If retirement feels like a distant, fuzzy concept, you’re not alone. But here’s a wake-up call: only 24% of urban Indians feel confident about their retirement savings, according to a 2025 survey. Meanwhile, the National Pension System (NPS) has quietly emerged as one of India’s most powerful retirement tools—with over 6.3 crore subscribers and assets under management exceeding ₹11 lakh crore .

What makes NPS special? It’s the only investment in India offering triple tax benefits:

-

Entry tax benefit: Deduction on your investments

-

Growth tax benefit: Compounding without tax

-

Exit tax benefit: Tax-free withdrawal at maturity (partially)

In this complete 2026 guide, you’ll discover:

-

How NPS works (simplified, with examples)

-

Triple tax benefits decoded—Section 80CCD(1), 80CCD(1B), and 80CCD(2)

-

NPS vs other retirement options—side-by-side comparison

-

Return-maximizing strategies—choose the right fund manager and asset allocation

-

Tier 1 vs Tier 2 accounts—which you need (and when)

-

Real examples—how much tax you save at different income levels

-

Common mistakes that cost you thousands

Let’s unlock the power of NPS for your retirement.

WHAT IS NPS AND HOW DOES IT WORK?

The National Pension System (NPS) is a government-sponsored retirement savings scheme, regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Think of it as a long-term wealth-building vehicle designed specifically for your retirement years.

Key Features at a Glance

| Feature | Description |

|---|---|

| Launched | 2004 (for government employees), 2009 (for all citizens) |

| Regulator | PFRDA (Pension Fund Regulatory and Development Authority) |

| Eligibility | Any Indian citizen aged 18-70 |

| Account Types | Tier 1 (Retirement account) and Tier 2 (Voluntary savings) |

| Minimum Contribution | Tier 1: ₹500 annually; Tier 2: ₹1,000 (varies by POP) |

| Lock-in | Tier 1: Until age 60 (partial withdrawal allowed); Tier 2: None |

| Tax on Maturity | 60% tax-free withdrawal; 40% annuity (taxable) |

*Source: PFRDA, NPS Trust *

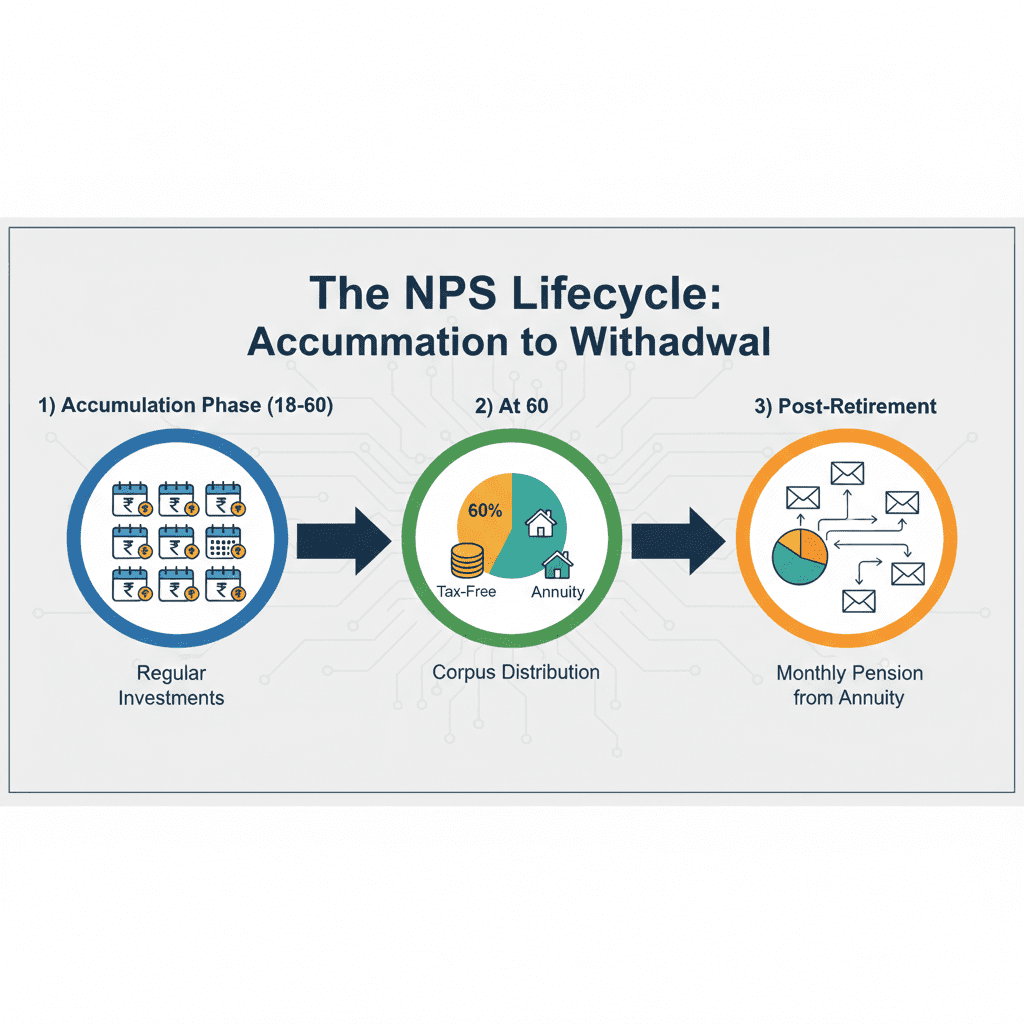

How NPS Works – The 3-Stage Lifecycle

Stage 1: Accumulation (Ages 18-60)

You invest regularly in your NPS account. Your money is managed by professional Pension Fund Managers (PFMs) who invest in a mix of equities (E), corporate bonds (C), government securities (G), and alternative investments (A). You choose your own asset allocation.

Stage 2: At Maturity (Age 60)

When you turn 60, you can withdraw:

-

Up to 60% of the corpus tax-free (lump sum)

-

At least 40% must be used to purchase an annuity (pension plan) from an IRDA-approved insurer

-

The annuity income is taxable as per your income slab

Stage 3: Post-Retirement Income

The annuity provides you with a regular monthly pension for life. You can choose different annuity options (lifetime, joint-life, return of purchase price, etc.).

Early Exit (Before 60)

You can exit before 60, but with conditions:

-

Minimum 5 years of account existence required

-

80% of corpus must be used for annuity

-

20% can be withdrawn tax-free (subject to conditions)

*Source: PFRDA Exit Rules *

Pro Tip: Use India Tax Tools’ NPS Calculator to project your retirement corpus based on your age, monthly contribution, and expected returns.

NPS TAX BENEFITS: THE TRIPLE ADVANTAGE DECODED

This is where NPS truly shines. No other investment offers tax benefits at all three stages—investment, growth, and withdrawal.

Benefit 1: Tax on Investment (Entry)

Under the Old Tax Regime, NPS investments are eligible for deductions under three sections:

| Section | Who Can Claim | Maximum Deduction | Notes |

|---|---|---|---|

| 80CCD(1) | All individuals (salaried/self-employed) | 20% of gross income (10% for govt employees) | Within overall 1.5 lakh 80C limit |

| 80CCD(1B) | All individuals | ₹50,000 (over and above 80C) | Exclusive NPS benefit |

| 80CCD(2) | Salaried employees only | Employer’s NPS contribution (up to 10%/14% of salary) | Over and above all limits |

Total Potential Deduction in Old Regime:

-

Your contribution: ₹1.5 lakh (under 80C) + ₹50,000 (under 80CCD(1B)) = ₹2 lakh

-

Employer contribution: Up to 10% of basic+DA (varies by employer type)

-

Total: ₹2 lakh + employer contribution—completely tax-free

Under New Tax Regime (2026) :

-

No deductions allowed under 80CCD(1), 80CCD(1B), or 80CCD(2)

-

Employer NPS contribution is taxable in your hands

-

However, the new regime offers lower tax rates—you must compare which benefits you more

Benefit 2: Tax on Growth (Accumulation)

This is the biggest wealth creator. The returns your NPS investments generate—whether from equities, bonds, or government securities—compound tax-free year after year. There’s no tax on dividends, interest, or capital gains within the NPS corpus during the accumulation phase.

Compare this to a fixed deposit where interest is taxed annually, reducing your compounding power.

Benefit 3: Tax on Withdrawal (Exit)

At maturity (age 60):

-

60% of corpus withdrawn as lump sum: Completely tax-free

-

40% of corpus used to purchase annuity: Not taxable at time of purchase

-

The annuity income (pension) you receive later: Taxable as per your income slab

This means the bulk of your retirement corpus (60%) grows and is withdrawn without ever paying tax.

Real Tax Saving Example

Scenario: Vikram, 34, earns ₹18 lakh annually (Old Tax Regime)

-

Contributes ₹50,000 to NPS under Section 80CCD(1B)

-

Also contributes ₹1.5 lakh to PPF/ELSS under 80C

-

Employer contributes ₹54,000 to NPS (10% of basic)

| Contribution | Section | Tax Saved (at 30% slab) |

|---|---|---|

| Own NPS (within 80C) | 80CCD(1) | Already counted in 1.5L |

| Own NPS (additional) | 80CCD(1B) | ₹15,000 |

| Employer NPS | 80CCD(2) | ₹16,200 |

| Total Tax Saved | ₹31,200 |

And this is just the tax saved every year. Over 26 years, this adds up to over ₹8 lakh in tax savings—plus the compounding benefit.

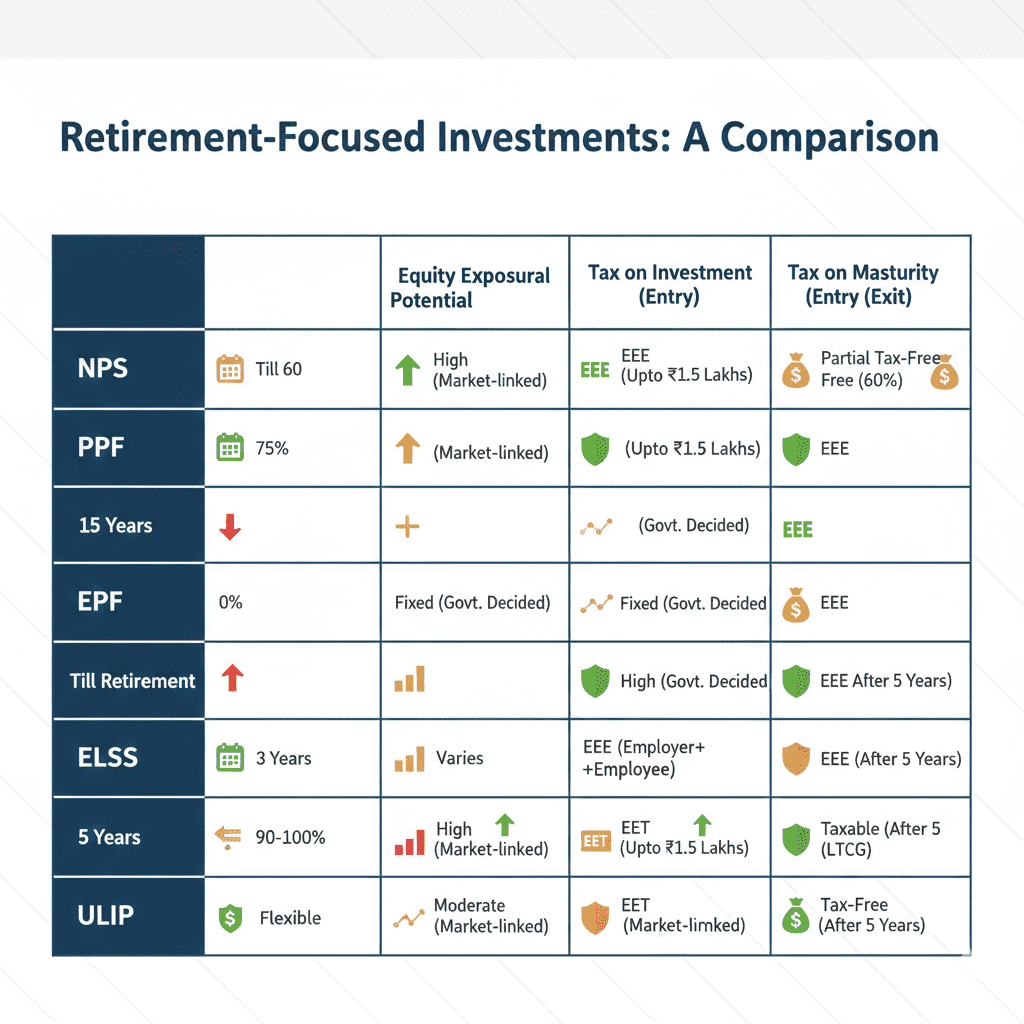

NPS VS OTHER RETIREMENT OPTIONS: COMPARISON

How does NPS stack up against traditional retirement tools?

| Feature | NPS | PPF | EPF | ELSS | ULIP |

|---|---|---|---|---|---|

| Lock-in | Till 60 (partial allowed) | 15 years | Till retirement | 3 years | 5 years |

| Equity Exposure | Up to 75% (till 50) | None | None | Up to 100% | Varies |

| Return Potential | High (market-linked) | Moderate (7.1% FY26) | Moderate (~8%) | High | Moderate |

| Tax on Investment | Triple benefit | 80C only | 80C only | 80C only | 80C only |

| Tax on Growth | Tax-free | Tax-free | Tax-free | Tax-free until sale | Tax-free |

| Tax on Maturity | 60% tax-free | Tax-free | Tax-free | LTCG >1L taxable | Varies |

| Expense Ratio | Low (~0.01-0.1%) | Zero | Zero | Moderate (0.5-1%) | High (2-3%) |

Key Takeaways

- NPS offers highest equity exposure among government-backed retirement schemes

- Lowest cost—expense ratios are among the lowest in the world

- Triple tax benefit—unmatched by any other product

- Partial liquidity through partial withdrawals (for specified purposes)

- The 60% tax-free withdrawal at maturity is unique

However, the mandatory annuity purchase (40%) and taxable annuity income are drawbacks compared to PPF/EPF.

HOW TO MAXIMIZE NPS RETURNS: SMART STRATEGIES

Returns aren’t automatic—they depend on your choices. Here’s how to optimize.

Strategy 1: Choose Your Pension Fund Manager Wisely

NPS offers multiple Pension Fund Managers (PFMs). Performance varies significantly.

| Fund Manager | 5-Year CAGR (Equity – E) | 5-Year CAGR (Corporate – C) |

|---|---|---|

| SBI Pension Funds | 15.2% | 9.1% |

| LIC Pension Fund | 14.8% | 8.9% |

| HDFC Pension | 16.1% | 9.4% |

| ICICI Prudential | 15.5% | 9.2% |

| UTI Retirement | 14.5% | 8.8% |

*Source: PFRDA performance data (illustrative, for conceptual understanding) *

Tip: Don’t just pick one. You can allocate across up to 3 fund managers. Review performance annually and switch if needed (limited free switches allowed).

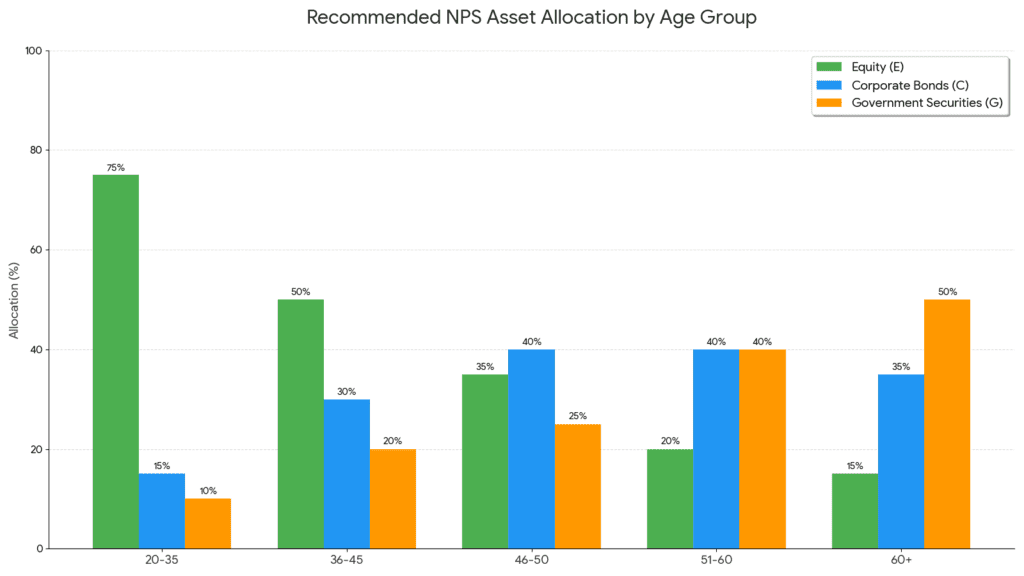

Strategy 2: Optimize Asset Allocation (E, C, G)

Your allocation to equities (E), corporate bonds (C), and government securities (G) determines long-term growth.

| Age | Recommended Equity (E) Allocation | Rationale |

|---|---|---|

| 20-35 | Active Choice: 65-75% | Maximum growth, time to recover volatility |

| 36-45 | Active Choice: 50-60% | Gradually reduce equity |

| 46-50 | Active Choice: 40-50% | Protect accumulated corpus |

| 51-60 | Auto-choice (gradual reduction) | Capital preservation |

| >60 | Annuity (40%) + debt | Income focus |

Auto Choice Option: If you prefer not to decide, NPS offers “Auto Choice” (Lifecycle Fund) where equity allocation decreases automatically with age.

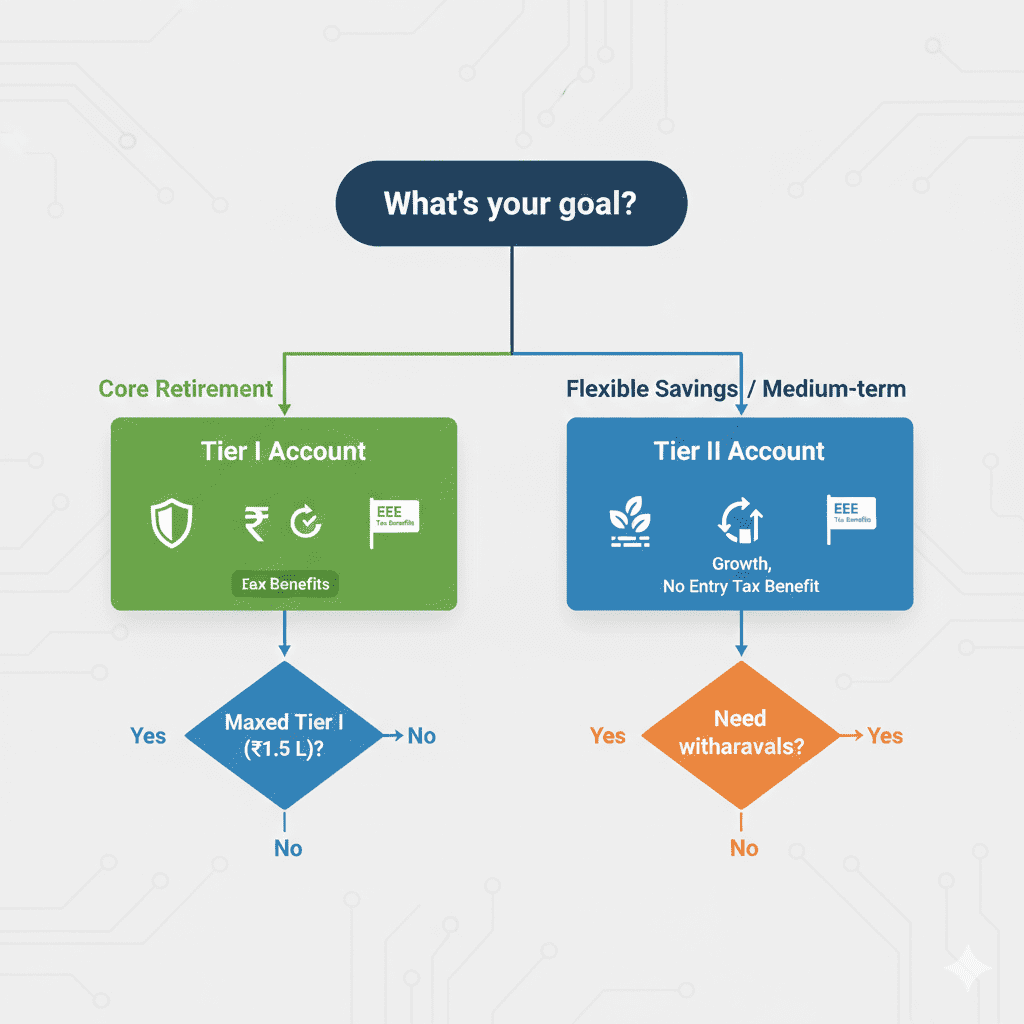

Strategy 3: Use Tier 1 + Tier 2 Strategically

| Account Type | Best For | Tax Benefit |

|---|---|---|

| Tier 1 (Primary) | Core retirement savings | Triple tax benefit (entry, growth, partial exit) |

| Tier 2 (Voluntary) | Additional savings, flexible withdrawals | Growth tax-free; no entry/exit benefit |

Strategy: Use Tier 1 for long-term retirement (maximize 80CCD benefits). Use Tier 2 for medium-term goals where you want NPS-like returns but with withdrawal flexibility.

Strategy 4: Make the Most of Employer Contributions

If your employer offers NPS contribution under Section 80CCD(2):

-

This is over and above your ₹1.5L 80C limit

-

Employer contribution up to 10%/14% of salary is tax-free in your hands

-

It also grows tax-free in your NPS account

Check if your employer has this facility. If not, request them to consider it—it’s a powerful employee retention tool.

Strategy 5: Don’t Ignore Annuity Selection

At maturity, 40% must go to annuity. Your choice here affects lifelong income:

| Annuity Option | Payout | Best For |

|---|---|---|

| Lifetime (single) | Highest monthly pension | Individual without dependents |

| Lifetime (joint) | Slightly lower, continues to spouse | Married couples |

| Return of Purchase Price | Lower pension, but corpus returned to nominee | Leaving inheritance |

| Increasing annuity | Starts low, increases with inflation | Long-term inflation protection |

Tip: Compare multiple insurers—you’re not locked to your PFM’s annuity provider. Shop around.

TIER 1 VS TIER 2 ACCOUNTS: WHICH ONE DO YOU NEED?

Tier 1 Account (Primary Retirement Account)

| Feature | Details |

|---|---|

| Purpose | Core retirement savings |

| Lock-in | Until age 60 (partial withdrawals allowed for specified purposes) |

| Minimum Contribution | ₹500 per year |

| Withdrawal Rules | Up to 25% of own contributions for specified purposes (education, marriage, house, illness) |

| Tax Benefits | Full triple benefit |

| Who Should Open | Anyone serious about retirement |

Tier 2 Account (Voluntary Savings)

| Feature | Details |

|---|---|

| Purpose | Flexible savings, medium-term goals |

| Lock-in | None (withdraw anytime) |

| Minimum Contribution | ₹1,000 (varies by POP) |

| Withdrawal Rules | Complete flexibility |

| Tax Benefits | Growth tax-free; no entry/exit tax benefit |

| Who Should Open | Those who want NPS-like returns with liquidity, already maximizing Tier 1 |

Key Decision Matrix

| Your Situation | Tier 1 | Tier 2 |

|---|---|---|

| Starting retirement savings | ✅ Open immediately | ⚠️ Optional |

| Already have Tier 1, want more NPS exposure | ⚠️ Increase Tier 1 contribution | ✅ Consider Tier 2 |

| Need flexibility to withdraw | ❌ Not suitable | ✅ Excellent |

| Want to save beyond ₹2 lakh tax deduction | ⚠️ No tax benefit beyond 2L | ✅ Still useful for growth |

| Short-term goal (<3 years) | ❌ Avoid | ⚠️ Equity risk remains |

COMMON NPS MISTAKES TO AVOID

| Mistake | Why It Hurts | Better Approach |

|---|---|---|

| Not opening NPS at all | Missing triple tax benefit and low-cost equity exposure | Open Tier 1 today—even ₹500 starts the clock |

| Choosing 100% debt (G or C) when young | Low long-term returns, inflation erodes corpus | At least 50% equity till age 40 |

| Ignoring fund manager choice | Default allocation may underperform | Review and select actively |

| Forgetting 80CCD(1B) ₹50,000 benefit | Leaving ₹15,000+ tax saving on table | Invest specifically for this |

| Not checking employer contribution | Missing free money + tax benefit | Ask HR about NPS facility |

| Withdrawing early without understanding | 80% annuity lock-in, tax implications | Explore partial withdrawal rules first |

| Choosing wrong annuity option | Lifetime income lower than possible | Compare multiple insurers |

| Stopping contributions | Compounding interrupted | Even small amounts matter; use SIP mode |

FREQUENTLY ASKED QUESTIONS

Q1: Is NPS tax-free at withdrawal?

Partially. At age 60:

-

60% of corpus withdrawn as lump sum: Tax-free

-

40% used for annuity: Not taxable at purchase

-

The annuity income (pension) you receive later: Taxable as per your slab

Q2: What is Section 80CCD(1B) in NPS?

Section 80CCD(1B) allows an additional deduction of up to ₹50,000 for NPS investments, over and above the ₹1.5 lakh limit under Section 80C . This is exclusive to NPS and a key reason to invest.

Q3: Can I have both Tier 1 and Tier 2 accounts?

Yes. In fact, you must have a Tier 1 account to open a Tier 2 account. Tier 2 is a voluntary savings account with no lock-in, but it doesn’t offer the same tax benefits as Tier 1 .

Q4: What happens to NPS if I die before retirement?

Your nominee receives the entire accumulated corpus. It is not subject to the 40% annuity rule. The lump sum paid to the nominee is tax-free under current rules.

Q5: Can I switch between pension fund managers?

Yes. You can switch your entire accumulated corpus from one PFM to another. You’re allowed one free switch per year. Additional switches may attract a nominal fee.

Q6: Is NPS better than PPF for retirement?

It depends on your age and risk appetite:

| Factor | NPS Better If… | PPF Better If… |

|---|---|---|

| Age | Young (20-45) – can take equity risk | Near retirement (50+) – need safety |

| Tax Benefit | Need extra ₹50,000 deduction | Only 80C limit needed |

| Returns | Want market-linked growth | Want guaranteed, safe returns |

| Liquidity | Can lock till 60 | Need 15-year lock (partial allowed) |

| Annuity | Don’t mind mandatory annuity | Want complete tax-free withdrawal |

Most experts recommend both – PPF for safety, NPS for growth.

Q7: How do I open an NPS account?

You can open online:

- Visit eNPS portal (https://enps.nsdl.com) or use your bank’s net banking

- Choose “Individual Subscriber”

- Fill details (PAN, Aadhaar, bank account)

- Complete e-sign/OTP verification

- Make initial contribution

- Receive PRAN (Permanent Retirement Account Number) instantly

You can also visit POPs (Points of Presence) like banks and post offices.

Q8: What is the minimum contribution in NPS?

-

Tier 1: ₹500 at account opening; minimum ₹1,000 per year thereafter

-

Tier 2: ₹1,000 at account opening; no minimum balance requirement

Q9: Can NRIs invest in NPS?

Yes. NRIs can open NPS accounts (Tier 1 only) if they are:

-

Indian citizens

-

Between 18-60 years

-

Having valid KYC documents (PAN, passport, etc.)

The account is subject to FEMA regulations, and annuity must be payable in India.

Q10: Is NPS taxable under new tax regime?

No. Under the New Tax Regime (default from 2023), deductions under Section 80CCD(1), 80CCD(1B), and 80CCD(2) are not available. Employer NPS contribution is also taxable in your hands . However, the growth within NPS remains tax-free, and the 60% lump sum withdrawal is still tax-free at exit.

ACTIONABLE CHECKLIST: MAXIMIZE YOUR NPS BENEFITS

Initial Setup

-

Open Tier 1 NPS account online (eNPS or bank)

-

Choose Pension Fund Manager(s) – review historical performance

-

Set asset allocation (E, C, G) based on age (use Active or Auto choice)

-

Set up monthly SIP/auto-debit for consistent contributions

-

Nominate beneficiaries

Annual Actions

-

Contribute at least ₹50,000 to claim full 80CCD(1B) benefit

-

Review fund performance against peers

-

Consider switching if a fund consistently underperforms (use free switch)

-

Check if employer offers NPS contribution (80CCD(2))

-

Update nominee if family circumstances change

At Key Life Stages

-

Age 40: Review equity allocation; consider reducing gradually

-

Job change: Check if new employer offers NPS; consolidate accounts if multiple

-

Marriage/child birth: Update nominee; consider increasing contribution

-

Age 50: Start planning annuity options; review asset allocation for capital preservation

At Maturity (Age 60)

-

Compare annuity options from multiple insurers (not just your PFM’s)

-

Choose withdrawal percentage (maximum 60% lump sum tax-free)

-

Select annuity type based on dependents and inflation needs

-

File ITR correctly – report annuity income annually

SUCCESS STORY: HOW RAJESH BUILT ₹2.3 CRORE RETIREMENT CORPUS

Profile: Rajesh, 45, software architect in Bengaluru

Started NPS: Age 30

Monthly Contribution: ₹5,000 (increased by 10% every 3 years)

Asset Allocation: Active choice – 65% E, 20% C, 15% G till 45; reduced to 50% E at 45

His Journey

| Age | Monthly Contribution | Corpus Accumulated |

|---|---|---|

| 30 | ₹5,000 | – |

| 35 | ₹6,000 | ₹4.2 lakh |

| 40 | ₹7,500 | ₹12.8 lakh |

| 45 (current) | ₹9,000 | ₹28.5 lakh |

Projected at 60 (assuming 12% returns):

-

Total corpus: ₹2.31 crore

-

Tax-free lump sum (60%): ₹1.39 crore

-

Annuity (40%): ₹92 lakh (providing monthly pension ~₹55,000)

Tax Savings Over 30 Years

| Period | Total NPS Investment | Tax Saved (30% slab) |

|---|---|---|

| Age 30-45 | ₹12.6 lakh | ₹3.78 lakh |

| Age 45-60 (projected) | ₹18.9 lakh | ₹5.67 lakh |

| Total | ₹31.5 lakh | ₹9.45 lakh |

Plus, the entire ₹2.31 crore corpus grew tax-free within NPS.

“The ₹50,000 extra deduction under 80CCD(1B) was my biggest motivation. That alone saved me over ₹15,000 in tax every year. Combined with equity growth, NPS has been my best retirement decision.” – Rajesh

CONCLUSION: YOUR RETIREMENT, YOUR NPS STRATEGY

Retirement planning isn’t about predicting the future—it’s about preparing for it. And NPS is one of the most powerful tools in your preparation toolkit.

The numbers speak for themselves:

-

Triple tax benefit unmatched by any other instrument

-

Lowest cost structure (0.01-0.1% expense ratio)

-

Equity growth potential with government backing

-

₹50,000 exclusive deduction under 80CCD(1B)

-

60% tax-free withdrawal at maturity

But like any tool, NPS delivers maximum results only when used strategically:

- Start early – even small amounts compound powerfully

- Choose equity aggressively when young

- Maximize the ₹50,000 80CCD(1B) benefit every year

- Leverage employer contributions if available

- Review periodically – fund managers, asset allocation

- Plan your annuity wisely at maturity

Your Next Steps

-

Open your NPS Tier 1 account today – it takes 15 minutes online

-

Use India Tax Tools’ NPS Calculator to project your retirement corpus

-

Set up monthly SIP – automate your contributions

-

Check with HR if your employer offers NPS under 80CCD(2)

-

Review asset allocation based on your age using the guidelines above

-

Share this guide with friends and family who haven’t started retirement planning

Remember: The best time to start retirement planning was 10 years ago. The second best time is today.

“NPS is the only investment in India that offers tax benefits at entry, growth, and exit. Use the ₹50,000 80CCD(1B) benefit—it’s free money from the government.”

Disclaimer: This article is for informational and educational purposes only and does not constitute investment or tax advice. NPS returns are market-linked and subject to volatility. Past performance does not guarantee future returns. Please consult your financial advisor before making investment decisions. The information provided is based on NPS rules, Budget 2026 announcements, and tax provisions available as of February 2026.