Meet Priya, 34, a marketing manager in Bangalore. She’s been investing in mutual funds for three years through SIPs. Last month, she redeemed a portion for her sister’s wedding and was shocked when her CA asked for ₹45,000 as tax on her gains. “But I’ve already paid tax on my income!” she thought. Then there’s Rajesh, 45, who received ₹1.2 lakh in dividends from his balanced fund and assumed it was tax-free—until the tax notice arrived.

If you’re a mutual fund investor, understanding the tax on your investments is as important as the returns themselves. A 2025 survey found that 62% of mutual fund investors are unaware of the tax implications of their redemptions, leading to last-minute tax shocks and even penalties.

Here’s the good news: mutual fund taxation follows clear rules. Once you understand them, you can plan your investments and redemptions to minimize your tax outgo legally.

In this comprehensive 2026 guide, you’ll discover:

-

LTCG vs STCG: The critical difference that changes your tax rate

-

Tax rates for equity, debt, and hybrid funds—side-by-side comparison

-

The ₹1.25 lakh exemption on equity LTCG (and how to use it)

-

Dividend taxation: Why dividends are now taxed in your hands (and at what rate)

-

Tax-saving with ELSS under Section 80C

-

Real examples with step-by-step calculations

-

Common mistakes that trigger tax notices

-

Smart strategies to reduce your tax burden

Let’s demystify mutual fund taxation—so you keep more of what you earn.

MUTUAL FUND TAXATION BASICS: TWO KEY CONCEPTS

Before diving into rates, you need to understand two fundamental concepts that apply to all mutual fund taxes.

Concept 1: Capital Gains vs. Income

When you invest in mutual funds, you can earn money in two ways:

| Type | What It Is | How It’s Taxed |

|---|---|---|

| Capital Gains | Profit from selling your units at a higher price than you bought | Capital gains tax (LTCG/STCG) |

| Dividend/IDCW | Periodic payouts from the fund’s earnings | Added to your income, taxed at slab rate |

Important: From 2020 onwards, dividends from mutual funds are no longer tax-free in the hands of investors. They are added to your income and taxed as per your slab rate . The fund also pays a Dividend Distribution Tax (DDT) before distributing.

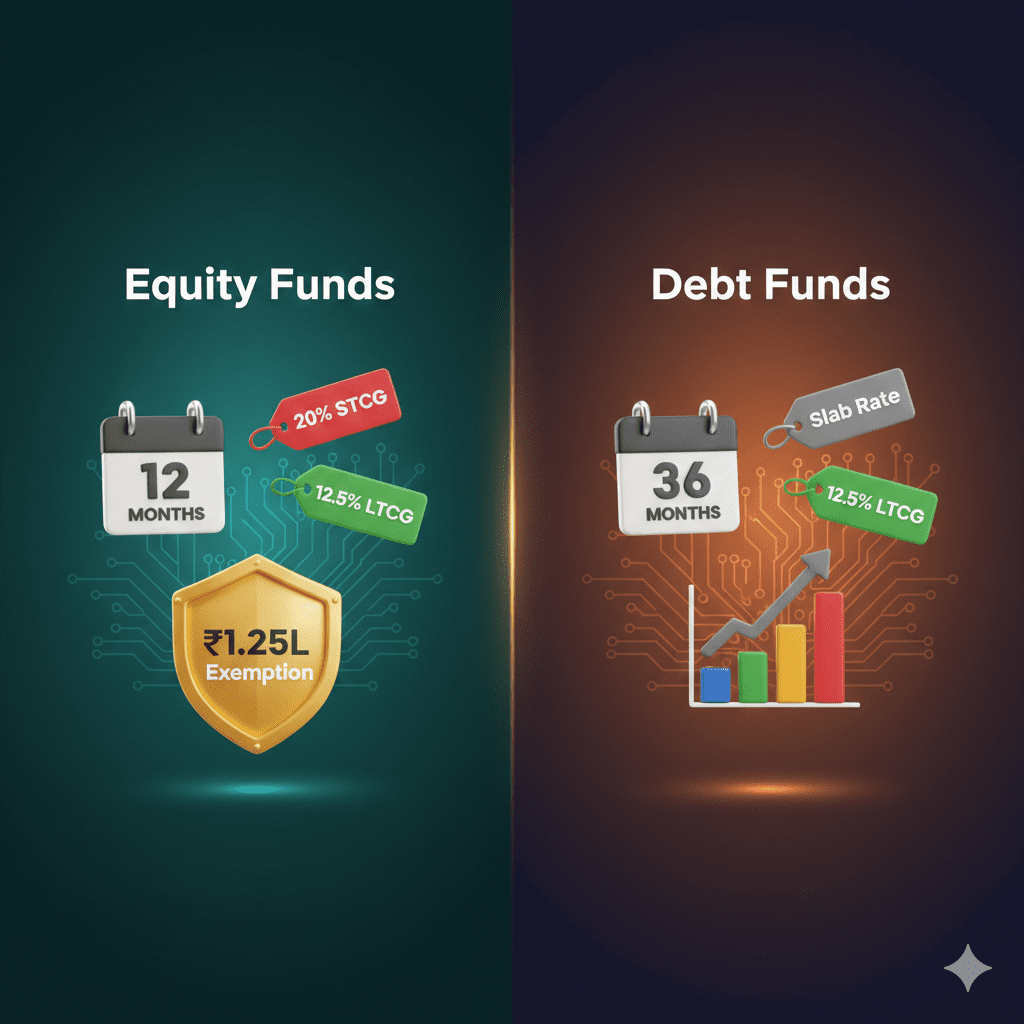

Concept 2: Holding Period Determines Tax Type

How long you held the units before selling determines whether your gain is Short-Term or Long-Term—and that decides the tax rate.

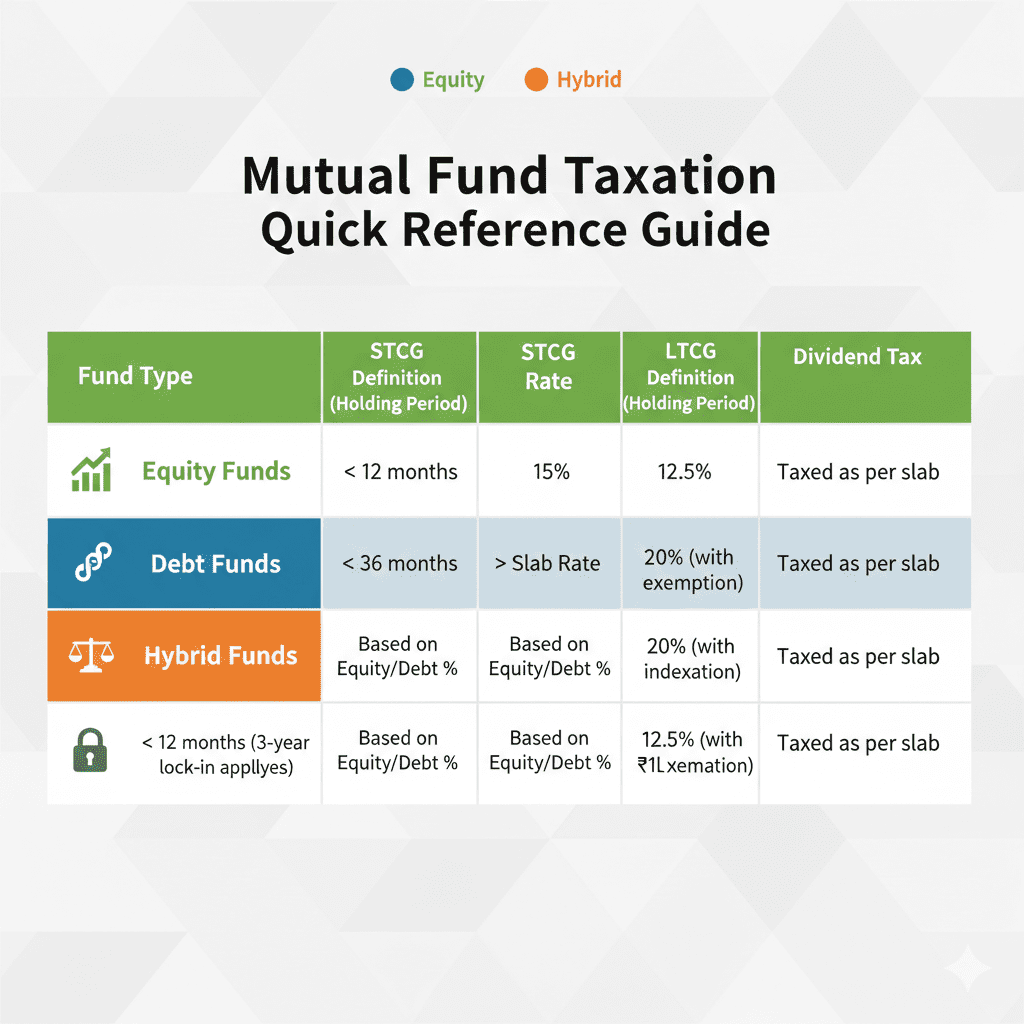

| Fund Type | Short-Term (STCG) | Long-Term (LTCG) |

|---|---|---|

| Equity-Oriented Funds | Held ≤ 12 months | Held > 12 months |

| Debt-Oriented Funds | Held ≤ 36 months | Held > 36 months |

*Source: Income Tax Act, Section 2(42A) *

Why this matters: LTCG is taxed at lower rates than STCG, and for equity funds, there’s even a ₹1.25 lakh annual exemption.

TAX ON EQUITY MUTUAL FUNDS (2026 RULES)

Equity funds are defined as those investing at least 65% of assets in Indian equities. This includes:

-

Large-cap, mid-cap, small-cap funds

-

ELSS (tax-saving funds)

-

Index funds and ETFs tracking equity indices

Short-Term Capital Gains (STCG) on Equity Funds

| Holding Period | Tax Rate | Surcharge? | Effective Rate |

|---|---|---|---|

| ≤ 12 months | 20% | As applicable | ~20.8% (with cess) |

-

STCG is taxed at a flat 20% (plus cess), regardless of your income slab .

-

No benefit of indexation.

-

No exemption limit—every rupee of STCG is taxable.

Long-Term Capital Gains (LTCG) on Equity Funds

| Holding Period | Tax Rate | Exemption Limit | Effective Rate |

|---|---|---|---|

| > 12 months | 12.5% | ₹1.25 lakh/year | ~13% (with cess) |

Key Rules for LTCG on Equity:

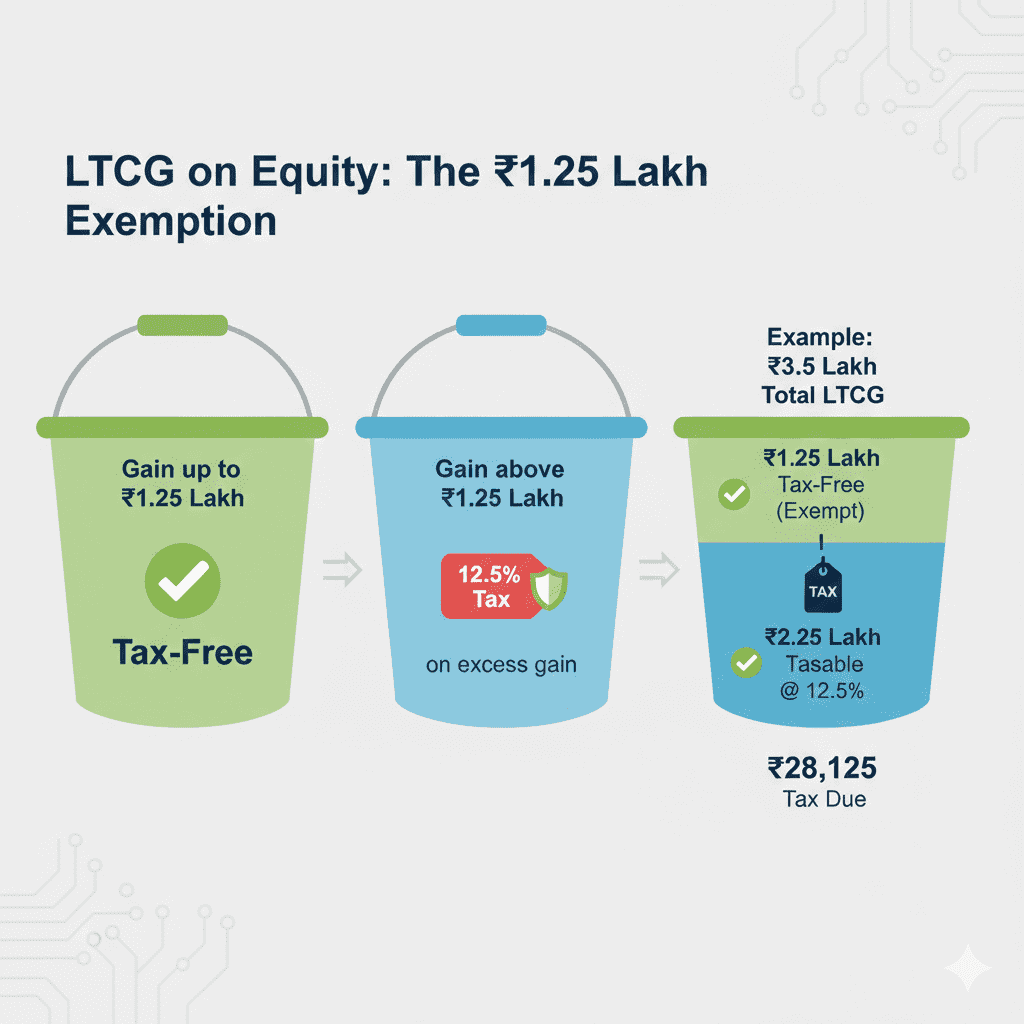

-

Gains up to ₹1.25 lakh in a financial year are tax-free .

-

Only gains above ₹1.25 lakh are taxed at 12.5% .

-

No indexation benefit available .

-

The ₹1.25 lakh limit is per assessee, not per fund.

Example: LTCG Calculation on Equity Funds

Scenario: Vikram redeems equity mutual fund units after 3 years.

| Particulars | Amount |

|---|---|

| Sale Value (Redemption) | ₹8,50,000 |

| Purchase Cost (Original investment) | ₹5,00,000 |

| Total Capital Gain | ₹3,50,000 |

Tax Calculation:

-

Total Gain: ₹3,50,000

-

Less: Exemption (up to ₹1,25,000) | ₹1,25,000

-

Taxable LTCG | ₹2,25,000

-

Tax @ 12.5% | ₹28,125

-

Add: Health & Education Cess @ 4% | ₹1,125

-

Total Tax Payable | ₹29,250

Net Gain After Tax: ₹3,50,000 – ₹29,250 = ₹3,20,750

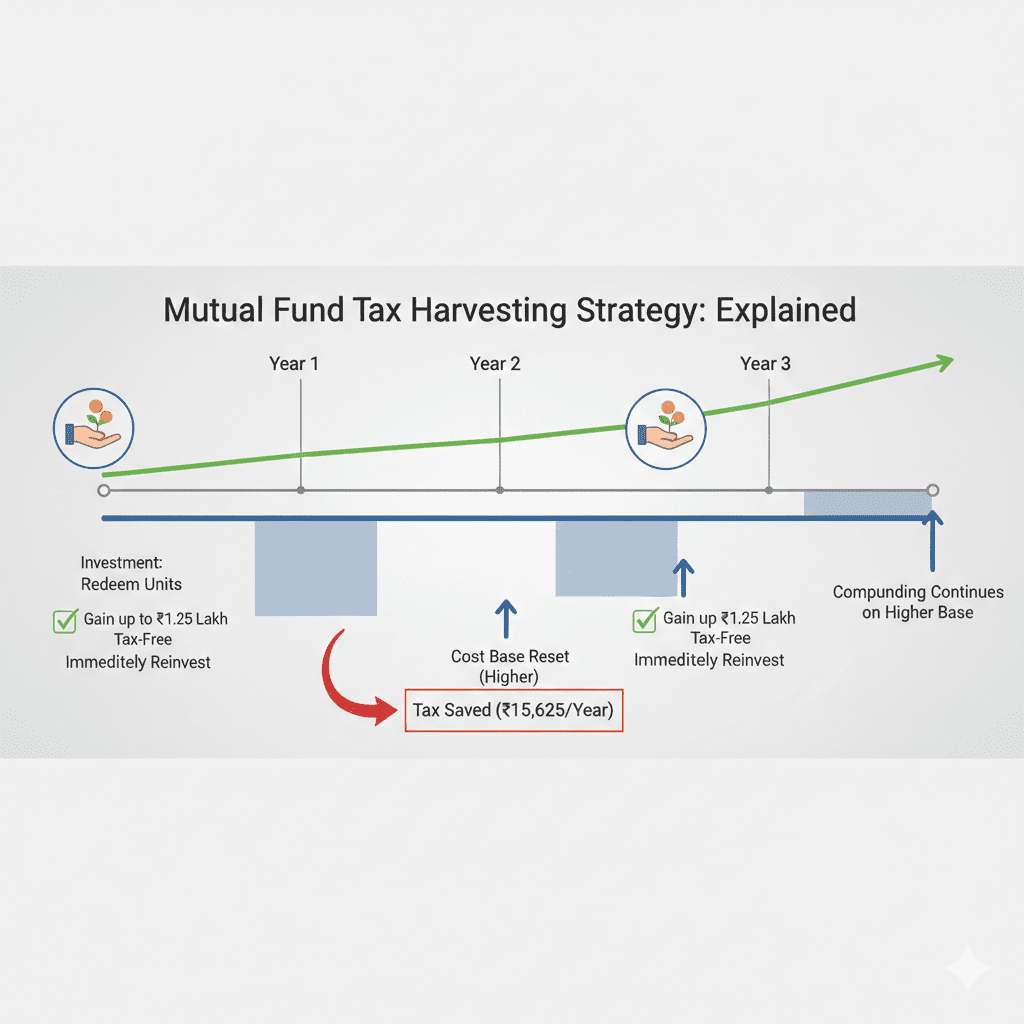

Strategy Tip: Tax Harvesting

Since the exemption is ₹1.25 lakh per year, consider redening units each year to book gains up to this limit, even if you reinvest immediately. This resets your purchase cost and reduces future tax liability .

TAX ON DEBT MUTUAL FUNDS (2026 RULES)

Debt funds invest primarily in fixed-income instruments like bonds, treasury bills, and money market instruments. This includes:

-

Corporate bond funds

-

Gilt funds

-

Liquid funds

-

Ultra-short duration funds

-

Banking & PSU funds

Key Rule Change: Debt Funds Taxed as per Slab Rate (from 2023)

A major change effective April 1, 2023: Capital gains from debt mutual funds are now taxed as per your income slab rate, regardless of holding period, if the fund invests less than 35% in equities .

Exception: Funds investing 35% or more in Indian equities are still taxed like equity funds.

Short-Term vs Long-Term for Debt Funds

| Fund Type | STCG Definition | LTCG Definition |

|---|---|---|

| Debt Funds (<35% equity) | Held ≤ 36 months | Held > 36 months |

| Tax Treatment | Both STCG and LTCG are taxed at income slab rate | Same—added to income |

Example: Debt Fund Redemption

Scenario: Sunita redeems debt fund units after 4 years (so LTCG by definition).

| Particulars | Amount |

|---|---|

| Sale Value | ₹12,00,000 |

| Purchase Cost | ₹8,00,000 |

| Total Capital Gain | ₹4,00,000 |

| Sunita’s Income Slab | 30% |

Tax Calculation:

-

Capital Gain added to Sunita’s income: ₹4,00,000

-

Tax @ 30% (her slab rate): ₹1,20,000

-

Add: Cess @ 4%: ₹4,800

-

Total Tax Payable: ₹1,24,800

Net Gain After Tax: ₹4,00,000 – ₹1,24,800 = ₹2,75,200

Impact on Liquid Funds

Even liquid funds, if held for short periods, now have gains taxed at your slab rate. This makes them less tax-efficient for high-income investors compared to arbitrage funds or FDs (which also have slab-rate taxation).

Strategy for Debt Funds

-

Hold in lower-income years: If you expect lower income in a future year (e.g., sabbatical, retirement), redeem then.

-

Use for short-term goals: For goals under 3 years, debt funds still make sense despite slab-rate tax.

-

Consider arbitrage funds: These are taxed like equity funds (12.5% LTCG after 1 year) but have debt-like risk profiles.

TAX ON HYBRID FUNDS (EQUITY + DEBT)

Hybrid funds invest in both equity and debt. Their tax treatment depends on the equity exposure.

Category 1: Aggressive Hybrid / Balanced Advantage Funds

| Criteria | Tax Treatment |

|---|---|

| Equity exposure ≥ 65% | Taxed like equity funds (12.5% LTCG >1yr, ₹1.25L exemption) |

| Examples | Aggressive hybrid funds, most balanced advantage funds |

Category 2: Conservative Hybrid / Debt-Oriented Hybrid

| Criteria | Tax Treatment |

|---|---|

| Equity exposure < 65% | Taxed like debt funds (slab rate for all gains) |

| Examples | Conservative hybrid funds, monthly income plans (MIPs) |

Category 3: Arbitrage Funds

| Criteria | Tax Treatment |

|---|---|

| Strategy | Exploits price differences in cash and derivative markets |

| Tax Treatment | Taxed like equity funds (12.5% LTCG after 1 year, ₹1.25L exemption) |

| Risk Profile | Very low (market-neutral), but tax-efficient |

Why Arbitrage Funds Are Popular: They offer debt-like returns with equity-like taxation—making them highly tax-efficient for high-income investors.

TAX ON DIVIDENDS (IDCW) FROM MUTUAL FUNDS

The tax treatment of dividends (now called IDCW – Income Distribution cum Capital Withdrawal) has changed significantly.

Pre-2020 vs Post-2020

| Aspect | Before April 2020 | After April 2020 |

|---|---|---|

| Who pays tax? | Fund paid DDT (Dividend Distribution Tax) | Investor pays tax |

| Tax rate | DDT varied by fund type | Added to investor’s income, taxed at slab rate |

| TDS | Not applicable | 10% TDS if dividend > ₹5,000/year |

*Source: Finance Act, 2020 *

Current Dividend Taxation Rules (2026)

| Fund Type | Tax Treatment | TDS Applicable |

|---|---|---|

| All Mutual Funds | Dividend added to investor’s income, taxed at slab rate | 10% if dividend > ₹5,000/year |

Example: Dividend Taxation

Scenario: Rajesh receives ₹60,000 in dividends from his balanced fund. His income slab is 30%.

| Particulars | Amount |

|---|---|

| Dividend Received | ₹60,000 |

| TDS deducted @10% | ₹6,000 |

| Net dividend credited | ₹54,000 |

At Year-End:

-

Dividend added to income: ₹60,000

-

Tax @30% slab: ₹18,000

-

Less: TDS already paid: (₹6,000)

-

Additional tax payable at filing: ₹12,000

Effective Tax Rate: 30% (same as his slab)

Key Points on Dividend Taxation

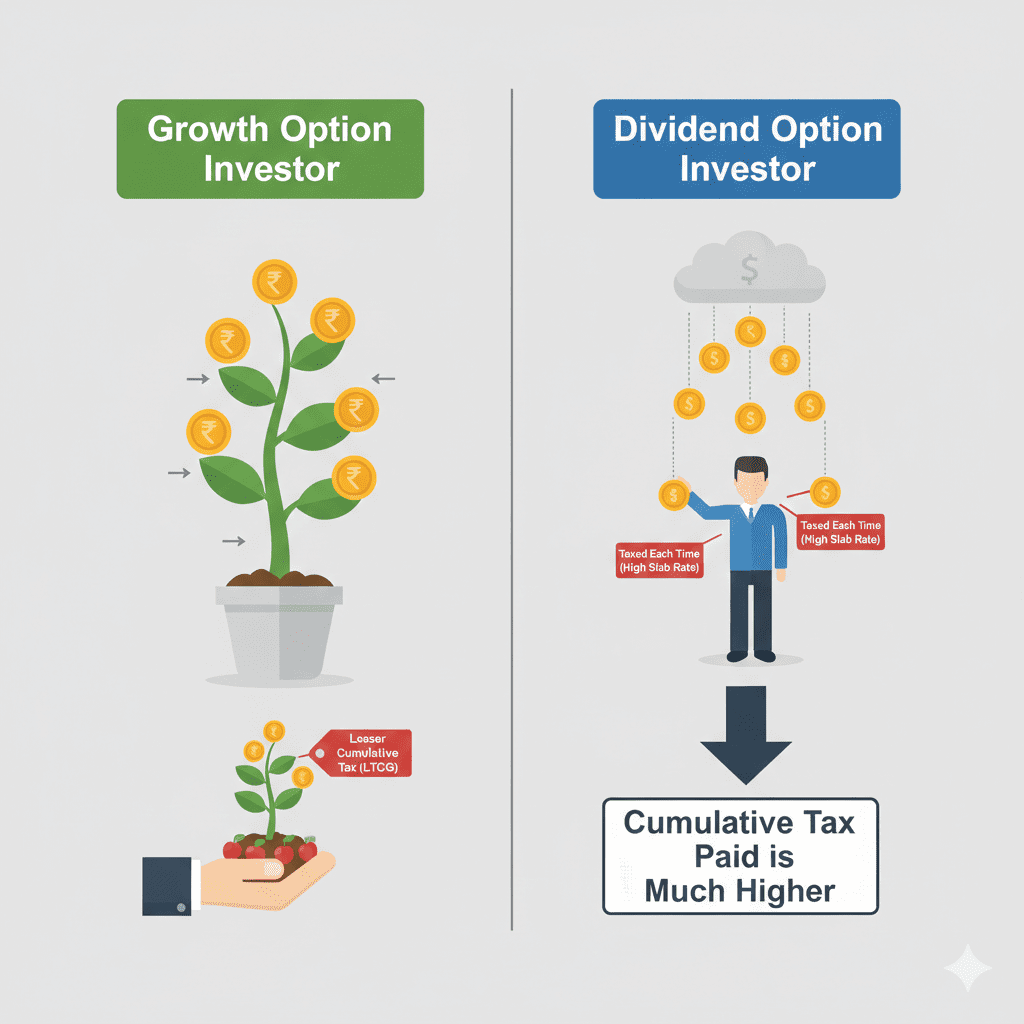

- No more tax-free dividends: All mutual fund dividends are taxable in your hands.

- TDS is not final tax: It’s just an advance; you may owe more or get refund depending on your slab.

- Report correctly: Dividends appear in your AIS; ensure they match your ITR filing.

- Growth option vs Dividend option: For most investors, growth option is more tax-efficient because tax is deferred until redemption, and LTCG rates (12.5%) are often lower than slab rates.

TAX-SAVING WITH ELSS (EQUITY-LINKED SAVINGS SCHEME)

ELSS is the only mutual fund category that offers tax deduction under Section 80C.

ELSS Tax Benefits

| Benefit | Details |

|---|---|

| Deduction under Section 80C | Up to ₹1,50,000 per year |

| Lock-in period | 3 years (shortest among 80C options) |

| Returns | Market-linked (equity) |

| Tax on redemption | Treated as equity fund (LTCG after 3 years) |

Tax on ELSS Redemption

Since ELSS has a mandatory 3-year lock-in, all redemptions are long-term by definition.

| Holding Period | Tax Rate |

|---|---|

| After 3 years (always) | LTCG: 12.5% (over ₹1.25 lakh/year) |

Example: ELSS Investment and Redemption

Scenario: Priya invests ₹1.5 lakh in ELSS and redeems after 5 years when the value is ₹3.2 lakh.

| Particulars | Amount |

|---|---|

| Investment (eligible for 80C deduction) | ₹1,50,000 |

| Redemption Value after 5 years | ₹3,20,000 |

| Capital Gain | ₹1,70,000 |

Tax Calculation:

-

Total Gain: ₹1,70,000

-

Less: LTCG Exemption (₹1.25L) | ₹1,25,000

-

Taxable Gain: ₹45,000

-

Tax @12.5%: ₹5,625

-

Cess @4%: ₹225

-

Total Tax Payable: ₹5,850

Net Gain After Tax: ₹1,70,000 – ₹5,850 = ₹1,64,150

ELSS vs Other 80C Options

| Feature | ELSS | PPF | EPF | Tax-Saving FD |

|---|---|---|---|---|

| Lock-in | 3 years | 15 years | Till retirement | 5 years |

| Returns | Market-linked (10-15% potential) | 7.1% (current) | ~8% | 6-7% |

| Tax on maturity | LTCG >1.25L taxable | Tax-free | Tax-free | Interest taxable |

| Best for | Young investors, long-term | Risk-averse, retirees | Salaried employees | Ultra-conservative |

TAX COMPARISON TABLE: AT A GLANCE

| Fund Type | STCG Definition | STCG Tax Rate | LTCG Definition | LTCG Tax Rate | Dividend Tax |

|---|---|---|---|---|---|

| Equity Funds (≥65% equity) | ≤12 months | 20% | >12 months | 12.5% (over ₹1.25L) | Slab rate |

| Debt Funds (<35% equity) | ≤36 months | Slab rate | >36 months | Slab rate | Slab rate |

| Hybrid (Aggressive) (≥65% equity) | ≤12 months | 20% | >12 months | 12.5% (over ₹1.25L) | Slab rate |

| Hybrid (Conservative) (<65% equity) | ≤36 months | Slab rate | >36 months | Slab rate | Slab rate |

| Arbitrage Funds | ≤12 months | 20% | >12 months | 12.5% (over ₹1.25L) | Slab rate |

| ELSS | N/A (3-yr lock-in) | — | >3 years | 12.5% (over ₹1.25L) | Slab rate |

*Source: Budget 2026, Income Tax Act provisions *

COMMON MISTAKES AND HOW TO AVOID THEM

| Mistake | Why It Hurts | Better Approach |

|---|---|---|

| Ignoring the ₹1.25 lakh LTCG limit | Paying tax when you could have redeemed tax-free | Plan redemptions to stay within limit each year |

| Holding debt funds for short term | STCG taxed at slab rate (30% for high earners) | Use arbitrage funds for debt-like needs |

| Choosing dividend option in high tax bracket | Dividends taxed at slab rate + TDS hassle | Choose growth option; redeem when needed |

| Not reporting dividends in ITR | Notice from IT department (AIS mismatch) | Always report dividend income |

| Forgetting indexation for old debt funds | Pre-2023 debt funds still get indexation benefit | Check purchase date for older investments |

| Selling equity funds just before 1 year | STCG at 20% instead of 12.5% LTCG | Wait a few weeks if possible |

| Not using ELSS for 80C | Missing tax deduction AND equity growth | ELSS beats other 80C options for long term |

| Ignoring tax harvesting | Paying more tax than necessary | Book LTCG up to ₹1.25L each year |

STRATEGIES TO MINIMIZE TAX ON MUTUAL FUNDS

Strategy 1: Tax Harvesting

What: Redeem equity funds each year to book gains up to ₹1.25 lakh (tax-free), and immediately reinvest.

Why It Works:

-

You use the annual exemption limit

-

Your purchase cost resets higher, reducing future gains

-

You remain invested in the market

Example:

-

Fund value: ₹10 lakh, original cost: ₹7 lakh (gain ₹3 lakh)

-

Year 1: Redeem units worth ₹1.25 lakh gain, reinvest

-

New cost base increases, future gains reduce

Strategy 2: Hold for Long Term (Equity)

Equity funds held >1 year get:

-

Lower tax rate (12.5% vs 20%)

-

₹1.25 lakh annual exemption

Strategy 3: Use Arbitrage Funds for Short-Term Surplus

For money you need in 1-3 years:

-

Arbitrage funds offer equity-like taxation

-

LTCG after 1 year at 12.5% (with ₹1.25L exemption)

-

Much better than debt funds taxed at slab rate

Strategy 4: Choose Growth Option Over Dividend

| Option | Tax Impact |

|---|---|

| Growth | Tax deferred until redemption; LTCG at 12.5% |

| Dividend | Taxed annually at slab rate (could be 30%) + TDS |

For most investors, growth option wins unless you need regular cash flow.

Strategy 5: Gift to Lower-Income Family Members

You can gift money to your spouse or adult children (over 18) for them to invest. Capital gains are taxed in their hands—if they’re in a lower slab, overall family tax reduces.

Caution: Clubbing provisions apply if the gift is without consideration and for spouse/minor child—income may be clubbed back.

Strategy 6: Use ELSS for 80C with Equity Exposure

Unlike PPF or tax-saving FDs, ELSS offers:

-

Equity growth potential

-

Shortest lock-in (3 years)

-

LTCG tax treatment

FREQUENTLY ASKED QUESTIONS

Q1: What is the tax on mutual funds in 2026?

It depends on the fund type and holding period:

-

Equity funds: STCG 20%, LTCG 12.5% (over ₹1.25L/year)

-

Debt funds: All gains taxed at your income slab rate

-

Dividends: Added to income, taxed at slab rate

Q2: Is LTCG on mutual funds tax-free?

Partially. For equity funds, LTCG up to ₹1.25 lakh per financial year is tax-free. Gains above this are taxed at 12.5% . For debt funds, no exemption—all gains taxed at slab rate.

Q3: How is dividend from mutual funds taxed?

Dividends (IDCW) are added to your total income and taxed as per your income tax slab rate. A 10% TDS is deducted if the dividend exceeds ₹5,000 in a year, but this is not the final tax .

Q4: Which is better for tax – growth or dividend option?

Growth option is almost always more tax-efficient, especially for those in higher tax brackets. You defer tax until redemption and may benefit from lower LTCG rates (12.5%) instead of slab-rate taxation on dividends each year .

Q5: Are arbitrage funds taxed like equity funds?

Yes. Arbitrage funds are treated as equity funds for taxation because they maintain required equity exposure. LTCG after 1 year: 12.5% with ₹1.25L exemption; STCG: 20% .

Q6: What is tax harvesting in mutual funds?

Tax harvesting means redeeming equity fund units each year to book gains up to the ₹1.25 lakh tax-free limit, and immediately reinvesting. This resets your purchase cost and reduces future taxable gains .

Q7: Is ELSS tax-free at withdrawal?

No. ELSS withdrawals are treated like any equity fund. LTCG after the 3-year lock-in: 12.5% tax on gains above ₹1.25 lakh per year . However, the investment itself gets tax deduction under Section 80C.

Q8: How is STCG on debt funds calculated?

STCG on debt funds (held ≤36 months) is added to your income and taxed at your applicable income slab rate. For example, if you’re in 30% slab, STCG is taxed at 30% (plus cess) .

Q9: Do I need to report mutual fund investments in ITR?

Yes. You must report:

-

All redemptions (capital gains)

-

All dividends received

-

ELSS investments (for 80C deduction)

These appear in your AIS; mismatch can trigger notices.

Q10: Can I offset mutual fund losses against other gains?

Yes.

-

STCL (Short-Term Capital Loss) can offset both STCG and LTCG

-

LTCL (Long-Term Capital Loss) can only offset LTCG

-

Unused losses can be carried forward for 8 years

ACTIONABLE CHECKLIST: PLAN YOUR MUTUAL FUND TAXES

Before Investing

-

Choose growth option over dividend (unless you need regular cash flow)

-

For short-term needs (<3 years), consider arbitrage funds (equity taxation)

-

For tax-saving under 80C, prefer ELSS over other options

-

Maintain separate folios for different goals (easier tracking)

During the Year

-

Track all redemptions and their holding periods

-

Monitor LTCG from equity funds—aim to stay within ₹1.25L if possible

-

Record all dividends received (even if small)

-

Note down any capital losses (can be carried forward)

At Year-End (Before March 31)

-

Consider tax harvesting—redeem equity funds up to ₹1.25L gain, reinvest

-

Review debt fund holdings—if in high slab, consider switching to arbitrage

-

Check ELSS investments—maximize 80C deduction if not done

At Tax Filing Time

-

Download AIS (Annual Information Statement) from income tax portal

-

Verify all redemptions and dividends match your records

-

Report capital gains in the correct schedule (CG or Schedule 112A)

-

Claim 80C deduction for ELSS investments

-

File on time—avoid late fees

SUCCESS STORY: HOW A SMART INVESTOR SAVED ₹1.2 LAKH IN TAXES

Profile: Vikram, 42, IT professional in Pune

Annual Income: ₹28 lakh (30% tax slab)

Mutual Fund Portfolio: ₹45 lakh across equity and debt funds

His Tax-Smart Moves

| Strategy | What He Did | Tax Saved |

|---|---|---|

| Tax Harvesting | Booked ₹1.2L LTCG each year from equity funds, reinvested | ₹15,000/year (over 3 years = ₹45,000) |

| Arbitrage for Short-term | Moved 6-month surplus from liquid fund to arbitrage fund | STCG would be 30% in debt; arbitrage gave 12.5% LTCG |

| Growth Option | Switched all dividend options to growth | Avoided 30% tax on dividends annually |

| ELSS for 80C | Invested ₹1.5L in ELSS instead of PPF | Higher returns + LTCG treatment |

| Loss Harvesting | Sold underperforming stock with ₹80K loss, offset against gains | ₹24,000 tax saved |

Total Tax Saved Over 3 Years: ₹1,27,000

“I used to think tax on investments was something that just happens. Now I plan for it—and save over a lakh every few years just by being smart about when and how I redeem.” – Vikram

CONCLUSION: MASTER YOUR MUTUAL FUND TAXES

Mutual fund taxation doesn’t have to be complicated or scary. The rules are clear, and with a little planning, you can legally minimize your tax outgo while letting your investments grow.

Key Takeaways

- Equity funds: LTCG 12.5% (over ₹1.25L), STCG 20%

- Debt funds: All gains taxed at your slab rate (post-2023)

- Dividends: Taxed at slab rate + 10% TDS

- ELSS: 80C deduction + equity tax treatment

- Arbitrage funds: Equity taxation with low risk

- Growth option beats dividend option for most investors

- Tax harvesting can save significant taxes annually

Your Next Steps

-

Review your mutual fund portfolio today—check holding periods and gain amounts

-

Use India Tax Tools’ Mutual Fund Tax Calculator to estimate tax on your redemptions

-

Plan redemptions to stay within ₹1.25L LTCG limit where possible

-

Consider arbitrage funds for short-term surplus

-

Consult your CA for personalized advice, especially for large redemptions

Remember: Paying tax on your gains means your investments have grown. But with smart planning, you can keep more of that growth for yourself.

“In mutual funds, what matters isn’t just what you earn—it’s what you keep after tax. Plan your redemptions, use the ₹1.25 lakh exemption, and let tax harvesting work for you.”

Disclaimer: This article is for informational and educational purposes only and does not constitute investment or tax advice. Tax laws are subject to change. Please consult your financial advisor or Chartered Accountant before making investment decisions. The information provided is based on Budget 2026 announcements and current tax provisions as of February 2026.