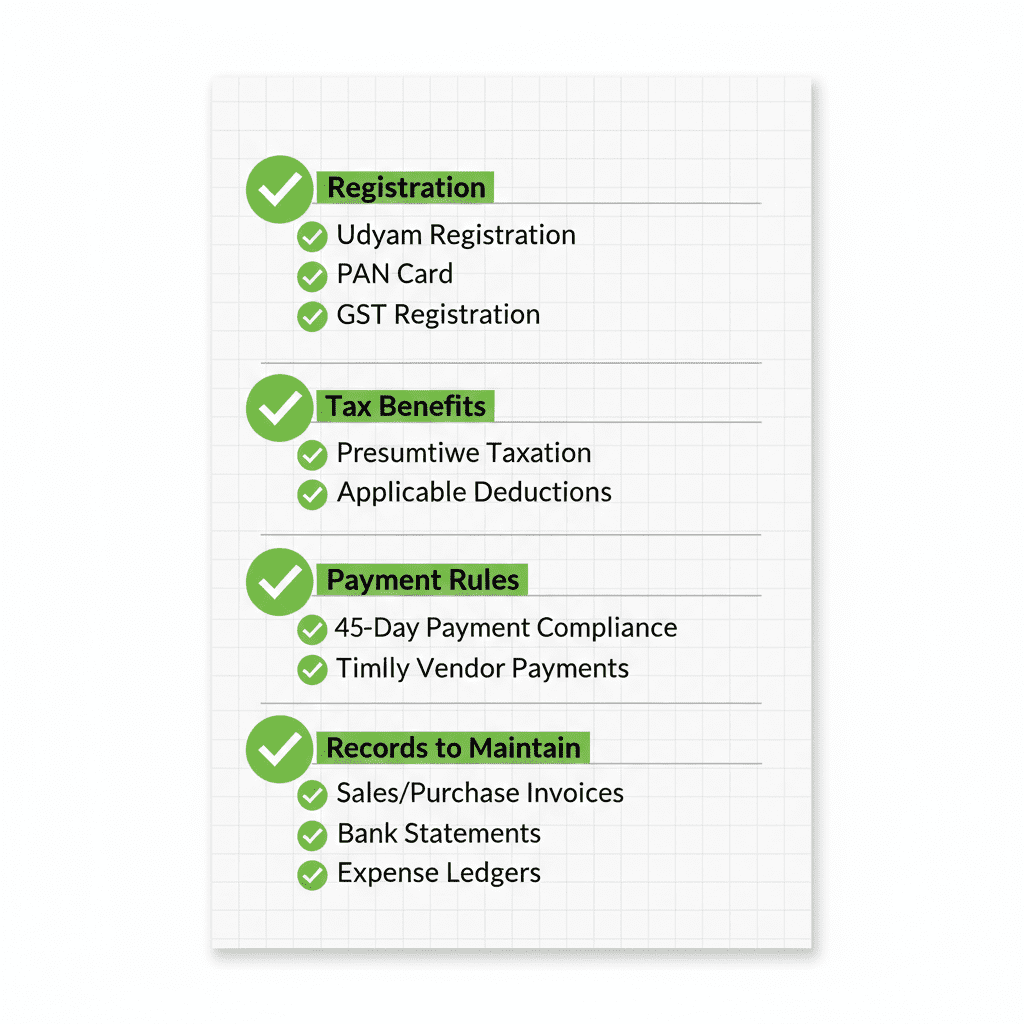

Udyam Registration (formerly Udyog Aadhaar) is mandatory to claim MSME benefits . It’s a 12-digit Unique Identity Number (UIN) obtained online.

Documents Required:

-

Aadhaar (of proprietor/managing partner/authorized signatory)

-

PAN card (business)

-

Bank account details

-

Business address proof

-

GSTIN (if applicable)

How to Register:

- Visit https://udyamregistration.gov.in

- Fill Aadhaar details, verify with OTP

- Enter business details (name, type, investment, turnover)

- Submit and get instant registration certificate

Pro Tip: Use India Tax Tools’ MSME Eligibility Checker to determine your category before registration.

MAJOR MSME TAX BENEFITS IN 2026

Here are the most valuable tax benefits available to MSMEs for FY 2025-26 (AY 2026-27).

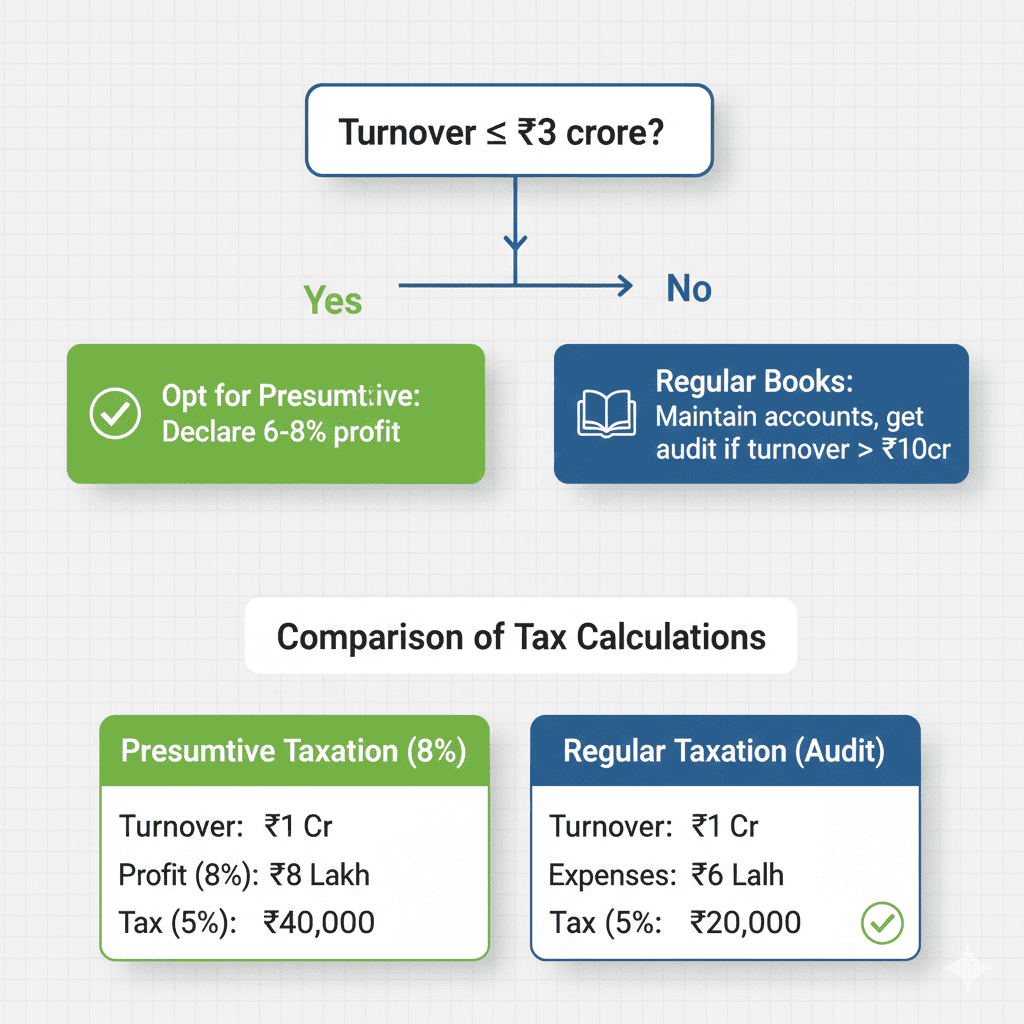

Benefit 1: Presumptive Taxation under Section 44AD (Expanded Limit)

What It Is: Instead of maintaining detailed books and getting accounts audited, small businesses can declare income at a prescribed rate of 8% (6% for digital receipts) of turnover.

2026 Update: The turnover limit for presumptive taxation has been increased from ₹2 crore to ₹3 crore for businesses receiving payments digitally .

| Aspect | Old Limit | New Limit (2026) |

|---|---|---|

| Maximum Turnover | ₹2 crore | ₹3 crore |

| Presumed Profit (Cash) | 8% | 8% |

| Presumed Profit (Digital) | 6% | 6% |

| Audit Required? | No | No (up to ₹3cr) |

Savings Example: A business with ₹2.5 crore turnover, actual profit 5% (₹12.5 lakh). Under presumptive scheme, they declare 6% (₹15 lakh) on digital receipts. Tax on ₹15 lakh instead of actual profit—beneficial if actual profit is lower than prescribed rates.

Benefit 2: Section 44ADA for Professionals (Limit Increased)

For professionals (doctors, lawyers, architects, freelancers) with turnover up to ₹75 lakh (increased from ₹50 lakh), income is presumed at 50% of gross receipts .

Who Qualifies: Specified professions under Section 44AA(1) plus any profession notified by CBDT.

Benefit 3: Lower Corporate Tax Rate (Section 115BAB)

Manufacturing MSMEs set up after October 2019 can opt for 15% corporate tax rate (plus surcharge and cess) subject to conditions.

| Tax Regime | Tax Rate | Surcharge | Effective Rate |

|---|---|---|---|

| New Manufacturing | 15% | 10% (if income > ₹1cr) | ~17.16% |

| Regular Corporate | 25% | 7-12% | ~27-30% |

Eligibility: Must be new manufacturing unit, commence production by March 31, 2024 (extended to 2025 for some sectors).

Benefit 4: Extended Credit Period for MSME Buyers

New Rule from 2026: Under Section 43B(h), payments to MSME suppliers must be made within 45 days to claim deduction . If payment is delayed beyond 45 days, the amount is deductible only when actually paid—not on accrual basis.

Impact: This encourages large companies to pay MSMEs on time, improving cash flow.

Benefit 5: Higher Deduction for Interest on Late Payments (Section 23 of MSMED Act)

Buyers who delay payments to MSMEs beyond agreed credit period must pay interest at compound interest with monthly rests—at three times the bank rate . This interest is taxable for MSMEs but provides negotiating power.

Benefit 6: Collateral-Free Loans Under CGTMSE

While not directly tax-related, Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) provides collateral-free loans up to ₹5 crore . Lower interest burden = higher taxable profit, but better cash flow.

Benefit 7: Exemption from TDS on Certain Payments

MSMEs with valid Udyam registration may be eligible for lower TDS deduction rates under Section 194M and related provisions, though specific thresholds apply.

Benefit 8: Priority in Government Tenders

MSMEs registered on Udyam portal get:

-

Exemption from earnest money deposit

-

Exemption from tender fee

-

15% price preference in certain categories

-

25% mandatory procurement from MSMEs by central ministries

NEW SCHEMES AND UPDATES FOR 2026

Budget 2026 and recent policy announcements have introduced several MSME-specific benefits.

Scheme 1: Enhanced Mudra Loan Limits

| Loan Category | Old Limit | New Limit (2026) |

|---|---|---|

| Shishu | ₹50,000 | ₹1 lakh |

| Kishor | ₹5 lakh | ₹10 lakh |

| Tarun | ₹10 lakh | ₹20 lakh |

*Source: PM Mudra Yojana updates *

Scheme 2: Production Linked Incentive (PLI) for MSMEs

PLI schemes now cover 14 sectors with specific MSME sub-limits. Benefits include:

-

Incentives of 4-15% on incremental sales

-

Lower effective tax rate due to higher profits

-

Mandatory Udyam registration for application

Scheme 3: Revised Definition of MSME for Benefits

While classification remains same, certain schemes now use turnover-only criteria for easier eligibility:

-

Micro: Turnover ≤ ₹5 crore (investment criteria relaxed for some benefits)

-

Small: Turnover ≤ ₹50 crore

-

Medium: Turnover ≤ ₹250 crore

Scheme 4: Digital Payment Incentives

To encourage digital transactions, MSMEs receiving >95% payments digitally get:

-

Lower presumptive rate (6% instead of 8%)

-

Higher Mudra loan limits

-

Priority in government tenders

Scheme 5: MSME Samadhaan Portal Integration

The delayed payment monitoring portal now integrates with Income Tax portal. Large companies delaying payments to MSMEs face:

-

Automatic disallowance of expense under Section 43B(h)

-

Higher scrutiny in tax assessments

STEP-BY-STEP GUIDE TO OPTIMIZE MSME TAX BENEFITS

Follow this action plan to maximize your tax savings.

Step 1: Get Udyam Registration

-

Register on https://udyamregistration.gov.in

-

Keep registration number ready for all benefit claims

-

Update registration annually with turnover/investment changes

Step 2: Choose Between Presumptive and Regular Taxation

| Your Situation | Likely Better Choice |

|---|---|

| Actual profit < 6-8% of turnover | Regular books (show lower profit) |

| Actual profit > 8% | Presumptive (declare 6-8%) |

| Turnover < ₹3 crore, mostly digital | Presumptive (6% rate) |

| Need loans (banks prefer audited books) | Regular (audited statements) |

| Have losses to carry forward | Regular (need books for loss) |

Use India Tax Tools’ MSME Tax Optimizer to compare both scenarios instantly.

Step 3: Structure Business Payments

-

Ensure payments to MSME suppliers made within 45 days

-

Get written agreements with buyers specifying credit period

-

Register all invoices on MSME Samadhaan portal if delayed

Step 4: Claim All Eligible Deductions

| Deduction Type | Section | Maximum Limit |

|---|---|---|

| Depreciation | 32 | As per rates |

| Scientific Research | 35 | 100-150% |

| Startup Expenses | 35D | 20% of capital (5 years) |

| Family Planning Promotion | 36(1)(ix) | Actual expenditure |

| Bad Debts | 36(1)(vii) | If written off in books |

Step 5: Maintain Proper Records

Even under presumptive scheme, maintain:

-

Invoices and bills

-

Bank statements

-

Udyam registration certificate

-

GST returns (if applicable)

-

Payment proofs for digital transactions

COMMON MISTAKES THAT DISQUALIFY MSME BENEFITS

Avoid these pitfalls that lead to benefit denial or tax notices.

Mistake 1: Not Updating Udyam Registration

Problem: Registration not updated with current turnover/investment. Benefits claimed based on outdated category.

Fix: Update registration annually or whenever crossing thresholds.

Mistake 2: Claiming Presumptive Benefits Without Conditions

Conditions for Section 44AD:

-

Turnover ≤ ₹3 crore

-

No deductions under 80-80U allowed

-

Cannot have income from profession under 44ADA

-

Must file ITR-3 or ITR-4 accordingly

Mistake 3: Mixing Presumptive and Regular Income

If you opt for presumptive for business income, you cannot claim separate deductions for that business. All business expenses are deemed covered in the 6-8% profit rate.

Mistake 4: Ignoring Section 44AD(4) – Five-Year Rule

If you opt for presumptive taxation for 5 years, you must remain in it for 5 consecutive years. Exiting earlier means:

-

Cannot opt for presumptive for next 5 years

-

All past benefits may be reopened

Mistake 5: Not Maintaining 45-Day Payment Records

Under Section 43B(h), payments delayed beyond 45 days to MSMEs are disallowed in buyer’s books. As MSME seller, maintain proof of:

-

Invoice date

-

Payment receipt date

-

Udyam registration of your business (to prove MSME status)

Mistake 6: Claiming Lower TDS Without Proper Documentation

To get lower TDS rates, provide:

-

Udyam certificate to deductor

-

Form 15G/15H if applicable

-

PAN and GST details

COMPARISON TABLES FOR QUICK REFERENCE

Table 1: MSME Tax Benefits at a Glance

| Benefit | Section/Scheme | Eligibility | Maximum Benefit |

|---|---|---|---|

| Presumptive Taxation | 44AD | Turnover ≤ ₹3 crore | No audit, 6-8% profit rate |

| Lower Corporate Tax | 115BAB | New mfg units (by 2024-25) | ~17% effective rate |

| 45-Day Payment Rule | 43B(h) | All MSME suppliers | Timely payments |

| Mudra Loans | PMMY | All MSMEs | Up to ₹20 lakh |

| PLI Incentives | Various | Sector-specific | 4-15% on sales |

| Tender Preferences | Public Procurement | Udyam registered | 15% price preference |

| CGTMSE Guarantee | Credit Guarantee | Micro & Small | ₹5 crore collateral-free |

Table 2: Presumptive Taxation Limits Comparison

| Category | Old Limit (FY 2023-24) | New Limit (FY 2025-26) | Profit Rate |

|---|---|---|---|

| Business (44AD) | ₹2 crore | ₹3 crore | 6% (digital) / 8% (cash) |

| Profession (44ADA) | ₹50 lakh | ₹75 lakh | 50% of gross receipts |

| Specified Professionals | ₹50 lakh | ₹75 lakh | 50% of gross receipts |

Table 3: Udyam Registration Requirements by Business Type

| Business Type | Document 1 | Document 2 | Document 3 |

|---|---|---|---|

| Proprietorship | Aadhaar of proprietor | PAN of proprietor | Bank account proof |

| Partnership Firm | Aadhaar of managing partner | PAN of firm | Partnership deed |

| Private Limited | Aadhaar of director | PAN of company | Incorporation certificate |

| LLP | Aadhaar of designated partner | PAN of LLP | LLP agreement |

| HUF | Aadhaar of Karta | PAN of HUF | HUF deed |

FREQUENTLY ASKED QUESTIONS

Q1: What is the turnover limit for MSME status in 2026?

The classification limits remain: Micro (₹5 crore), Small (₹50 crore), Medium (₹250 crore) turnover. Investment limits also apply—see table in Section 2 .

Q2: Is Udyam registration mandatory for MSME tax benefits?

Yes. Without valid Udyam registration, you cannot claim most MSME-specific benefits like presumptive taxation (higher limits), 45-day payment protection, or priority in tenders .

Q3: What is Section 43B(h) and how does it affect MSMEs?

Section 43B(h) disallows deduction for payments made to MSMEs beyond 45 days in the buyer’s books. For MSMEs, this means:

-

You get paid faster

-

Maintain proof of Udyam registration to enforce this

-

Register on MSME Samadhaan portal for delayed payments

Q4: Can a professional (doctor, lawyer) claim MSME benefits?

Yes. Professionals with turnover up to ₹75 lakh can claim presumptive taxation under Section 44ADA at 50% of gross receipts . They must register as MSME if they meet investment/turnover criteria.

Q5: What is the difference between Section 44AD and 44ADA?

| Aspect | Section 44AD | Section 44ADA |

|---|---|---|

| Applies to | Business (trading, manufacturing) | Specified professions |

| Turnover Limit | ₹3 crore | ₹75 lakh |

| Presumed Profit | 6-8% | 50% |

| Audit Required? | No | No |

Q6: How do I calculate investment for MSME classification?

Include cost of plant, machinery, and equipment (excluding land and building). For service enterprises, include equipment cost. Use:

-

Original cost (not depreciated value)

-

Exclude furniture, vehicles (unless integral to business)

-

Include both owned and leased assets (if capitalized)

Q7: Can I switch between presumptive and regular taxation?

You can opt for presumptive any year if eligible. But once you opt for presumptive, you must continue for 5 consecutive years . Early exit means no presumptive for next 5 years.

Q8: What records should MSMEs maintain for tax purposes?

Even under presumptive, maintain:

-

Sales and purchase invoices

-

Bank statements

-

Udyam registration certificate

-

Proof of digital receipts (for 6% rate)

-

Payment proofs for expenses

-

Stock register (if applicable)

Q9: Are MSMEs exempt from audit?

Not automatically. Audit required if:

-

Turnover > ₹10 crore (regular businesses)

-

Under presumptive, no audit up to ₹3 crore

-

If claiming losses, may need audit regardless

Q10: How does the 45-day payment rule work for exports?

The rule applies to payments for goods/services received by MSMEs. For exports, if the buyer is outside India, Section 43B(h) may not apply directly, but FEMA and RBI guidelines govern export payments .

ACTIONABLE CHECKLIST: OPTIMIZE YOUR MSME TAX BENEFITS

Before March 31, 2026 (Year-End Planning)

-

Check Udyam registration status – update if expired

-

Calculate turnover and investment – confirm MSME category

-

If turnover < ₹3 crore, evaluate presumptive taxation (Section 44AD)

-

Compare tax under presumptive vs regular using India Tax Tools’ MSME Optimizer

-

For professionals, check eligibility for Section 44ADA (₹75 lakh limit)

-

Review all payments to MSME suppliers – ensure within 45 days

-

Register delayed payments on MSME Samadhaan portal

-

If manufacturing, check PLI scheme eligibility

During ITR Filing (July-September 2026)

-

Choose correct ITR form:

-

ITR-3: Regular business income

-

ITR-4: Presumptive taxation (44AD/44ADA)

-

-

Report Udyam registration number (if applicable)

-

Claim all eligible deductions:

-

Depreciation (if regular books)

-

Section 35 (scientific research)

-

Section 35D (preliminary expenses)

-

-

Verify TDS credits in Form 26AS

-

For digital receipts >95%, claim 6% presumptive rate

-

File on or before due date (avoid late fees)

Year-Round Compliance

-

Maintain Udyam registration (update annually)

-

Track all invoices with MSME buyers

-

Issue timely invoices with clear payment terms

-

For large receivables, use MSME Samadhaan portal

-

Keep digital payment proofs for lower presumptive rate

-

Review eligibility for new schemes quarterly

SUCCESS STORY: HOW A MICRO UNIT SAVED ₹2.3 LAKH

Business: Sharma Electronics, a Delhi-based trading business

Turnover: ₹2.4 crore (FY 2025-26)

Nature: B2B and B2C sales of electronic components

Employees: 4

Before Optimization

-

Filed regular returns with audited books

-

Actual profit: ₹14.2 lakh (5.9% of turnover)

-

Tax paid: ₹4.1 lakh (including surcharge)

-

Audit cost: ₹25,000 annually

After MSME Optimization

-

Udyam Registration: Registered as Micro enterprise

-

Presumptive Taxation: Opted for Section 44AD (digital receipts)

-

Digital Push: Increased digital receipts to 96% of turnover

-

Declared Profit: 6% of ₹2.4 crore = ₹14.4 lakh

Result

| Parameter | Before | After | Change |

|---|---|---|---|

| Declared Profit | ₹14.2 lakh | ₹14.4 lakh | +₹20,000 |

| Tax Payable | ₹4.1 lakh | ₹2.8 lakh | -₹1.3 lakh |

| Audit Cost | ₹25,000 | Nil | -₹25,000 |

| Compliance Time | 40 hours | 10 hours | -75% |

| Total Savings | – | ₹1.55 lakh | – |

Plus, they now qualify for:

-

Mudla loans up to ₹20 lakh (expansion planned)

-

Priority in government tenders

-

45-day payment protection from corporate buyers

“I wish I’d known about this earlier. The same profit, less tax, and no audit headache. It’s not tax evasion—it’s smart planning.” – Mr. Sharma, Proprietor

CONCLUSION: YOUR MSME, MAXIMIZED

MSME tax benefits in 2026 offer unprecedented opportunities for small businesses to reduce tax burden, improve cash flow, and scale operations. From the expanded presumptive taxation limit of ₹3 crore to the powerful 45-day payment protection under Section 43B(h), the government has created a framework that genuinely supports small enterprises.

But here’s the truth: these benefits don’t apply automatically. You must:

-

Register under Udyam

-

Choose the right tax regime for your situation

-

Comply with conditions (45-day payments, digital receipts)

-

Review eligibility regularly as your business grows

The effort is worth it. A typical MSME can save:

-

15-25% on effective tax rate

-

₹25,000-50,000 in audit costs (if under presumptive)

-

Weeks of compliance time annually

-

Significant interest through timely payments

Your Next Steps

-

Get Udyam registered today if you haven’t—it’s free and takes 15 minutes

-

Use India Tax Tools’ MSME Benefits Calculator to estimate your savings

-

Review your payment terms with all buyers—enforce 45-day rule

-

Share this guide with fellow business owners

-

Consult a CA for personalized advice, especially if crossing thresholds

Your MSME isn’t just a business—it’s part of India’s economic backbone. Claim the benefits you deserve, stay compliant, and grow with confidence.

“MSME benefits aren’t charity—they’re the government’s recognition that small businesses drive India’s economy. Register, claim, comply, and grow. The tax savings are your reward for being part of this ecosystem.”

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice. Tax laws, MSME classifications, and scheme details are subject to change based on government notifications. Please consult a qualified Chartered Accountant or MSME consultant for advice tailored to your specific business circumstances. The information provided is based on MSME rules, Budget 2026 announcements, and tax provisions available as of February 2026.