It’s 2026, and the “March Madness” of tax-saving is upon us again. You’re likely staring at your salary slip, wondering where to invest ₹1.5 lakh to save tax under Section 80C. But in the rush to beat the deadline, are you choosing the right instrument? Or are you simply parking money in the first option your friend suggests?

Here’s a hard truth: Not all tax-saving investments are created equal. While Section 80C offers a powerful deduction of up to ₹1.5 lakh, the “best” option for your friend might be a terrible fit for your financial goals .

Whether you are building a retirement corpus, saving for a child’s marriage, or simply looking for safe, guaranteed returns, your choice should align with your risk appetite and timeline.

In this Section 80C Complete Guide for 2026, we go beyond the basic list. We will rank over 15 investment options based on two critical parameters: Returns and Safety. We will also clarify the big debate—Old Tax Regime vs. New Tax Regime—so you can make an informed decision for FY 2025-26 (AY 2026-27). Plus, we’ll show you how tools like those on IndiaTaxTools.com can simplify your calculations.

Let’s dive in and build a tax-saving strategy that doesn’t just reduce your tax bill but also builds genuine long-term wealth.

Section 1: The Great Tax Shift – Old Regime vs. New Regime in 2026

Before we rank the investments, we must address the elephant in the room: Which tax regime should you choose?

As of FY 2025-26, India operates with two parallel tax systems. The New Tax Regime offers lower slab rates but disallows most deductions and exemptions, including Section 80C. The Old Tax Regime has higher slab rates but allows you to claim deductions like Section 80C, 80D, and HRA .

Here are the updated tax slabs for the New Tax Regime for FY 2025-26 (AY 2026-27):

| Income Slab (₹) | Tax Rate |

|---|---|

| 0 – 4,00,000 | Nil |

| 4,00,001 – 8,00,000 | 5% |

| 8,00,001 – 12,00,000 | 10% |

| 12,00,001 – 16,00,000 | 15% |

| 16,00,001 – 20,00,000 | 20% |

| 20,00,001 – 24,00,000 | 25% |

| Above 24,00,000 | 30% |

Source: Income Tax Department /

The Big Question: Should you opt for the new regime and ignore Section 80C?

Answer: It depends on your investible surplus. If you are already investing to meet long-term goals (like retirement or a child’s education), the old regime likely saves you more tax. However, if you don’t have significant investments or expenses (HRA, etc.), the new regime’s lower rates and higher standard deduction (₹75,000 for salaried) are simpler and may be more beneficial .

Our Advice: Don’t guess. Use an online tax calculator (like the one you can build or link from IndiaTaxTools.com) to compare your tax liability under both regimes. Once you decide to stick with the Old Regime, the following guide to Section 80C investments is your roadmap.

Section 2: The Golden Trio of Safety (EEE Status)

For risk-averse investors, the government-backed small savings schemes are the gold standard. The best among them offer the Exempt-Exempt-Exempt (EEE) status, meaning your investment, the interest earned, and the maturity amount are all tax-free . This is the pinnacle of tax efficiency.

1. Sukanya Samriddhi Yojana (SSY) – The High-Yield Champion

-

Interest Rate: 8.2% p.a. (compounded annually)

-

Lock-in Period: 21 years (or marriage of the girl child after 18)

-

Risk: Sovereign (Lowest)

-

Best For: Parents of a girl child below 10 years.

SSY is currently the undisputed king of debt-based, tax-free returns. With an interest rate of 8.2%, it outpaces most other small savings schemes and even bank FDs . The power of compounding over 21 years can create a substantial corpus for your daughter’s higher education or marriage. It’s not just a tax-saving tool; it’s a wealth-creation engine for a specific, meaningful goal .

2. Public Provident Fund (PPF) – The Anchor of Your Portfolio

-

Interest Rate: 7.1% p.a. (compounded annually)

-

Lock-in Period: 15 years

-

Risk: Sovereign (Lowest)

-

Best For: Retirement planning and building a long-term, risk-free corpus.

PPF remains the anchor of a conservative investor’s portfolio. It promotes disciplined saving with a 15-year lock-in, rewarding patience with attractive, risk-adjusted returns . While the rate is lower than SSY, its flexibility (extendable in blocks of 5 years) and partial withdrawal facility after 6 years make it incredibly versatile for long-term goals .

3. Employees’ Provident Fund (EPF) – The Mandatory Wealth Builder

-

Interest Rate: 8.25% p.a. (for FY 2024-25)

-

Lock-in Period: Until retirement

-

Risk: Sovereign (Lowest)

-

Best For: Salaried employees seeking a forced retirement corpus.

For salaried individuals, EPF is a no-brainer. It offers a high interest rate (usually above PPF) and the benefit of employer contributions. The power of regular contributions over a 30-year career, coupled with tax-free compounding, makes EPF the largest retirement corpus for most employees .

Section 3: The Market-Linked Performers (High Return Potential)

If you have a higher risk appetite and a long-term horizon (7+ years), equity should be part of your tax-saving strategy. These options offer the potential to beat inflation by a wide margin, though they come with volatility.

4. Equity Linked Savings Scheme (ELSS) – The Wealth Creator

-

Historical Returns: 14-18% (over long term, market-linked)

-

Lock-in Period: 3 years (shortest among all 80C options)

-

Risk: Moderate to High

-

Best For: Young investors seeking wealth creation and tax savings.

ELSS is the only 80C option that invests in equities. Historically, ELSS funds have delivered average five-year rolling returns of about 15.3%, often beating benchmark indices . The three-year lock-in is the shortest in the 80C category, offering relatively better liquidity. However, it is crucial to remember that returns are not guaranteed and are subject to market risks.

Investor Insight: Under the new tax regime, ELSS loses its tax-saving sheen but remains a solid equity investment with a mandatory 3-year lock-in, which can actually help inculcate investment discipline .

5. National Pension System (NPS) – The Retirement Specialist

-

Historical Returns: 9-12% (mix of equity and debt, market-linked)

-

Lock-in Period: Until retirement (60 years)

-

Risk: Moderate

-

Best For: Individuals focused solely on retirement who want an additional deduction over 80C.

NPS is not just a Section 80C investment. While contributions up to ₹1.5 lakh qualify under 80C, you can claim an additional deduction of up to ₹50,000 under Section 80CCD(1B) . This makes it one of the most powerful tax-saving tools for higher-income earners. It invests in a mix of equity and debt, offering market-linked returns with low fund management charges.

Section 4: The Fixed-Income Regulars (Moderate Safety, Taxable Returns)

This category includes traditional options that are safe but offer partially taxable returns. They are suitable for conservative investors who have already maxed out their EEE quota.

6. National Savings Certificate (NSC)

-

Interest Rate: 7.7% p.a. (compounded annually)

-

Lock-in Period: 5 years

-

Risk: Sovereign (Lowest)

-

Taxation: Interest for the first 4 years is deemed reinvested and qualifies for Section 80C. Interest in the 5th year is fully taxable .

NSC has a “reinvestment advantage.” While you don’t receive the interest annually, it gets reinvested and also qualifies for a tax deduction (except in the final year), boosting your effective return.

7. Tax-Saving Fixed Deposits (FDs)

-

Interest Rate: 6.5% – 7.5% (varies by bank)

-

Lock-in Period: 5 years

-

Risk: Low (but not sovereign guaranteed beyond ₹5 lakh)

-

Taxation: Interest is fully taxable as per your income slab.

Tax-saving FDs are simple and safe but offer post-tax returns that are often lower than PPF for those in higher tax brackets.

8. Senior Citizens’ Savings Scheme (SCSS)

-

Interest Rate: 8.2% p.a. (paid quarterly)

-

Lock-in Period: 5 years (extendable)

-

Risk: Sovereign (Lowest)

-

Best For: Senior citizens.

-

Taxation: Interest is fully taxable, but senior citizens can claim a deduction up to ₹50,000 under Section 80TTB .

SCSS offers one of the best interest rates for retirees, and the 80TTB deduction makes it more tax-efficient for seniors.

9. 5-Year Post Office Time Deposit (TD)

-

Interest Rate: 7.5% p.a.

-

Lock-in Period: 5 years

-

Risk: Sovereign (Lowest)

-

Taxation: Interest is fully taxable annually .

Only the 5-year variant qualifies for Section 80C. It’s a straightforward, safe option, but the annual taxation of interest reduces its net return for taxable individuals.

Section 5: The Hybrid & Insurance Options (Proceed with Caution)

These options often blend insurance with investment. While they offer tax benefits, they are notorious for high costs and lower returns compared to “invest and insure separately” strategies.

10. Unit Linked Insurance Plans (ULIPs)

-

Returns: Market-linked

-

Lock-in Period: 5 years

-

Risk: Moderate to High

-

Taxation: EEE (subject to premium conditions)

-

Best For: Those who want a single product for insurance and investment (though often not recommended).

ULIPs have become more transparent after regulatory changes, with lower charges. However, they still lock you in for 5 years. Compare them thoroughly with a combination of a term plan + ELSS/PPF before investing.

11. Life Insurance Premiums (Traditional Policies)

-

Returns: 4-6% p.a. (very low)

-

Lock-in Period: Policy term (often 10-15 years)

-

Risk: Low

-

Taxation: EEE (subject to conditions)

-

Best For: Almost no one from a pure investment perspective.

Endowment and money-back policies are among the worst-performing investment options. They offer a meager 4-6% return, which is often lower than a bank FD and does not beat inflation . If you need life cover, buy a pure term insurance plan. For investments, stick to the options above.

Section 6: The Comprehensive Ranking (Returns vs. Safety)

To help you decide, here’s how the major Section 80C options stack up against each other.

Table 1: Returns vs. Safety Matrix

| Investment Option | Expected Returns (p.a.) | Safety Level | Lock-in Period | Tax on Maturity | Best Suited For |

|---|---|---|---|---|---|

| Sukanya Samriddhi Yojana | 8.2% (Fixed) | Highest | 21 years | Tax-Free | Girl Child’s Future |

| ELSS | 14-18% (Market-linked) | Moderate | 3 years | Taxable (LTCG) | Wealth Creation |

| EPF | 8.25% (Fixed) | Highest | Retirement | Tax-Free | Retirement (Salaried) |

| NPS (Tier I) | 10-12% (Market-linked) | Moderate-High | Retirement | 60% Tax-Free | Retirement (All) |

| PPF | 7.1% (Fixed) | Highest | 15 years | Tax-Free | Retirement / Long-term |

| NSC | 7.7% (Fixed) | Highest | 5 years | Partially Taxable | Medium-term goals |

| SCSS | 8.2% (Fixed) | Highest | 5 years | Taxable | Senior Citizens |

| Tax-Saving FD | 6.5-7.5% (Fixed) | High | 5 years | Taxable | Ultra-Conservative |

| Life Insurance | 4-6% (Poor) | High | Policy Term | Tax-Free | Avoid for investment |

Section 7: How to Build Your ₹1.5 Lakh Portfolio

Now that you know the options, how do you choose? A well-diversified portfolio is key. Don’t put all your eggs in one basket.

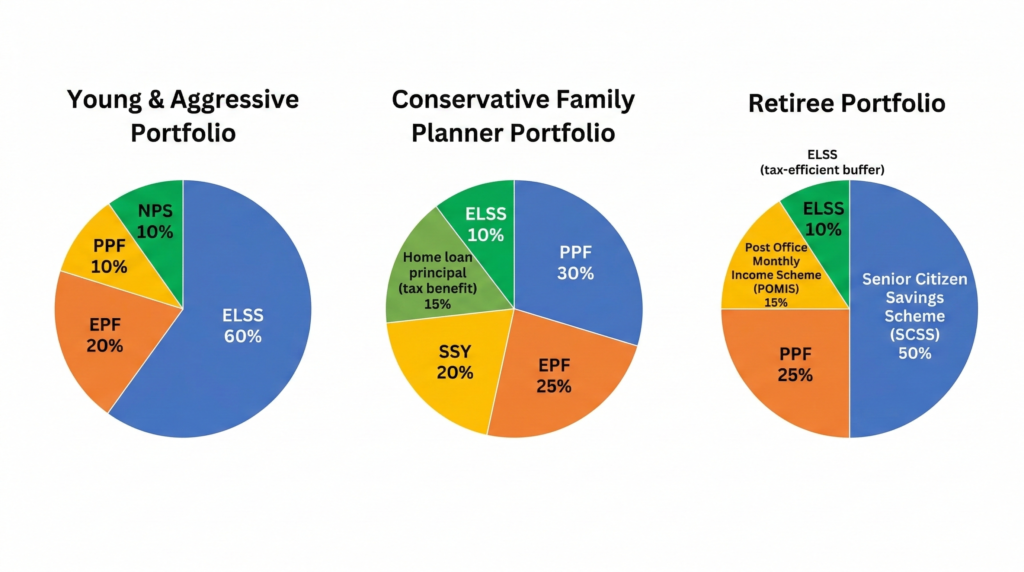

Scenario A: The Young & Aggressive Investor (Age: 28)

-

Goal: Maximize wealth creation.

-

Portfolio: ₹90,000 in ELSS (SIP), ₹50,000 in NPS (for extra 80CCD benefit), ₹10,000 in PPF (for long-term safety).

-

Rationale: High equity allocation for growth, with a small safe debt cushion.

Scenario B: The Conservative Family Planner (Age: 38)

-

Goal: Safety for children’s education and retirement.

-

Portfolio: ₹1,00,000 in PPF (for retirement), ₹50,000 in SSY (for daughter’s future).

-

Rationale: Maximizing government-backed, tax-free EEE instruments with clear goals.

Scenario C: The Retiree (Age: 62)

-

Goal: Regular income and capital preservation.

-

Portfolio: ₹1,50,000 in SCSS.

-

Rationale: Highest safe returns with quarterly payouts, and additional tax benefit under Section 80TTB.

Actionable Checklist:

-

Decide on Tax Regime: Use an Income Tax Calculator (like on IndiaTaxTools.com) to compare old vs. new regime liability.

-

Assess Risk: Are you comfortable with market volatility? If not, stick to PPF/SSY.

-

Calculate Required Investment: You need to invest ₹12,500 per month to hit the ₹1.5 lakh limit. Can you do it?

-

Set Up SIPs: For ELSS, start a monthly SIP to average out market volatility.

-

Track Your Investments: Use a portfolio tracker to monitor your 80C investments.

Conclusion

Section 80C is more than just a tax deduction; it’s a structured savings framework that can help you build significant wealth over time. For FY 2025-26, the choice is clear: If you’re in the old regime, don’t just invest to save tax—invest to achieve your life goals.

-

For guaranteed, tax-free growth, SSY and PPF are unmatched.

-

For beating inflation, ELSS is your best bet.

-

For an extra retirement push, don’t forget the additional ₹50,000 in NPS.

Start early, plan wisely, and let your investments work for you. Avoid the last-minute rush in March 2026. Use tools to simplify your planning, calculate your returns, and stay on track.

Ready to optimize your taxes? Use our Section 80C Calculator at IndiaTaxTools.com to see exactly how much you can save and which investments fit your profile.

Frequently Asked Questions (FAQ)

1. Can I claim Section 80C deduction if I opt for the New Tax Regime?

No. Section 80C deductions are not allowed under the New Tax Regime. They are exclusively available to taxpayers who opt for the Old Tax Regime .

2. Which Section 80C investment has the highest return?

Historically, ELSS has the potential to generate the highest returns (12-18%) as it is linked to the equity market. Among fixed-income options, Sukanya Samriddhi Yojana (SSY) offers the highest guaranteed return at 8.2% .

3. What is the difference between EEE and EET status?

-

EEE (Exempt-Exempt-Exempt): Investment, interest, and maturity are tax-free (e.g., PPF, EPF, SSY).

-

EET (Exempt-Exempt-Taxed): Investment is tax-free at entry, but the maturity proceeds (or interest) are taxed (e.g., NSC, Tax-saving FDs) .

4. Is there any benefit of investing in NPS over and above the ₹1.5 lakh Section 80C limit?

Absolutely. Under Section 80CCD(1B), you can claim an additional deduction of up to ₹50,000 for investments in NPS (Tier I account), over and above the ₹1.5 lakh limit of Section 80C .

5. Can I claim home loan principal repayment under Section 80C?

Yes, the principal portion of your home loan EMI is eligible for a deduction under Section 80C, up to the overall limit of ₹1.5 lakh .

6. Which is better for a child’s future: SSY or PPF?

For a girl child, SSY is far superior due to its higher interest rate (8.2% vs 7.1%). For a boy child, PPF is the best government-backed option .

Resources & Further Reading

-

Income Tax India Official Portal: For official notifications and forms.

-

Internal Link: Check out our guide on “How to Calculate Capital Gains from ELSS” on IndiaTaxTools.com.

-

Internal Link: Use our NPS Returns Calculator to project your retirement corpus.

Disclaimer: This article is for informational purposes only and does not constitute financial or tax advice. Tax laws are subject to change. Please consult a qualified Chartered Accountant or financial advisor before making any investment decisions.

(Disclaimer: This article contains tools from IndiaTaxTools.com for your convenience.)