Meet Rajesh, who runs a successful electronics trading business in Delhi. Last year, his turnover touched ₹1.2 crore. His CA casually mentioned, “You might need a tax audit this year.” Rajesh panicked—what’s a tax audit? Does it mean the IT department is investigating him? Will it cost him a fortune?

Then there’s Priya, a freelance graphic designer in Mumbai with ₹65 lakh in receipts. She’s heard about tax audit but isn’t sure if it applies to professionals. Her friend told her about “presumptive taxation,” but she’s confused.

If you’re a business owner or professional, tax audit under Section 44AB is one of the most critical compliance requirements you’ll face. And no, it’s not a “raid” or investigation—it’s a statutory audit of your books by a Chartered Accountant.

In 2026, with updated threshold limits and stricter reporting requirements, understanding tax audit is essential to avoid penalties and stay compliant.

In this comprehensive guide, you’ll discover:

-

What tax audit is (and what it isn’t)

-

Threshold limits for businesses and professionals (updated for FY 2025-26)

-

Presumptive taxation rules—when audit is NOT required

-

Who needs audit even below thresholds (special cases)

-

Required documents—complete checklist for your CA

-

Due dates for audit report filing

-

Penalties for non-compliance

-

Step-by-step process of tax audit

-

Common mistakes to avoid

Let’s demystify tax audit—so you can face it with confidence.

WHAT IS TAX AUDIT UNDER SECTION 44AB?

Tax audit is a examination of your business or profession’s accounts by a Chartered Accountant, mandated by Section 44AB of the Income Tax Act.

What Tax Audit IS

What Tax Audit IS NOT

Why Was Tax Audit Introduced?

The government introduced tax audit to:

- Ensure proper maintenance of books by businesses

- Verify correct income computation and claim of deductions

- Check compliance with tax laws

- Reduce tax evasion by under-reporting income

- Provide detailed information to tax authorities through Form 3CD

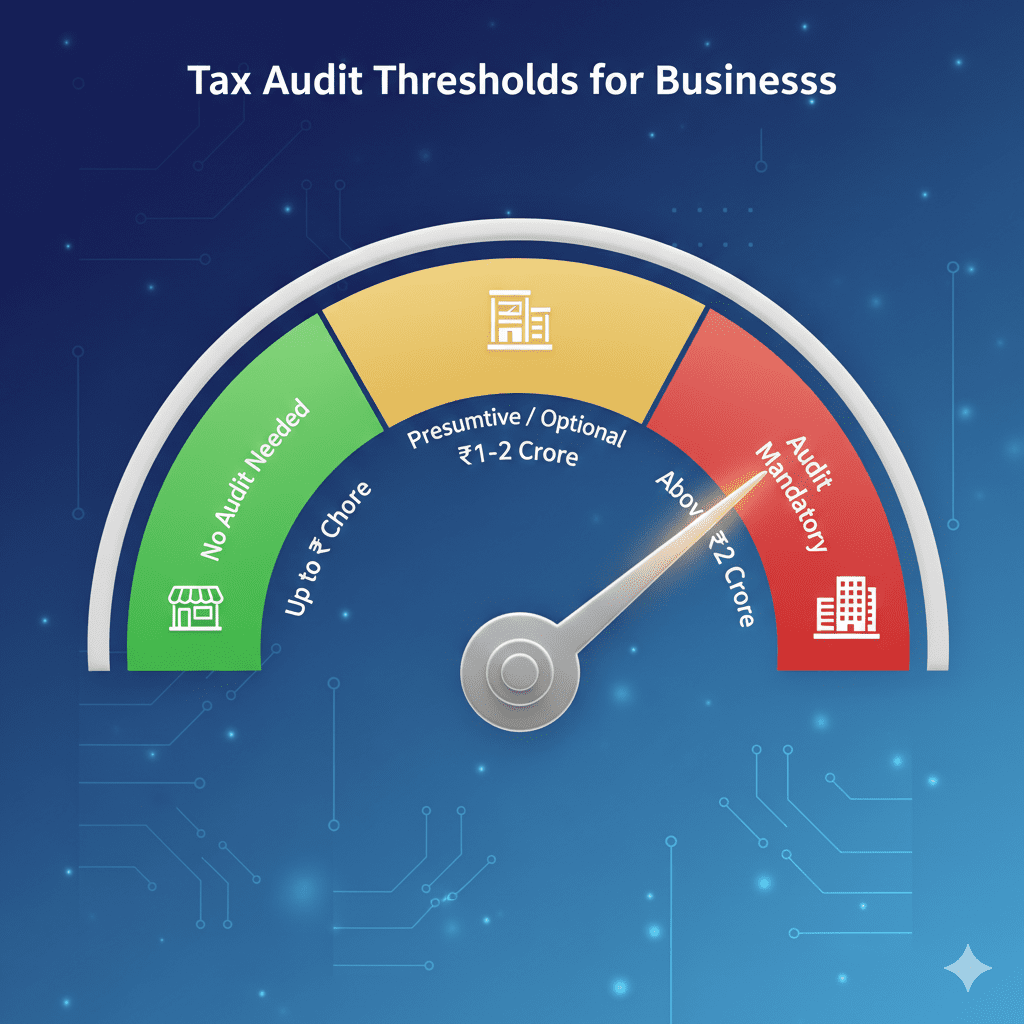

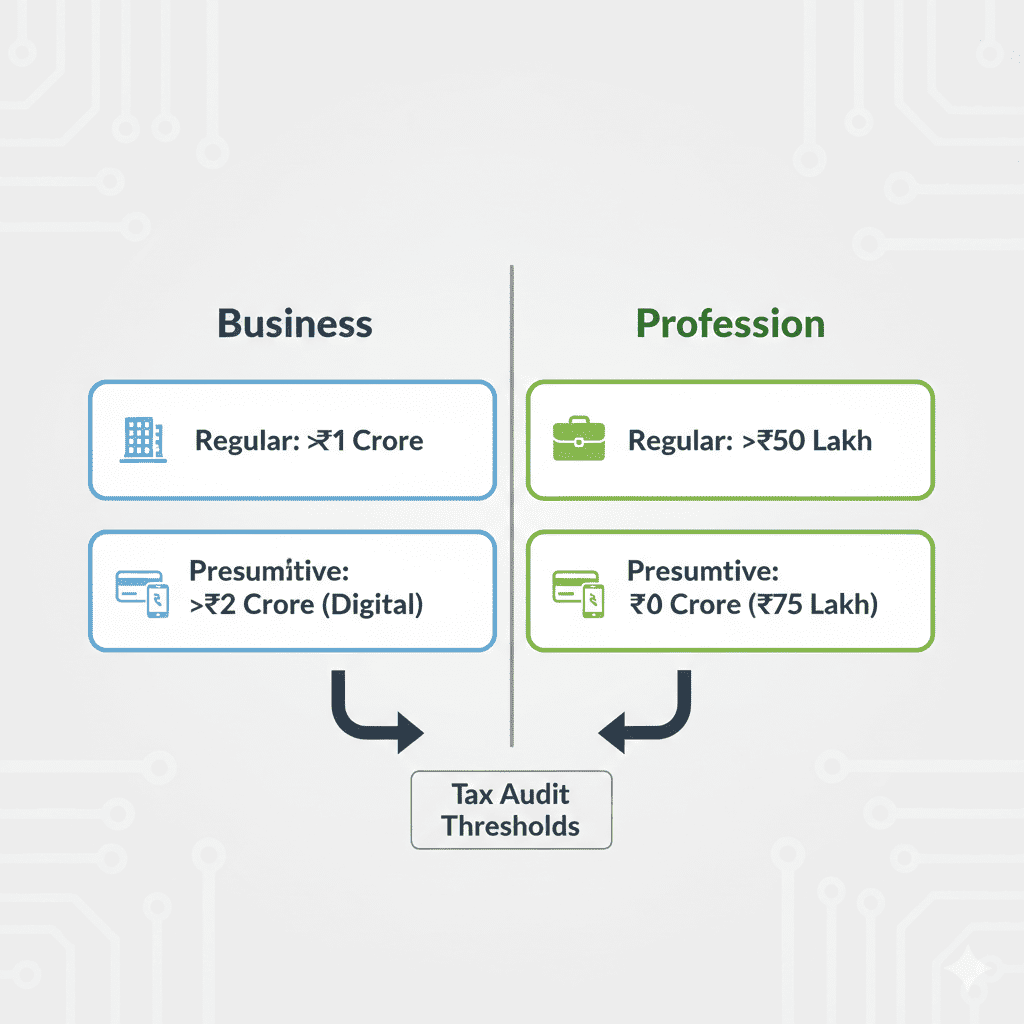

THRESHOLD LIMITS FOR TAX AUDIT (FY 2025-26)

The threshold for tax audit depends on whether you’re in business or profession, and whether you opt for presumptive taxation.

For Businesses (Section 44AB)

Key Updates for 2026:

-

The ₹1 crore threshold remains for regular businesses

-

For businesses opting for presumptive taxation under Section 44AD, the threshold for audit is ₹2 crore (if at least 95% of transactions are digital)

For Professionals (Section 44AB)

Key Updates for 2026:

-

The threshold for professionals under presumptive taxation (Section 44ADA) increased to ₹75 lakh (from ₹50 lakh)

-

This applies to specified professions (legal, medical, engineering, architecture, accountancy, etc.)

Summary Table: Tax Audit Thresholds 2026

*Source: Income Tax Act, Section 44AB, as amended by Finance Act 2026 *

WHEN AUDIT IS REQUIRED EVEN BELOW THRESHOLDS

In certain cases, tax audit is mandatory even if your turnover/receipts are below the threshold.

Special Cases Triggering Tax Audit

Example: Loss Case

Scenario: Vikram’s trading business has turnover of ₹90 lakh (below ₹1 crore), but he incurred a loss of ₹2 lakh.

Example: Lower Profit than Presumptive

Scenario: Priya is a lawyer with gross receipts of ₹60 lakh. She opts for presumptive taxation under 44ADA, but declares only 40% profit (₹24 lakh) instead of presumptive 50%.

PRESUMPTIVE TAXATION AND AUDIT EXEMPTION

Presumptive taxation schemes allow small taxpayers to declare income at prescribed rates without maintaining detailed books—and avoid tax audit.

Section 44AD (Businesses)

Section 44ADA (Professionals)

Important Conditions

- Digital receipts: To claim 6% presumptive rate for business, at least 95% of receipts must be through digital mode

- Five-year rule: Once you opt for presumptive, you must continue for 5 years; exiting earlier means no presumptive for next 5 years

- No deductions: Under presumptive, you cannot claim separate deductions for expenses (they’re deemed included in profit rate)

Example: When Audit is Avoided

Scenario: Rajesh’s trading business has turnover ₹1.8 crore, all digital receipts.

Tax saved: No audit fee (₹15,000-₹30,000) + simpler compliance

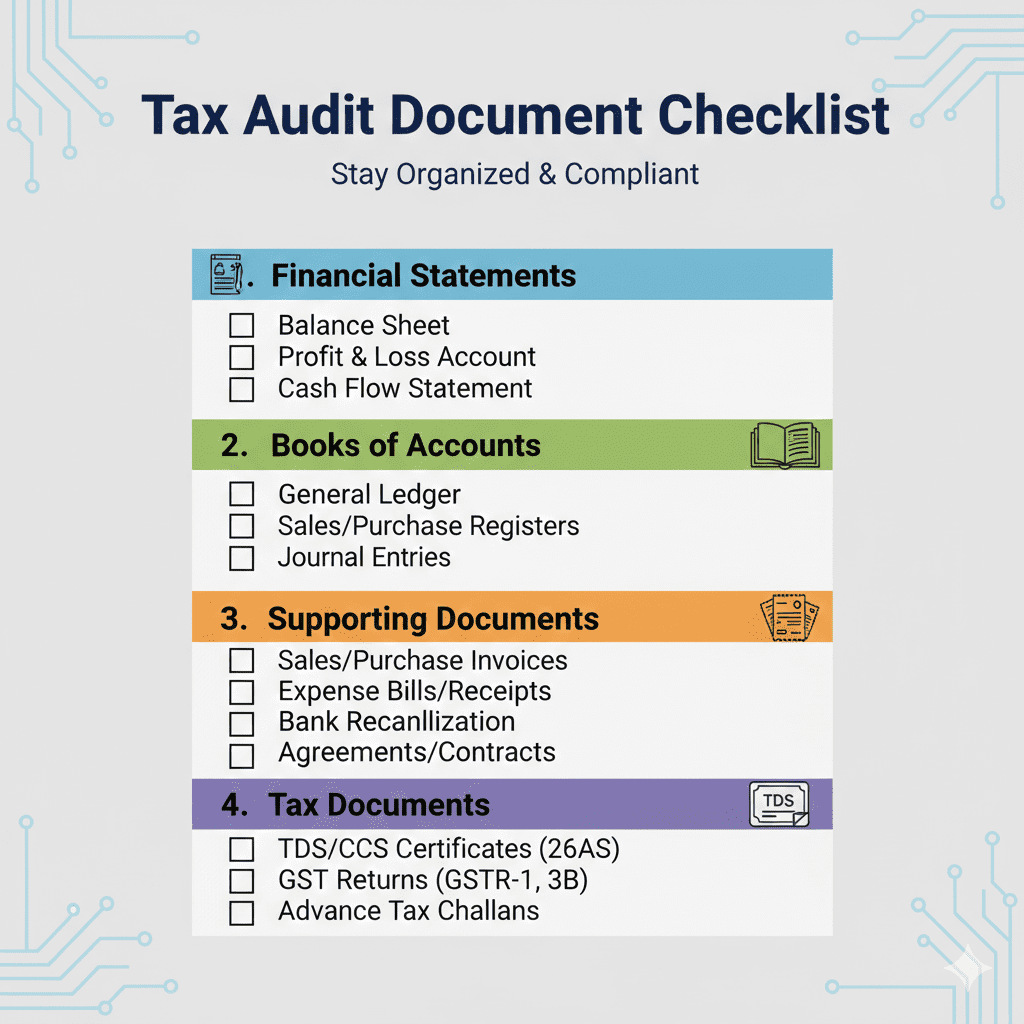

REQUIRED DOCUMENTS FOR TAX AUDIT

Proper documentation makes tax audit smooth and cost-effective. Here’s your complete checklist.

Financial Statements

Books of Accounts

Supporting Documents

Tax-Related Documents

Specific Documents for Audit Report (Form 3CD)

Form 3CD requires detailed information. Your CA will need:

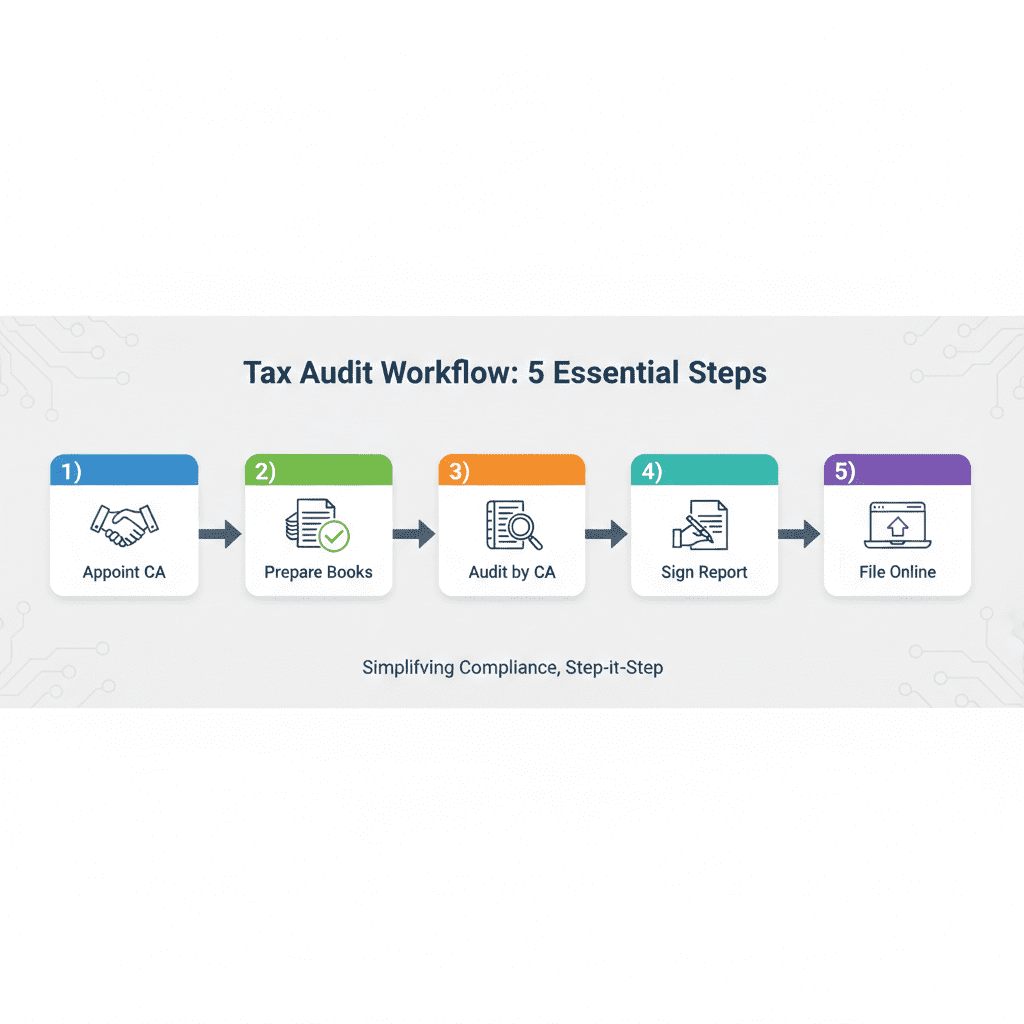

TAX AUDIT PROCESS: STEP-BY-STEP

Step 1: Appointment of Auditor

-

Appoint a Chartered Accountant before the end of financial year (ideally)

-

Provide engagement letter confirming scope of audit

-

Discuss timelines and fees

Step 2: Preparation of Books

-

Ensure all books are updated till 31st March

-

Reconcile bank statements, GST returns, TDS statements

-

Prepare trial balance and draft financials

Step 3: Audit by CA

Your CA will:

-

Verify books with supporting documents

-

Check compliance with Income Tax Act

-

Identify any discrepancies or adjustments

-

Prepare audit report in Form 3CB/3CD

Step 4: Finalization and Signing

-

Review draft audit report

-

Make any agreed adjustments

-

Sign audit report (CA digital signature)

-

Obtain your acceptance

Step 5: Filing on Income Tax Portal

Due Date: 30th September 2026 for AY 2026-27

Step 6: Filing Income Tax Return

After audit report is filed, you file your ITR (by 31st October for audit cases).

TAX AUDIT REPORT: FORM 3CB AND 3CD EXPLAINED

The tax audit report consists of two parts.

Form 3CB (Audit Report)

This is the certificate by the CA stating that:

-

They have examined the accounts

-

Books are maintained as per law

-

Financial statements give a true and fair view

-

Particulars in Form 3CD are true and correct

Form 3CD (Statement of Particulars)

This is the detailed information required under the Act. It has 44 clauses covering:

Sample Clauses

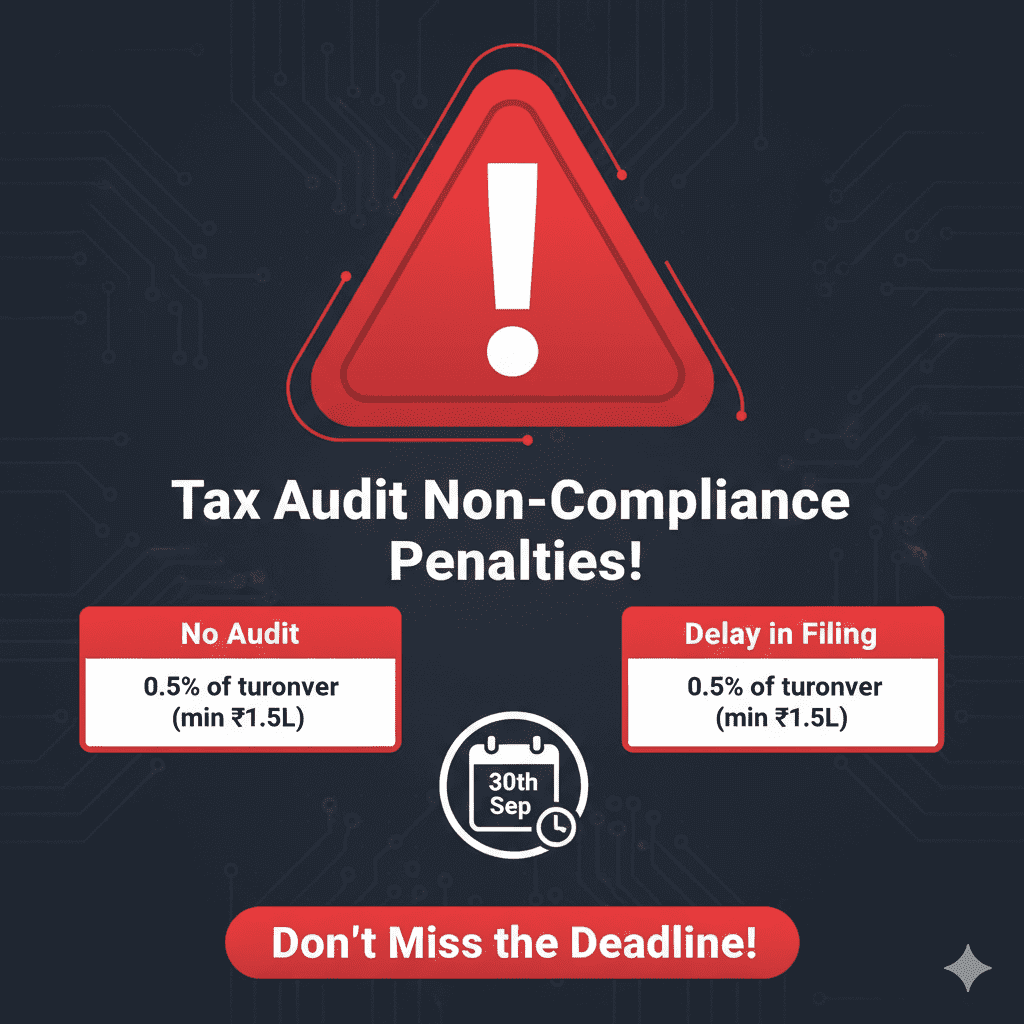

DUE DATES AND PENALTIES

Tax Audit Due Dates (AY 2026-27)

Penalty for Non-Compliance (Section 271B)

Example: Turnover ₹2 crore, penalty = 0.5% = ₹1,00,000 (since less than ₹1.5L)

Interest on Tax Due

If audit delay causes delay in tax payment:

COMMON MISTAKES AND HOW TO AVOID THEM

FREQUENTLY ASKED QUESTIONS

Q1: What is the turnover limit for tax audit in 2026?

For businesses:

For professionals:

Q2: Who is exempt from tax audit?

You are exempt if:

Q3: What is the penalty for not getting tax audit done?

Penalty under Section 271B is 0.5% of turnover or gross receipts, or ₹1,50,000—whichever is lower .

Q4: Can I do tax audit myself?

No. Tax audit must be conducted by a practicing Chartered Accountant. You cannot audit your own books.

Q5: What is the due date for tax audit report?

Tax audit report (Form 3CB/3CD) must be filed by 30th September 2026 for AY 2026-27 . ITR for audit cases is due 31st October.

Q6: Is tax audit required if I have a loss?

Yes. If you have business/profession loss and are not opting for presumptive taxation, audit is required to verify and allow loss to be carried forward .

Q7: What is Form 3CD?

Form 3CD is the statement of particulars that forms part of the tax audit report. It contains 44 clauses with detailed information about your business, accounts, expenses, transactions, and tax compliance.

Q8: Do I need tax audit if I’m a freelancer?

Freelancers are treated as professionals. If your gross receipts exceed ₹50 lakh (regular) or ₹75 lakh (presumptive under 44ADA), you need tax audit. If you declare less than 50% profit under presumptive, audit is required regardless of receipts.

Q9: What documents are needed for tax audit?

See the detailed checklist in Section 6. Key documents include: financial statements, books of accounts, bank statements, invoices, TDS certificates, GST returns, and prior year ITR.

Q10: Can I file ITR before tax audit?

No. For audit cases, ITR can only be filed after the audit report is uploaded on the portal. The ITR form will prompt for audit details.

ACTIONABLE CHECKLIST: PREPARE FOR TAX AUDIT

Throughout the Year

-

Maintain proper books of accounts (cash book, bank book, ledgers)

-

Reconcile bank statements monthly

-

Deduct TDS on eligible payments and deposit on time

-

File TDS returns quarterly

-

Reconcile GST returns with books monthly

-

Keep all invoices and supporting documents organized

3 Months Before Year-End (Jan-Mar 2026)

-

Review turnover/receipts—estimate if threshold will be crossed

-

If close to threshold, plan accordingly (consider digital receipts for lower presumptive rate)

-

Appoint CA for audit if required

-

Complete physical stock verification

After Year-End (Apr-Jun 2026)

-

Finalize books of accounts

-

Prepare trial balance and draft financials

-

Provide all documents to CA

-

Respond to CA queries promptly

-

Review draft audit report

Before 30th September 2026

-

Ensure audit report is finalized and signed

-

Verify that CA has uploaded Form 3CB/3CD on portal

-

Confirm receipt of acknowledgement

Before 31st October 2026

-

File income tax return (ITR-3, ITR-4, or ITR-5/6)

-

Verify that audit details are correctly entered in ITR

-

E-verify ITR

CONCLUSION: TAX AUDIT MADE SIMPLE

Tax audit under Section 44AB need not be intimidating. It’s a statutory requirement designed to ensure transparency and accuracy in income reporting. With proper preparation, it becomes a routine annual exercise.

Key Takeaways

- Know your threshold: ₹1 crore for business (regular), ₹2 crore (presumptive with digital); ₹50 lakh for profession (regular), ₹75 lakh (presumptive)

- Presumptive taxation: Can help you avoid audit if you declare prescribed profit

- Loss cases: Audit required even below thresholds to carry forward loss

- Documents matter: Organized records make audit smooth and cost-effective

- Deadlines: Audit report by 30th September; ITR by 31st October

- Penalties: 0.5% of turnover for non-compliance—avoid at all costs

Your Next Steps

-

Calculate your turnover/receipts for FY 2025-26—are you crossing thresholds?

-

If yes, start preparing documents now

-

Use India Tax Tools’ Tax Audit Readiness Tool to assess your preparedness

-

Consult your CA early—don’t wait until August

-

Maintain digital records—use accounting software for easier compliance

Remember: A smooth tax audit is a sign of a well-managed business. Embrace it as an opportunity to get your financial house in order.

“Tax audit isn’t a punishment—it’s a health checkup for your business finances. Embrace it, prepare for it, and let it strengthen your compliance.”

Disclaimer: This article is for informational and educational purposes only. Tax laws, thresholds, and due dates are subject to change based on government notifications. Please consult your Chartered Accountant for advice tailored to your specific situation. The information provided is based on Budget 2026 announcements and current provisions as of February 2026.

India Tax ToolsFebruary 24, 202610 Mins read36

India Tax ToolsFebruary 24, 202610 Mins read36

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment