Tax Benefits on Digital Payments: Save Extra Money in 2026

Whether you’re a salaried professional, a freelancer, or a small business owner, understanding how to leverage these tax benefits on digital payments can add up to significant savings. This comprehensive guide will walk you through everything you need to know: from Section 80G deductions on digital donations to tracking business expenses and maximizing cashback offers that reduce your taxable income.

By the end of this article, you’ll have a clear roadmap to save extra money in 2026 simply by changing how you pay. Let’s dive into the digital payment revolution that’s not just convenient—it’s financially smart.

Section 1: Understanding the Digital Payment Tax Landscape in 2026

The financial year 2025-26 (Assessment Year 2026-27) brings continuity to India’s digital payment incentives while introducing subtle shifts that smart taxpayers can exploit. The government’s vision of a less-cash society isn’t just about convenience—it’s backed by concrete tax provisions.

The Regulatory Framework

The Income Tax Act, through various sections, encourages digital transactions by:

-

Providing deductions for payments made through digital modes

-

Offering presumptive taxation benefits for businesses accepting digital payments

-

Creating disincentives for large cash transactions

Key sections to remember:

-

Section 80G: 50% or 100% deduction on donations made digitally

-

Section 44AD: Higher presumptive income limit for businesses receiving digital payments

-

Section 40A(3): Disallowance of expenses above ₹10,000 paid in cash

Why 2026 Is Different

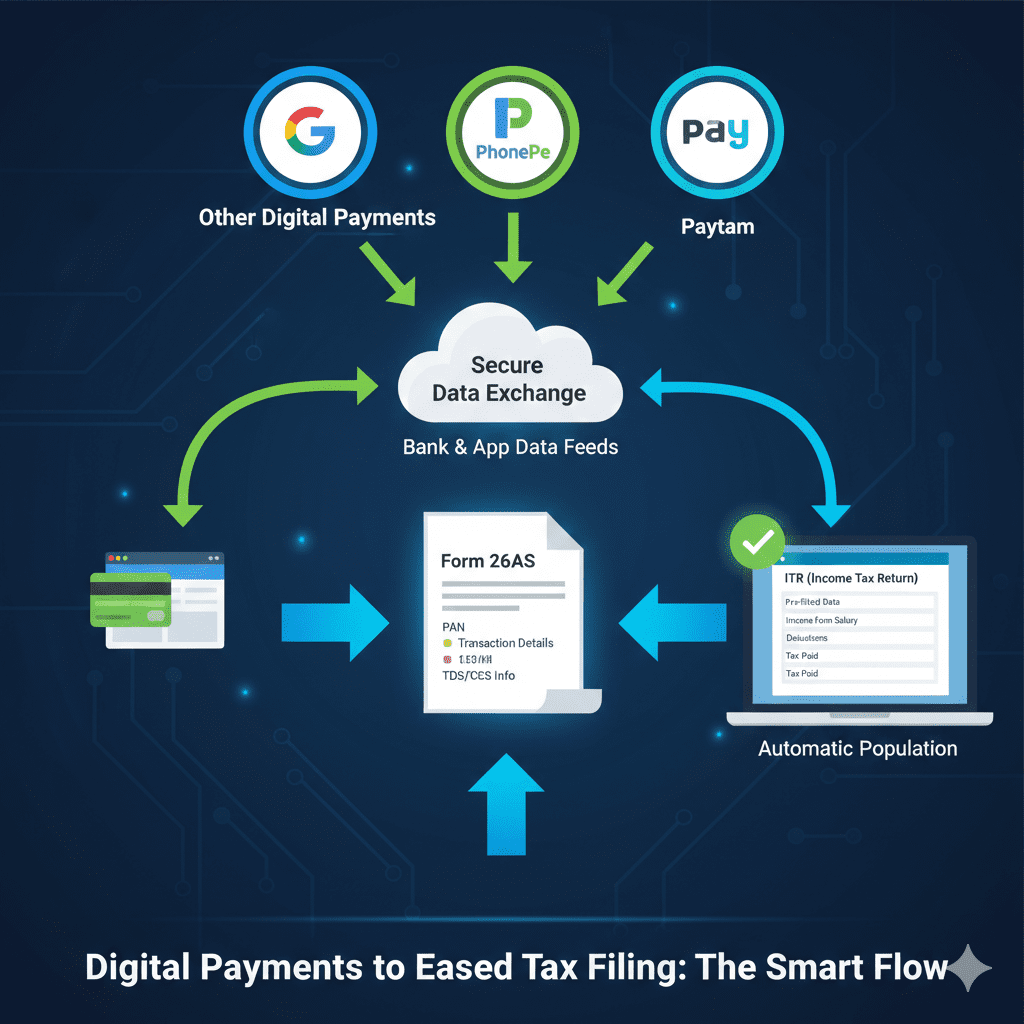

This year, the government has streamlined the process of claiming these benefits through pre-filled ITR forms. The Income Tax Department now automatically populates your digital payment data from sources like:

-

Bank statements

-

Payment gateways (Paytm, PhonePe, Google Pay)

-

UPI transaction history

This means less paperwork for you and better compliance tracking—but it also means you need to understand exactly which transactions qualify for benefits.

![]()

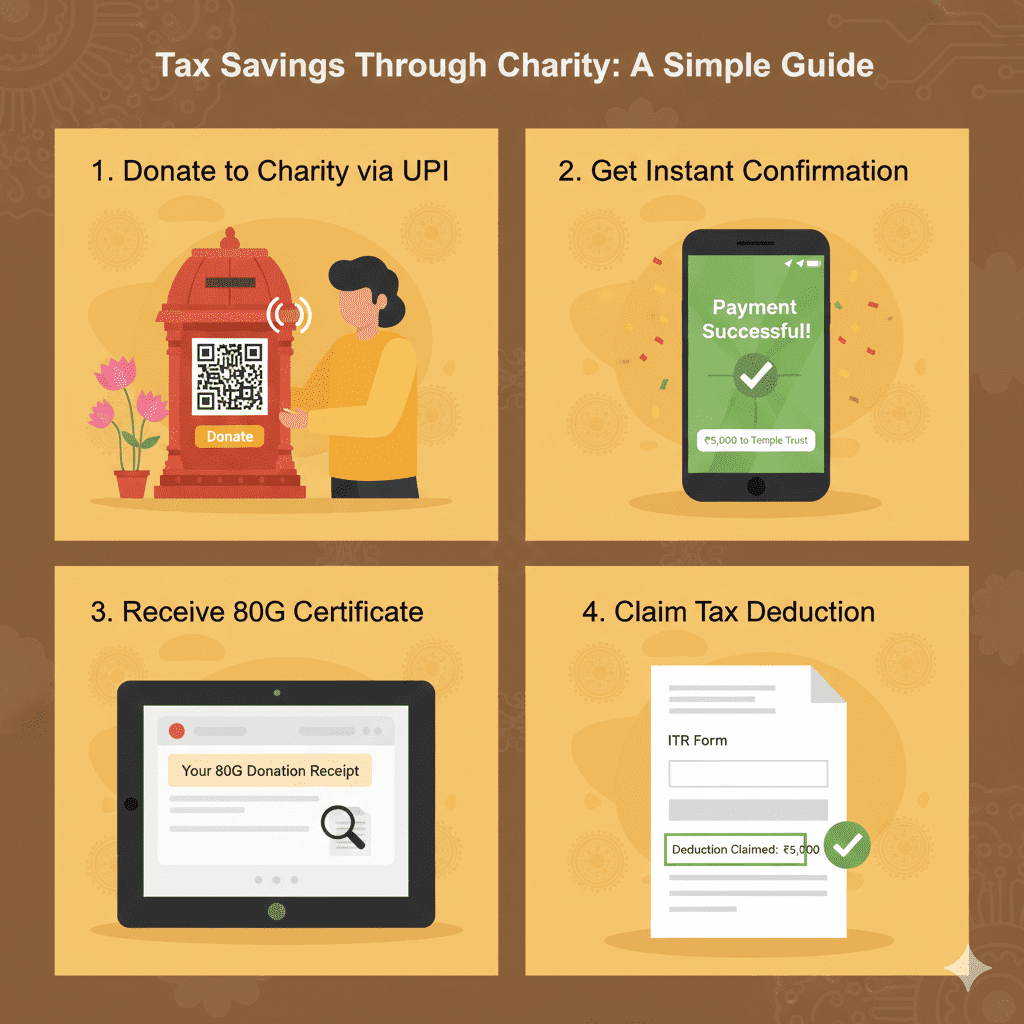

Section 2: Section 80G – Double Benefits on Charitable Donations

One of the most straightforward ways to save tax through digital payments is by making charitable donations online. Section 80G offers deductions on donations to specified funds and charitable institutions—and doing it digitally often provides additional proof and tracking benefits.

How It Works

When you donate to a registered charity through digital modes:

- You receive an instant 80G receipt via email

- The transaction is automatically recorded in your bank statement

- You can claim 50% or 100% deduction (depending on the organization)

Example: If you donate ₹10,000 to a 100% deduction eligible charity via UPI, your taxable income reduces by ₹10,000. In the 30% tax bracket, that’s ₹3,000 in actual tax savings.

Maximizing Section 80G Benefits

| Strategy | Digital Method | Tax Impact |

|---|---|---|

| Monthly donations | Set up auto-debit from savings account | Consistent deduction proof |

| Year-end giving | UPI transfer before March 31 | Last-minute tax planning |

| Corporate donations | Net banking with PAN linkage | Business expense + 80G |

Tools to Track Donations

Using India Tax Tools’ Donation Tracker, you can:

-

Log all digital donations with 80G certificates

-

Calculate total deduction eligible amount

-

Generate reports for your CA during filing

Pro Tip: Always verify the charity’s 80G validity on the Income Tax portal before donating. Fake charities are common, and digital payments don’t automatically guarantee genuineness.

Section 3: Business Expenses – The Digital Trail Advantage

For freelancers, consultants, and small business owners, digital payments create an automatic expense trail that’s invaluable during tax assessment.

Presumptive Taxation Under Section 44AD

If you opt for presumptive taxation scheme (Section 44AD), digital payments offer a distinct advantage:

-

Presumptive income limit is 8% for cash receipts

-

But only 6% for digital receipts (if total turnover is less than ₹2 crore)

What this means: For every ₹1 lakh you receive digitally, your presumptive income is ₹6,000 instead of ₹8,000—effectively reducing your tax liability.

Documenting Business Expenses

Digital payments create an audit trail that satisfies tax officers. Every business expense paid digitally:

-

Appears in your bank statement

-

Has a timestamp and merchant details

-

Can be linked to invoices electronically

Tools to Simplify Tracking

The Business Expense Tracker helps you:

- Categorize digital payments by expense type

- Generate expense reports for tax filing

- Flag non-deductible expenses automatically

![]()

Common Deductible Digital Payments

-

Rent: Pay through NEFT/UPI to claim HRA or business rent deduction

-

Professional fees: Payments to consultants, lawyers, CAs

-

Utilities: Electricity, internet, phone bills paid online

-

Office supplies: Amazon Business, stationary portals

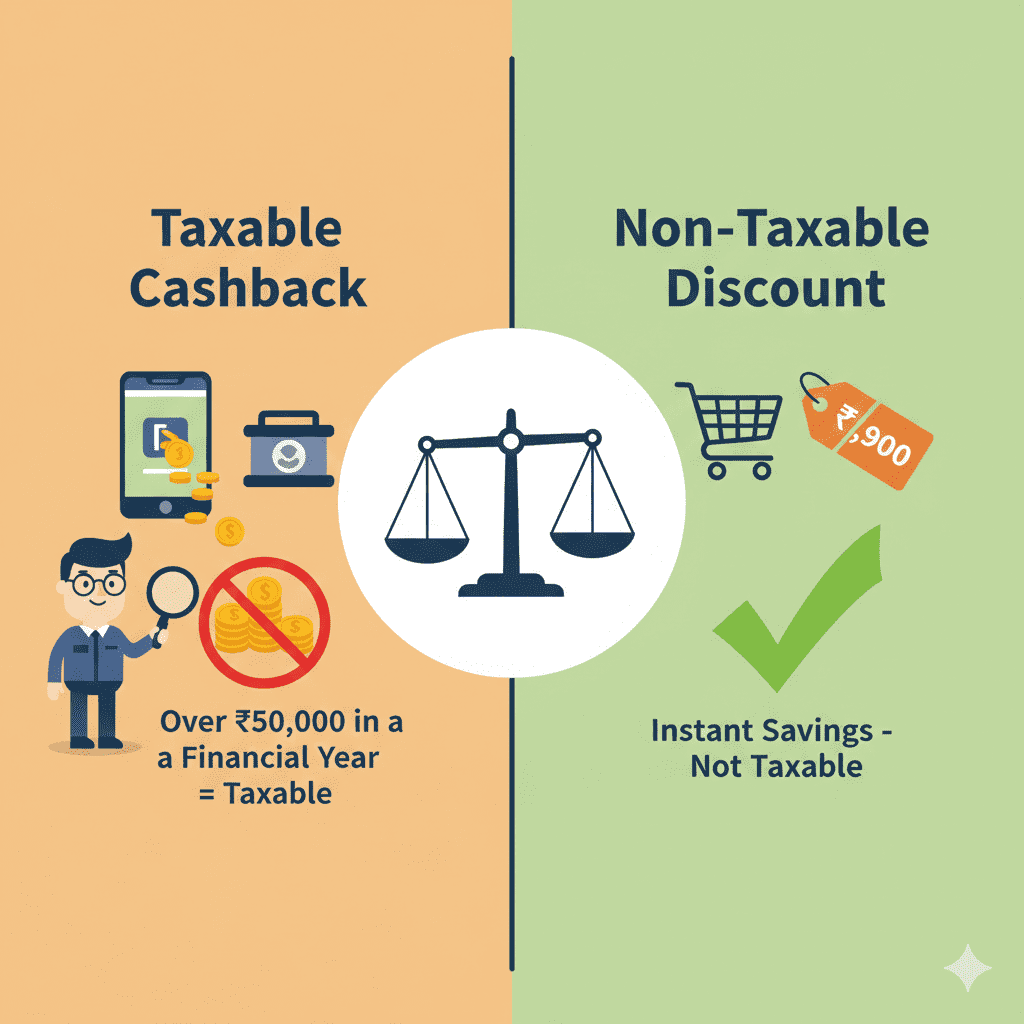

Section 4: Cashback and Rewards – Tax-Free or Taxable?

Cashbacks and rewards on digital payments create confusion: are they taxable income or discounts? The answer depends on how you receive them.

Classification Rules

| Type of Reward | Tax Treatment | Example |

|---|---|---|

| Discount on purchase | Not taxable | ₹50 off on ₹500 bill via coupon |

| Cashback to bank account | Taxable as income | ₹100 credited to savings account |

| Reward points | Taxable when converted to cash | Points redeemed for statement credit |

| Gift vouchers | Taxable if from business | Amazon voucher worth ₹5,000 |

The ₹50,000 Threshold

Under Section 56(2)(x), gifts exceeding ₹50,000 in value are taxable as “Income from Other Sources.” This includes:

-

Cashbacks accumulated during the year

-

Reward points converted to cash/goods

-

Referral bonuses from payment apps

Smart Strategy: Use cashbacks for immediate discounts rather than accumulating them. If you receive a ₹100 cashback as wallet money, use it immediately—it’s effectively a discount. If it sits in your bank, it’s taxable income.

Tracking Cashbacks for Tax Purposes

The Income from Other Sources Calculator helps you:

-

Track total cashbacks received during the year

-

Calculate taxable portion above ₹50,000

-

Include this in your ITR accurately

Section 5: The Digital Payment Ecosystem – Tools That Simplify Tax Compliance

India’s digital payment infrastructure has matured to the point where tax compliance can be almost automated—if you use the right tools.

Payment Apps with Tax Features

Several apps now offer built-in tax tracking:

| App | Tax Feature | Best For |

|---|---|---|

| Google Pay | Transaction categorization | Personal expense tracking |

| PhonePe | Annual tax statement download | Freelancers |

| Paytm | 80G certificate integration | Donors |

| CRED | Credit card payment tracking | High spenders |

Why Use Dedicated Tax Tools?

While payment apps provide basic data, dedicated tax tools offer deeper analysis. India Tax Tools provides:

-

Digital Payment Analyzer: Categorizes all UPI/card transactions by tax relevance

-

Section 80C Optimizer: Shows how digital investments (ELSS, PPF online) affect your tax

-

GST Calculator: For business owners tracking input tax credit on digital purchases

Setting Up Your Digital Tax System

- Link all payment methods to a single tracker (use CSV exports from apps)

- Tag transactions as personal/business/donation as you go

- Run monthly reports to see your tax-saving progress

- Share with your CA before March for last-minute planning

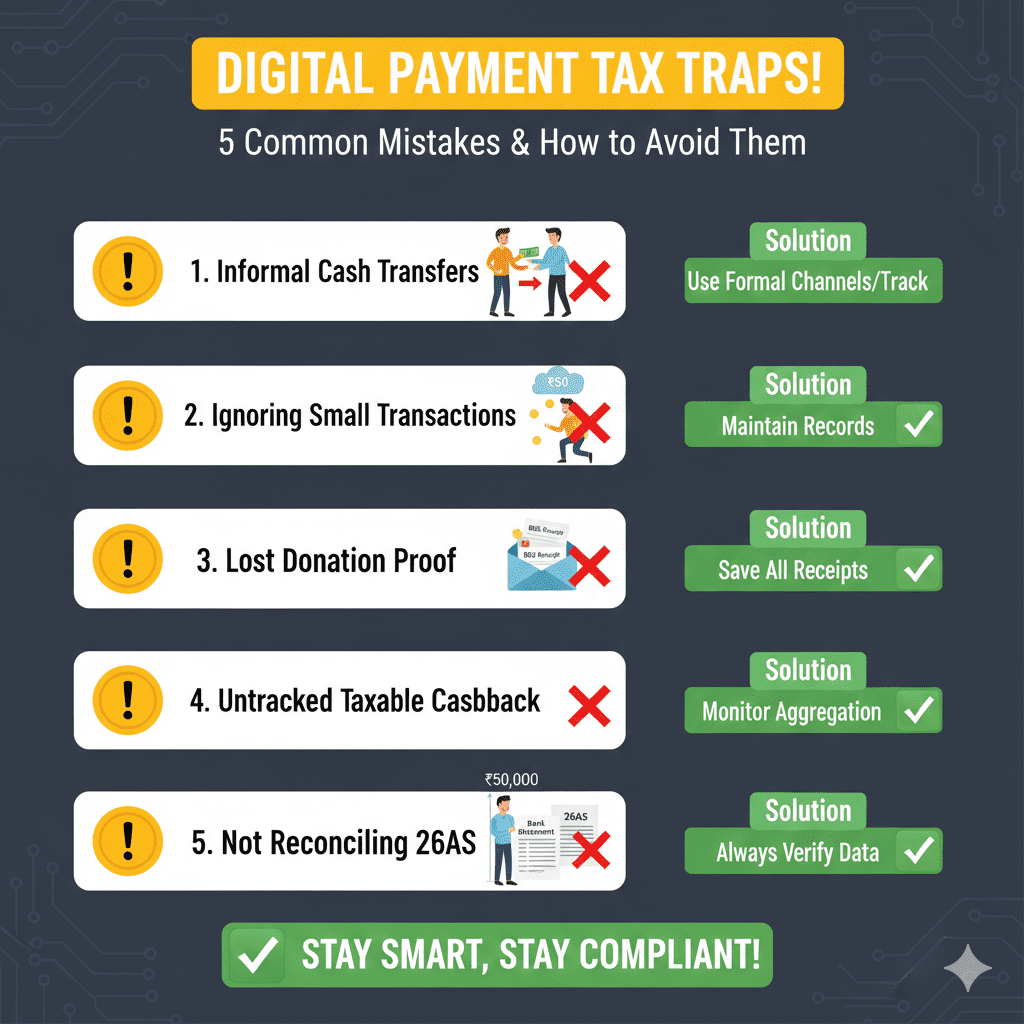

Section 6: Common Mistakes to Avoid in Digital Payment Tax Claims

Even smart taxpayers make errors that cost them deductions or trigger scrutiny. Here’s what to watch for in 2026.

Mistake 1: Treating All Digital Payments as Tax-Deductible

Only payments with specific purposes qualify:

-

❌ Paying friend ₹5,000 for dinner – Not deductible

-

✅ Paying CA ₹5,000 for tax consultation – Deductible

Mistake 2: Ignoring Small Transactions

Those ₹50 UPI payments to the vegetable vendor add up. If you’re a business claiming expense deductions, every eligible small payment counts. Use the Small Business Expense Tracker to aggregate these.

Mistake 3: Missing 80G Receipts

Digital donations automatically generate receipts, but they often go to spam. Set up filters to save all 80G emails in a dedicated folder.

Mistake 4: Confusing Cashbacks with Discounts

Remember the ₹50,000 rule. If you’re a heavy user of cashback apps, track all credits to your bank account separately.

Mistake 5: Not Reconciling with 26AS

The new ITR forms pull digital payment data directly into your 26AS. Always reconcile your claimed deductions with what appears in Form 26AS to avoid notices.

Section 7: Future Trends – What to Expect Beyond 2026

The digital payment tax landscape is evolving rapidly. Here’s what experts predict for the coming years.

Real-Time Tax Deductions

The government is piloting programs where TDS (Tax Deducted at Source) could be applied at the point of digital payment for certain high-value transactions. This would mean tax is deducted instantly, similar to how TDS works on salaries.

Blockchain-Based Tracking

By 2027, we may see blockchain integration where every digital payment creates an immutable tax record, eliminating the need for manual entry entirely.

Increased Limits for Digital Benefits

Expect the presumptive taxation benefit (6% for digital receipts) to extend to higher turnover limits, encouraging more businesses to go cashless.

Integration with Account Aggregators

The Account Aggregator framework will allow tax tools to securely pull your digital payment data from all sources with your consent, making tax filing nearly automatic.

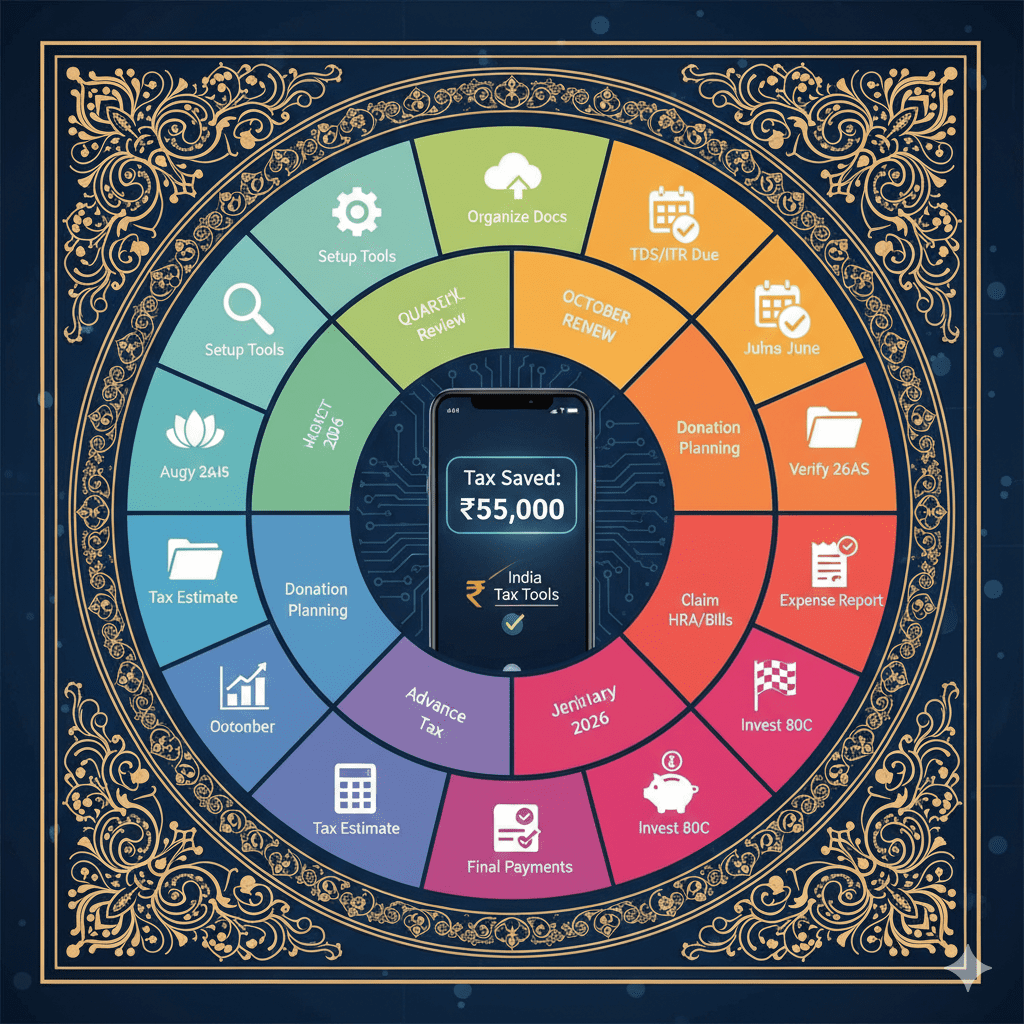

Section 8: Action Plan – Your 2026 Digital Tax Savings Checklist

Ready to start saving? Follow this month-by-month action plan:

April 2025 (Start of Financial Year)

-

Set up India Tax Tools account

-

Link all payment methods (bank accounts, UPI apps, cards)

-

Create folders for digital receipts (80G, business expenses)

Quarterly (June, September, December, March)

-

Run expense reports from your tracker

-

Verify all 80G receipts received

-

Check cashback accumulation against ₹50,000 threshold

January 2026

-

Estimate total tax liability using Advanced Tax Calculator

-

Plan March donations to optimize Section 80G

March 2026

-

Make final digital donations before March 31

-

Pay all pending business expenses digitally

-

Download annual transaction summaries from all apps

April-July 2026 (Filing Season)

-

Reconcile all digital payment data with Form 26AS

-

Upload categorized data to your CA

-

File ITR with all claimed deductions

Conclusion

The shift to digital payments in India isn’t just about convenience—it’s a financial strategy that can put real money back in your pocket. From Section 80G deductions on charitable donations to presumptive tax benefits for businesses and careful tracking of cashbacks, the opportunities to save are substantial.

By using smart tools like those at India Tax Tools, you can transform your everyday digital transactions into a systematic tax-saving machine. The key is awareness and consistency: know which payments qualify, track them diligently, and claim what’s rightfully yours.

As we move through 2026, the integration between digital payments and tax systems will only deepen. Those who adapt now will not only save money this year but will be ahead of the curve as India moves toward a fully digital tax ecosystem.

Your next step: Visit India Tax Tools and start your digital payment tax audit today. With 50+ free tools updated for AY 2026-27, you have everything you need to maximize your savings—all in one place, 100% private and secure.

Frequently Asked Questions

Q1: Are UPI payments automatically considered for tax deductions?

A: No. UPI payments are just transactions. You need to categorize them as eligible expenses (business, donation, investment) to claim deductions. The transaction itself doesn’t automatically qualify—the purpose matters.

Q2: What’s the maximum I can save using digital payment tax benefits?

A: There’s no fixed maximum—it depends on your income and spending. A salaried person donating ₹50,000 digitally could save ₹15,000 in taxes (30% bracket). A business owner with ₹10 lakh digital expenses could save over ₹3 lakh in taxes.

Q3: Do I need to keep paper records if I pay digitally?

A: Digital records (bank statements, payment app screenshots, email receipts) are generally sufficient. However, for donations, always download the official 80G receipt from the charity’s website—don’t rely solely on payment confirmation.

Q4: How do I prove a digital payment was for business?

A: Maintain an invoice or bill for the expense. The combination of digital payment proof + invoice creates a complete audit trail. Tools like India Tax Tools’ Invoice Generator can help you create professional records.

Q5: Are cashbacks from credit cards taxable?

A: Cashbacks credited to your bank account are taxable as “Income from Other Sources.” However, if you receive statement credits or discounts, they’re not taxable as they reduce your expense rather than adding to income.

Q6: What happens if I cross ₹50,000 in cashbacks?

A: The amount above ₹50,000 becomes taxable. You must declare it in your ITR under “Income from Other Sources.” Use the Other Income Calculator to compute exact tax liability.

Disclaimer: This article is for educational purposes only and does not constitute professional tax advice. Tax laws are subject to change, and individual situations vary. Always consult a qualified Chartered Accountant for advice specific to your circumstances. All tools mentioned are updated for Finance Act 2026 but should be used as guidance, not as final authority for tax filing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment