Meet Priya, a 32-year-old marketing professional in Bangalore. She just received a ₹5 lakh bonus and is staring at her bank account with a mix of excitement and anxiety. “Should I put this entire amount into mutual funds at once? Or start a monthly SIP? What if the market crashes right after I invest?” Meanwhile, her colleague Ramesh, 45, has been investing ₹10,000 monthly for years but wonders if he’d have been better off with lump sum investments during market dips.

If you’ve ever faced this dilemma, you’re not alone. SIP vs lump sum is arguably the most debated question in Indian personal finance circles. With over ₹28,265 crore flowing into SIPs monthly as of August 2025 , and millions of Indians receiving bonuses, inheritances, or maturities each year, the choice matters—and it can significantly impact your long-term wealth.

Here’s the truth: There’s no universal winner. The right choice depends on market conditions, your risk tolerance, investment horizon, and even your psychological makeup. A ₹10,000 monthly SIP and a ₹1.2 lakh lump sum investment can deliver very different outcomes over the same period .

In this comprehensive 2026 guide, you’ll discover:

-

Mathematical comparison: SIP vs lump sum returns over 1, 3, 5, and 20 years

-

Market scenario analysis: Which works better in rising, falling, and volatile markets

-

Risk psychology: Why your personality matters more than you think

-

The hybrid solution: STP (Systematic Transfer Plan) explained

-

Tax implications: How holding periods differ between the two methods

-

Decision framework: A simple flowchart to choose your strategy

By the end, you’ll know exactly which approach—or combination—fits your financial situation in 2026.

SIP AND LUMP SUM: UNDERSTANDING THE BASICS

Before comparing returns, let’s clarify what each method actually does.

What is Systematic Investment Plan (SIP)?

A Systematic Investment Plan (SIP) allows you to invest a fixed amount in mutual funds at regular intervals—typically monthly, though weekly or quarterly options exist .

How SIP Works:

-

You commit to investing ₹X every month

-

On the designated date, the amount is auto-debited from your bank

-

You receive units at the prevailing Net Asset Value (NAV) that day

-

Over time, you accumulate units at different prices

Key Advantage: SIPs implement rupee cost averaging. When the market is low, your fixed amount buys more units. When it’s high, you buy fewer units. This automatically averages your purchase cost without requiring you to time the market .

Best For: Salaried individuals with regular monthly income, first-time investors, and those who want to build investment discipline .

What is Lump Sum Investment?

A lump sum investment involves deploying a significant amount of money into a mutual fund or investment vehicle all at once .

How Lump Sum Works:

-

You have a corpus ready (bonus, inheritance, maturity proceeds)

-

You invest the entire amount on a single day

-

Your entire capital starts working immediately

-

Returns compound on the full amount from day one

Key Advantage: Immediate market participation and full compounding on the entire principal. In rising markets, this can significantly outperform staggered investments .

Best For: Investors with large surplus funds, those receiving windfalls, experienced investors comfortable with market timing, and long-term horizons .

Quick Comparison: SIP vs Lump Sum

| Feature | SIP | Lump Sum |

|---|---|---|

| Investment Pattern | Fixed amount at regular intervals | Entire amount at once |

| Market Timing Risk | Low (averaged over time) | High (depends on entry point) |

| Compounding Base | Builds gradually | Full amount from day one |

| Discipline Required | Automatic (set and forget) | Self-discipline needed |

| Best Market Condition | Volatile or expensive markets | After corrections, rising markets |

| Minimum Amount | As low as ₹500 | Typically ₹5,000–₹10,000 |

Source: DSP Mutual Fund , Motilal Oswal

SIP VS LUMP SUM: MATHEMATICAL COMPARISON (WITH REAL NUMBERS)

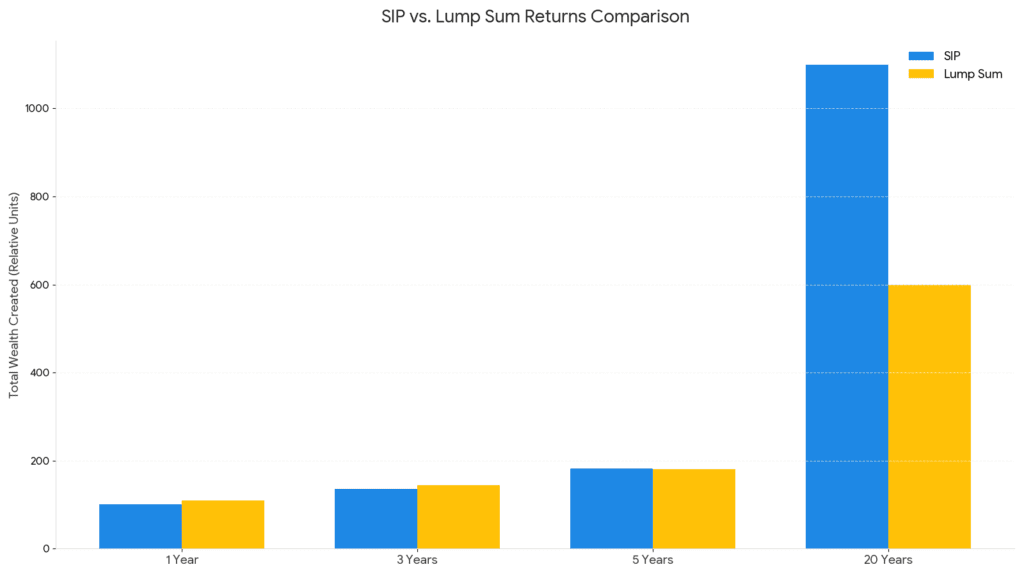

Let’s move from theory to actual numbers. Using conservative 12% returns (unless otherwise specified), here’s how SIP and lump sum compare across different time horizons.

Scenario 1: 1-Year Investment Horizon

SIP: ₹10,000 per month

-

Total invested: ₹1,20,000

-

Expected returns at 12%: ₹8,093

-

Total value after 1 year: ₹1,28,093

Lump Sum: ₹1,20,000 one-time

-

Total invested: ₹1,20,000

-

Expected returns at 12%: ₹14,400

-

Total value after 1 year: ₹1,34,400

Verdict: Lump sum outperforms by ₹6,307

Why? The entire lump sum amount remained invested for the full year, allowing compounding to work on a higher base from day one .

Scenario 2: 3-Year Investment Horizon

SIP: ₹10,000 per month

-

Total invested: ₹3,60,000

-

Expected returns at 12%: ₹75,076

-

Total value after 3 years: ₹4,35,076

Lump Sum: ₹1,20,000 one-time (same total investment)

-

Total invested: ₹3,60,000

-

Expected returns at 12%: ₹93,519

-

Total value after 3 years: ₹4,53,519

Verdict: Lump sum still leads, but the gap narrows slightly

Scenario 3: 20-Year Long-Term Horizon

Case A: ₹1,000 Monthly SIP

-

Total invested: ₹2,40,000 (over 20 years)

-

Expected returns at 15%: ₹10,87,073

-

Total value after 20 years: ₹13,27,073

Case B: ₹1 Lakh Lump Sum (one-time)

-

Total invested: ₹1,00,000

-

Expected returns at 15%: ₹15,36,654

-

Total value after 20 years: ₹16,36,654

Case C: ₹2,000 Monthly SIP

-

Total invested: ₹4,80,000

-

Expected returns at 12%: ₹15,18,295

-

Total value after 20 years: ₹19,98,295

Case D: ₹1 Lakh Lump Sum at 12%

-

Total invested: ₹1,00,000

-

Expected returns at 12%: ₹8,64,629

-

Total value after 20 years: ₹9,64,629

Key Insights from Long-Term Data

- Lump sum advantage in rising markets: When markets trend upward, lump sum generally outperforms because the entire capital participates from the start.

- SIP advantage in volatile/flat markets: SIPs shine when markets are range-bound or volatile, as they average out purchase costs.

- Discipline beats timing: A ₹2,000 monthly SIP growing to nearly ₹20 lakh over 20 years demonstrates the power of consistent investing.

- The base effect: Even though the ₹1 lakh lump sum at 12% generated only ₹9.64 lakh versus ₹19.98 lakh from SIP, remember the SIP invested 4.8x more money over the period.

- Critical Takeaway: The method matters less than staying invested. A study of the Nifty 50 TRI over 24 years (2001-2025) showed that missing just the 50 best trading days would have reduced your returns from 15.61% CAGR to less than 1% .

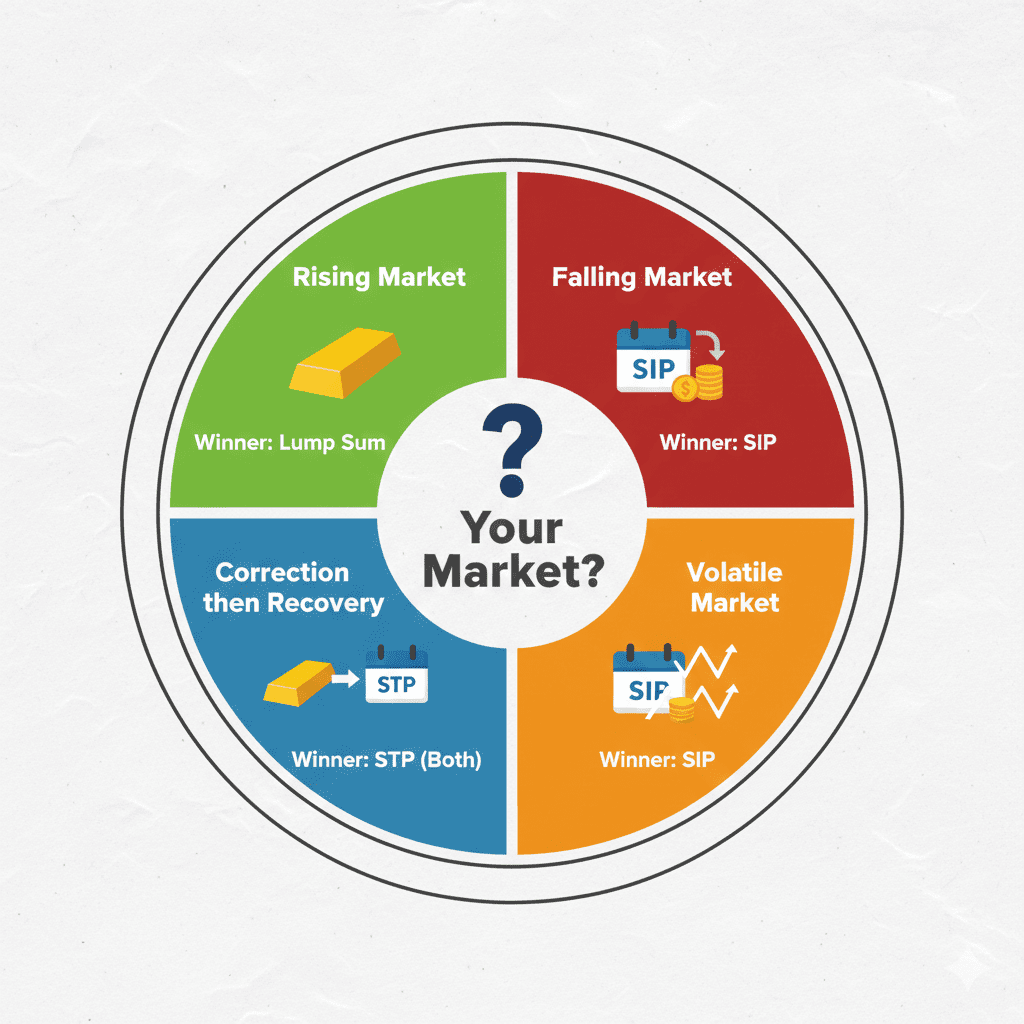

MARKET SCENARIO ANALYSIS: WHEN EACH METHOD WINS

The “better” method depends entirely on what the market does after you invest.

Scenario A: Rising Market (Bull Phase)

Example: You invest in January, and markets rally 20% over the year.

| Method | Outcome |

|---|---|

| Lump Sum | Entire corpus benefits from 20% growth |

| SIP | Only first month’s investment gets full 20%; later installments get progressively less time |

Winner: Lump Sum

Scenario B: Falling Market (Bear Phase)

Example: Markets decline 15% in first six months, then recover.

| Method | Outcome |

|---|---|

| Lump Sum | Full corpus takes immediate 15% hit; recovery takes time |

| SIP | Early months buy at lower prices; recovery benefits all units |

Winner: SIP

Scenario C: Volatile / Range-Bound Market

Example: Markets fluctuate between -5% and +5% throughout the year.

| Method | Outcome |

|---|---|

| Lump Sum | Performance depends entirely on entry point |

| SIP | Rupee cost averaging buys more units at lows, fewer at highs |

Winner: SIP

Scenario D: Market Correction Followed by Recovery

Example: Market drops 20% in first quarter, then recovers 30% over next nine months.

| Method | Outcome |

|---|---|

| Lump Sum (invested before crash) | Severe initial loss; may take years to recover |

| Lump Sum (invested at bottom) | Maximum gains from recovery |

| SIP (ongoing) | Buys throughout the crash at low prices; benefits fully from recovery |

Winner: SIP (for avoiding timing risk) or perfectly timed lump sum (for maximum gains—but timing perfection is rare)

Real-World Data: Nifty Benchmark Study

A study comparing SIP vs lump sum returns across Nifty indices (as of July 2024) revealed :

| Benchmark | 1-Yr SIP Return | 1-Yr Lump Sum | 3-Yr SIP CAGR | 3-Yr Lump Sum | 5-Yr SIP CAGR | 5-Yr Lump Sum |

|---|---|---|---|---|---|---|

| NIFTY 50 TRI | 34.12% | 27.87% | 20.91% | 17.37% | 20.89% | 17.60% |

| NIFTY 100 TRI | 41.46% | 33.95% | 23.14% | 18.33% | 22.12% | 18.34% |

| NIFTY 500 TRI | 46.44% | 40.05% | 26.80% | 20.68% | 25.32% | 20.82% |

Observation: SIPs consistently outperformed lump sum across all time horizons in this specific historical period—demonstrating that in real-world volatile markets, cost averaging provides a tangible edge .

THE PSYCHOLOGY FACTOR: RISK TOLERANCE AND EMOTIONAL COMFORT

Numbers don’t tell the whole story. Your psychological makeup is equally important.

The Lump Sum Emotional Challenge

Imagine this: You’ve just invested your entire ₹10 lakh bonus in an equity fund. Two weeks later, a global news event triggers a 10% market correction. Your portfolio now shows ₹9 lakh.

How do you feel?

-

Can you sleep at night?

-

Will you panic and sell at the bottom?

-

Or will you view it as a buying opportunity (if you have more cash)?

If the thought makes you anxious, lump sum may not be for you—even if historically it might have generated higher returns .

The SIP Emotional Advantage

Now imagine the same market correction, but you’re investing ₹25,000 monthly through SIP:

How do you feel?

-

“Great! This month’s SIP will buy units at a discount.”

-

No panic because only a small portion of your total future corpus is affected.

-

You’re actually grateful for the opportunity to average down.

This psychological comfort is SIP’s hidden superpower .

Investor Personality Types

| Investor Type | Better Suited For | Why |

|---|---|---|

| First-time investor | SIP | Gradual market exposure builds confidence |

| Experienced, high-risk tolerance | Lump Sum (in right conditions) | Can handle volatility, may time entries |

| Anxious / loss-averse | SIP | Emotional stability matters more than marginal returns |

| Busy professional | SIP | Automation ensures discipline without mental load |

| Retiree with corpus | Hybrid (STP) | Balance growth with capital protection |

The Bottom Line on Psychology

As Sanjiv Bajaj of BajajCapital puts it: “Markets reward discipline far more consistently than they reward timing. SIPs work because they take the emotion out of investing and let time do the heavy lifting” .

If you’re the type who checks portfolio values daily and reacts to news, SIP will save you from yourself. If you’re stoic and can ignore short-term fluctuations, lump sum may serve you well.

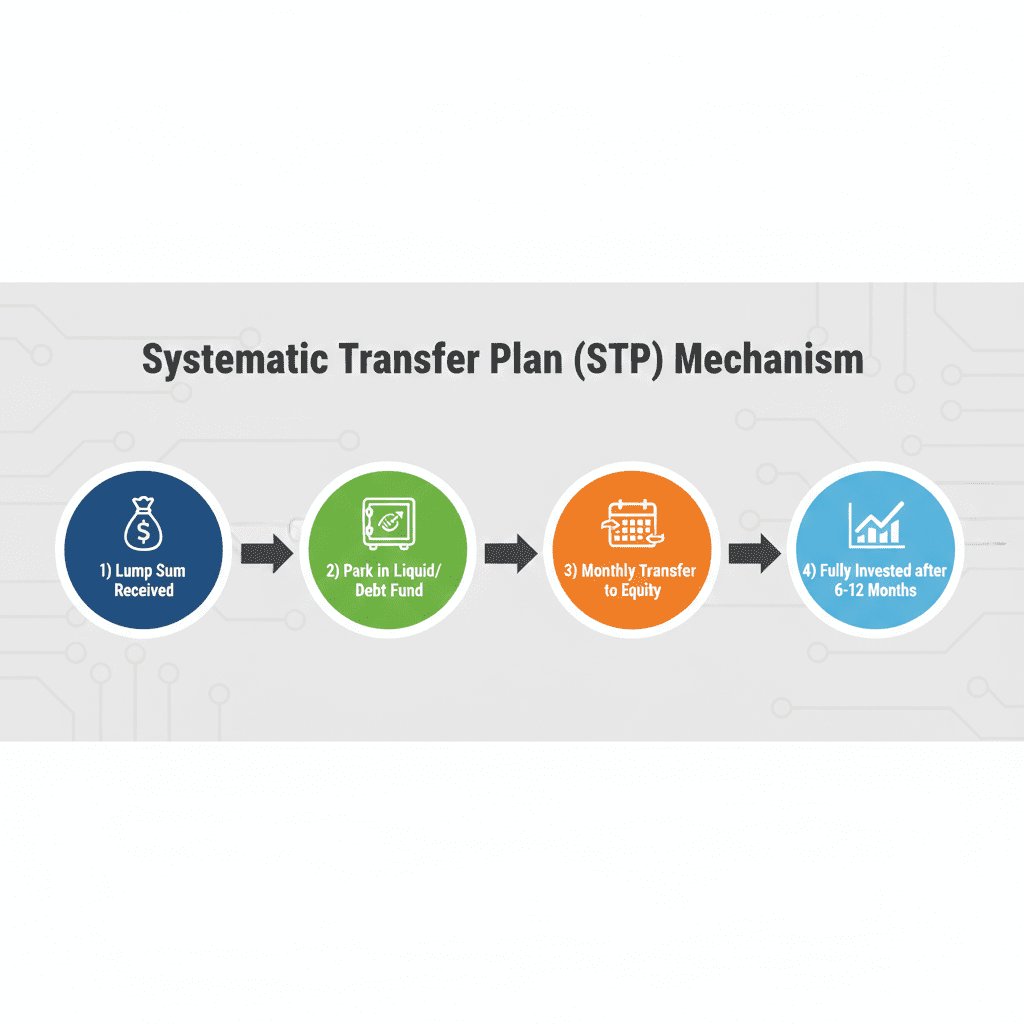

THE HYBRID SOLUTION: SYSTEMATIC TRANSFER PLAN (STP)

What if you want the best of both worlds—immediate deployment for some returns, plus averaging to reduce timing risk? Enter the Systematic Transfer Plan (STP) .

How STP Works

- You invest your entire lump sum in a debt fund (liquid fund, overnight fund, or ultra-short duration fund).

- You set up an STP instruction to transfer a fixed amount monthly from this debt fund into your target equity fund.

- The debt fund earns modest returns (6-7% typically) while your money waits.

- Over 6-12 months, your entire corpus gradually moves into equities.

STP Example

| Step | Action | Amount |

|---|---|---|

| 1 | You receive ₹10 lakh bonus | ₹10,00,000 |

| 2 | Invest in Liquid Fund (immediate) | ₹10,00,000 |

| 3 | Set up STP of ₹83,333/month for 12 months into an Equity Fund | ₹83,333 × 12 |

| 4 | After 12 months | Fully invested in Equity |

Why STP Makes Sense in 2026

| Advantage | Explanation |

|---|---|

| Reduces timing risk | If markets crash next month, only the first STP tranche is affected |

| No idle cash | Your money earns debt fund returns while waiting |

| Averaging benefit | You get rupee cost averaging without delaying market participation entirely |

| Emotional comfort | Gradual exposure prevents panic during corrections |

When to Use STP

| Scenario | STP Recommended? |

|---|---|

| Markets at all-time highs | ✅ Yes |

| You’re nervous about investing a large sum | ✅ Yes |

| You have a 3-5 year horizon | ✅ Yes |

| Markets just crashed 15% | ❌ Probably not—consider lump sum |

| You’re a seasoned investor | ❌ May prefer direct lump sum |

Source: Motilal Oswal , DSP Mutual Fund

TAX IMPLICATIONS: A OFTEN-OVERLOOKED DIFFERENCE

Most comparisons ignore tax, but the holding period calculation differs significantly between SIP and lump sum .

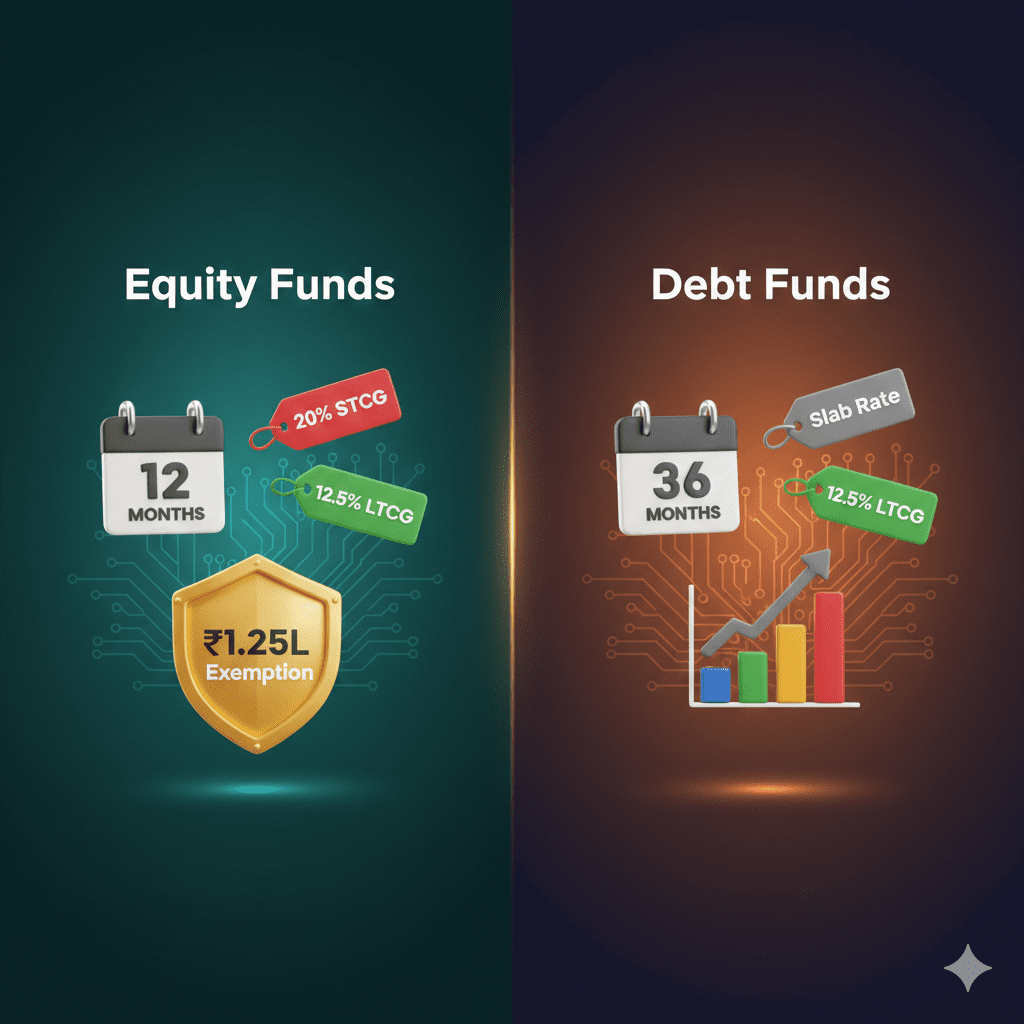

Equity Funds Tax Rules (2026)

| Holding Period | Tax Type | Rate |

|---|---|---|

| Less than 1 year | Short-term capital gains (STCG) | 20% |

| More than 1 year | Long-term capital gains (LTCG) | 12.5% (over ₹1.25 lakh) |

Source: Budget 2026 updates

How SIP Affects Holding Period

With SIP, you have multiple purchase dates. When you redeem:

-

FIFO (First-In, First-Out) method applies

-

The oldest units (first SIP installments) are sold first

-

Some units may be long-term, others short-term, depending on when each SIP was made

Example: You started a ₹10,000 monthly SIP in January 2025. In January 2026, you need to redeem ₹50,000.

-

Units from Jan-Feb 2025 (12+ months old) → LTCG

-

Units from Mar-Dec 2025 (<12 months) → STCG

You’ll pay two different tax rates on the same redemption.

How Lump Sum Affects Holding Period

With lump sum, you have a single purchase date:

-

Hold for >1 year → all gains LTCG

-

Redeem within 1 year → all gains STCG

Much simpler to track and calculate .

Tax Efficiency Tip

For long-term goals (>5 years), the tax complexity of SIP is manageable. But if you’re investing a large amount that you might need partially within 1-3 years, lump sum’s simpler tax treatment could be advantageous.

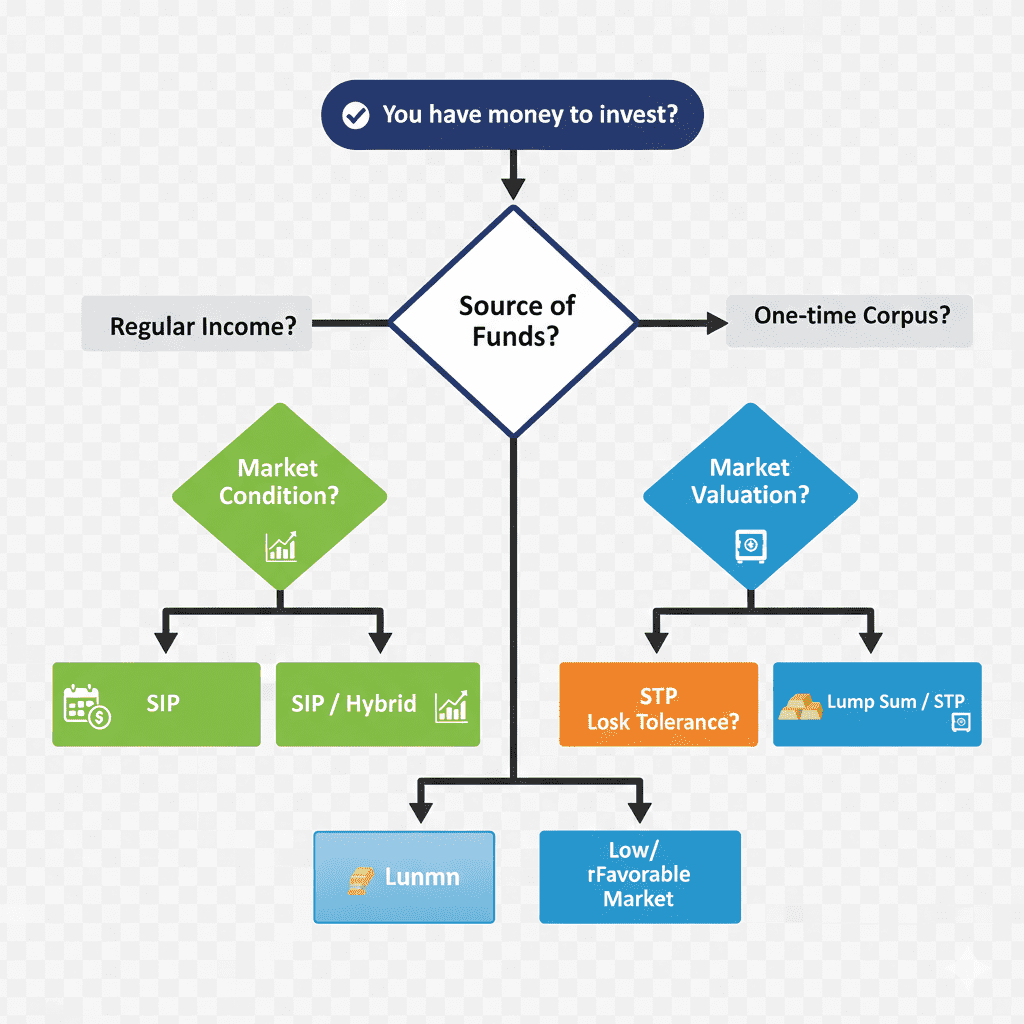

DECISION FRAMEWORK: HOW TO CHOOSE IN 2026

Use this step-by-step framework to decide.

Step 1: Analyze Your Cash Flow

| You have… | Primary method |

|---|---|

| Regular monthly surplus (salary, business income) | SIP |

| One-time windfall (bonus, inheritance, property sale) | Lump Sum or STP |

Step 2: Assess Market Valuations

| Market Condition | Recommended Approach |

|---|---|

| Markets at all-time highs, valuations stretched | SIP or STP (staggered entry) |

| Markets just corrected 10-15% | Consider lump sum |

| Mid-cap/small-cap valuations high | SIP in these segments |

| Large-cap valuations reasonable | Can consider lump sum |

Step 3: Evaluate Your Risk Tolerance

Honestly answer: “If I invest my entire amount today and markets fall 15% tomorrow, will I panic and sell?”

-

Yes, I’ll panic → Choose SIP or STP

-

No, I’ll stay invested or buy more → Lump sum may be acceptable

Step 4: Consider Your Investment Horizon

| Horizon | SIP | Lump Sum |

|---|---|---|

| Less than 3 years | ⚠️ Risky (equity not recommended for short term) | ⚠️ Even riskier |

| 3-5 years | ✅ Good (averaging helps) | ⚠️ Timing risk high |

| 5-7 years | ✅ Very good | ✅ Good (if entry reasonable) |

| 7+ years | ✅ Excellent | ✅ Excellent (compounding shines) |

Step 5: The Final Decision Matrix

| Your Profile | Recommended Strategy |

|---|---|

| Salaried professional, first-time investor, markets near highs | Start SIP; continue for 5+ years |

| Received ₹5 lakh bonus, markets stable | 50% lump sum now, 50% STP over 6 months |

| Experienced investor, markets just crashed | Lump sum (if you have courage and cash) |

| Retiree with ₹50 lakh corpus | Conservative hybrid: STP into balanced advantage funds |

| Any investor, any situation | At least start a SIP—something beats nothing |

EXPERT STRATEGIES FOR 2026

Strategy 1: The Core-Satellite Approach

Use SIP for your core portfolio (60-70% of allocation) to build discipline and average costs over time. Use lump sum for satellite investments (30-40%) when opportunities arise—like market corrections or sector-specific dips .

Strategy 2: Valuation-Based Allocation

| Market Valuation | Equity Allocation Method |

|---|---|

| Nifty PE > 25 (expensive) | 100% SIP (or STP over 12+ months) |

| Nifty PE 20-25 (fair) | 50% lump sum, 50% SIP/STP |

| Nifty PE < 18 (attractive) | Consider lump sum with 3-year horizon |

Strategy 3: The 12-Month STP Rule

For any lump sum above ₹5 lakh in uncertain markets, default to a 12-month STP:

-

Invest in liquid fund immediately

-

Transfer equal amount monthly to equity

-

Adjust duration based on volatility (longer if markets frothy)

Strategy 4: Goal-Based Allocation

| Goal | Horizon | Recommended Method |

|---|---|---|

| Child’s education (10 years away) | Long | SIP (discipline) + lump sum (if markets correct) |

| Retirement (20+ years) | Very long | SIP (consistent) + lump sum (windfalls) |

| House down payment (3 years) | Medium | Debt fund STP (capital preservation priority) |

| Emergency fund | Always | Liquid fund lump sum (no equity) |

FREQUENTLY ASKED QUESTIONS

Q1: Which gives higher returns – SIP or lump sum?

It depends on market conditions. In rising markets, lump sum typically outperforms because full capital participates from day one. In falling or volatile markets, SIP often delivers better returns through rupee cost averaging . Over very long periods (15+ years), the difference narrows, and staying invested matters more than the method .

Q2: Is SIP better than lump sum for first-time investors?

Yes. SIP is generally recommended for first-time investors because it:

-

Provides gradual market exposure

-

Reduces emotional stress during volatility

-

Builds investment discipline

-

Requires no market timing expertise

Q3: Can I do both SIP and lump sum?

Absolutely. In fact, this is what many sophisticated investors do:

-

Regular SIPs from monthly income

-

Lump sum investments from bonuses or windfalls

-

Additional lump sums during market corrections

Q4: What is the minimum amount for SIP vs lump sum?

| Method | Minimum Amount |

|---|---|

| SIP | As low as ₹500 per month |

| Lump Sum | Typically ₹5,000 (some funds allow ₹1,000) |

Q5: How does tax treatment differ between SIP and lump sum?

Tax rules are the same for both, but holding period calculation differs. With SIP, each installment has a different purchase date, so when you redeem, FIFO applies—older units may be long-term, newer ones short-term. Lump sum has a single purchase date, simplifying tax calculation .

Q6: What is STP and when should I use it?

Systematic Transfer Plan (STP) involves parking a lump sum in a debt fund and transferring fixed amounts monthly to an equity fund. Use STP when:

-

Markets are at all-time highs

-

You’re nervous about investing a large amount

-

You have a 3-5 year horizon and want to reduce timing risk

Q7: Is 2026 a good time for lump sum investment?

It depends on your goal and the specific market segment. As of early 2026:

-

Large-cap valuations are near long-term averages

-

Mid-cap and small-cap valuations are elevated

-

Consider hybrid funds (balanced advantage, multi-asset) for lump sum

-

Use STP for pure equity exposure

Q8: Can I convert my SIP into lump sum later?

You can’t “convert” existing SIPs, but you can:

-

Increase SIP amount (step-up SIP)

-

Make additional lump sum purchases in the same fund

-

Start a new lump sum investment alongside existing SIP

Q9: What if markets crash after I invest a lump sum?

Don’t panic. If you have a long-term horizon (5+ years), history shows markets recover . The 2008 crash, COVID-19 crash—all were followed by strong recoveries. Consider it an opportunity to average down if you have additional cash .

Q10: Which is better for retirement planning – SIP or lump sum?

Both have their place:

-

SIPs are ideal for building retirement corpus through regular savings

-

Lump sums work well for deploying annual bonuses or inheritance

-

Many retirement calculators assume SIP-like contributions

-

A combination provides flexibility and potential for higher corpus

ACTIONABLE CHECKLIST: CHOOSE YOUR STRATEGY

Before You Invest

-

Identify source of funds: Regular income (SIP) or windfall (lump sum)

-

Check current market valuations (Nifty PE, sector-specific)

-

Honestly assess your risk tolerance (can you handle a 15% drop?)

-

Define investment horizon (minimum 3-5 years for equity)

-

Set clear goals (retirement, education, wealth creation)

For SIP Investors

-

Choose fund type based on goal (large-cap for stability, flexi-cap for flexibility)

-

Decide SIP amount (start with what’s comfortable, increase annually)

-

Set up auto-debit mandate

-

Link to mobile for tracking

-

Consider step-up SIP (increase 10% annually)

-

Don’t stop SIP during market falls – that’s when you benefit most

For Lump Sum Investors

-

If markets are at highs, consider STP instead

-

For direct lump sum, consider balanced advantage funds for downside protection

-

Keep some cash aside for emergencies—don’t invest everything

-

Have a clear exit strategy (goal-based)

-

Don’t check portfolio daily—it causes emotional decisions

For STP Investors

-

Choose a reliable liquid/debt fund for parking

-

Decide transfer frequency (monthly is standard)

-

Set STP duration (6-12 months typical)

-

Ensure target equity fund aligns with goals

-

Review after STP completes

Post-Investment Discipline

-

Review portfolio annually (not daily)

-

Rebalance if asset allocation drifts

-

Increase SIP amounts as income grows

-

Stay invested through market cycles

-

Consult advisor for major life changes

CONCLUSION: THE REAL WINNER IS YOU, STAYING INVESTED

After all the analysis, numbers, and scenarios, one truth emerges clearly: the real winner isn’t SIP or lump sum—it’s the investor who stays invested through market ups and downs .

Consider this: A study of the Nifty 50 TRI over 24 years showed that missing just the 50 best trading days would have reduced your returns from 15.61% CAGR to less than 1% . The best days often come right after the worst days—precisely when many investors panic and exit.

So whether you choose SIP, lump sum, or a hybrid STP approach, the most important decision is to start and stay.

For 2026, Here’s Your Action Plan

- If you have regular income: Start a SIP today—even ₹1,000 monthly makes a difference

- If you have a windfall: Consider market valuations—use STP if uncertain, lump sum if confident

- If you’re confused: Do both—70% SIP, 30% lump sum (or STP)

- If markets correct: Don’t panic—if anything, consider investing more

- If markets rally: Stay disciplined—don’t exit prematurely

Tools to Help You Decide

Use India Tax Tools’ Investment Calculators to:

-

SIP Calculator: See how your monthly investments grow over time

-

Lump Sum Calculator: Project future value of one-time investments

-

Goal Planner: Determine required SIP/lump sum for your goals

-

Tax Calculator: Understand post-tax returns

Final Thought

As Morgan Housel wisely noted: “No one’s success is proven until they have survived a calamity” . In investing, the ultimate test isn’t picking the perfect entry point—it’s staying calm, disciplined, and invested when everything around you seems chaotic.

SIP gives you that discipline automatically. Lump sum tests your resolve immediately. Choose based on who you are, not just what the numbers say.

Start today. Stay invested. Let time do its magic.

“SIP vs lump sum is the wrong question. The right question is: ‘Will I stay invested through the next crash?’ Because markets reward those who stay, not those who time.”

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. Please consult your financial advisor before making investment decisions. The information provided is based on data available as of February 2026.