Tax on Part-Time Income 2026: Rules & Filing Guide

Then there’s Vikram, a college student who does freelance graphic design projects alongside his studies, earning ₹80,000 a year. He’s never filed taxes and wonders if he needs to.

If you earn from a part-time job, freelance work, side hustle, or any additional income beyond your primary salary, you’re not alone. According to a 2025 survey, over 40% of urban Indians have some form of secondary income . Yet, most are confused about the tax implications.

The good news? Part-time income is taxable, but the rules are clear—and you can plan to minimize your tax burden legally.

In this comprehensive 2026 guide, you’ll discover:

-

How part-time income is classified (salary vs. freelance vs. other sources)

-

TDS on part-time earnings – when it’s deducted and when it’s not

-

Exemptions available for certain types of part-time work

-

Clubbing rules – when your income is added to someone else’s

-

Deductions you can claim (even for part-time work expenses)

-

How to file ITR with multiple income sources

-

Common mistakes that trigger notices

-

Real examples with step-by-step calculations

Let’s demystify tax on part-time income—so you can earn extra without tax anxiety.

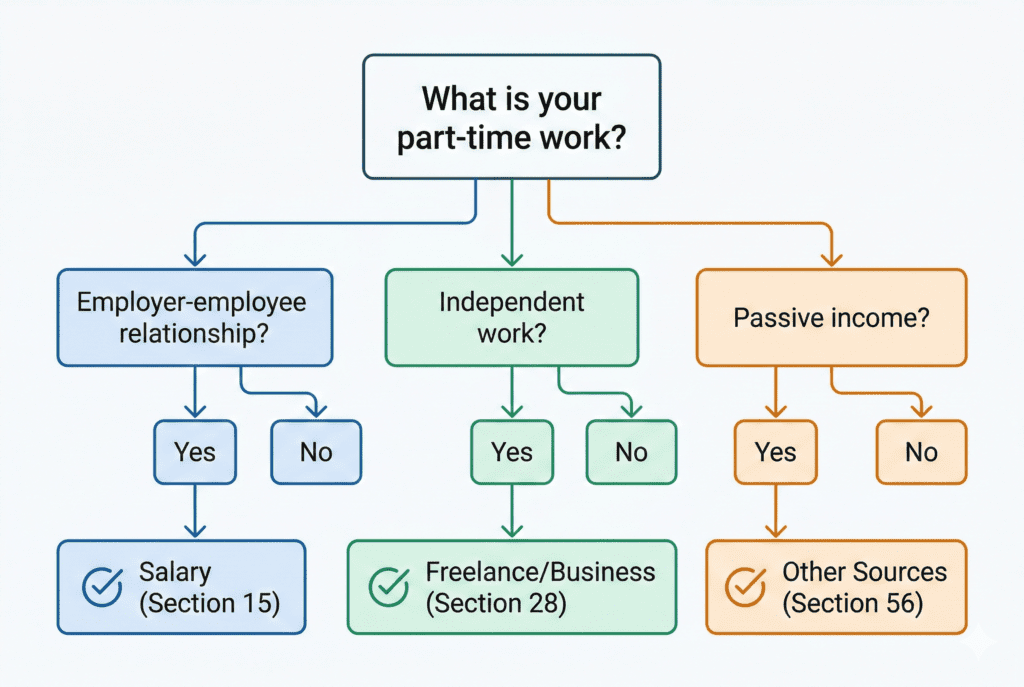

HOW PART-TIME INCOME IS CLASSIFIED FOR TAX PURPOSES

The tax treatment of your part-time income depends on how it is classified under the Income Tax Act. There are three possible heads:

Classification Table

| Nature of Part-Time Work | Head of Income | TDS Section | TDS Rate (2026) |

|---|---|---|---|

| Part-time job (e.g., teaching, coaching, hourly work with employer-employee relationship) | Salary (Section 15) | 192 | As per slab |

| Freelance/Consultancy (e.g., graphic design, content writing, consulting) | Business/Profession (Section 28) | 194J | 10% |

| One-off assignments (e.g., guest lecture, project-based work) | Other Sources (Section 56) | 194J or 194C | 10% or 1-2% |

| Passive income (e.g., rent from a property, interest on savings) | Other Sources | 194A/194I | 10% on interest, 10% on rent |

| Commission-based work | Business/Profession | 194H | 5% |

Key Distinction: Salary vs. Freelance

| Feature | Salary | Freelance/Business |

|---|---|---|

| Employer-employee relationship | Yes (control over work, fixed hours) | No (you control how work is done) |

| TDS deduction | By employer under Section 192 | By payer under Section 194J/194C |

| Form issued | Form 16 | Form 16A or TDS certificate |

| Expenses allowed | Limited (standard deduction, HRA) | All business expenses |

| Presumptive taxation | No | Yes (Section 44ADA for professionals) |

Example: Priya’s Part-Time Tutoring

| Aspect | Analysis |

|---|---|

| Nature | Priya tutors students independently, sets her own hours, no employer control |

| Classification | Freelance income (Business/Profession) |

| TDS | If payment from each student > ₹30,000, student may deduct 10% TDS under 194J |

| Expenses | Can claim books, travel, internet, etc. |

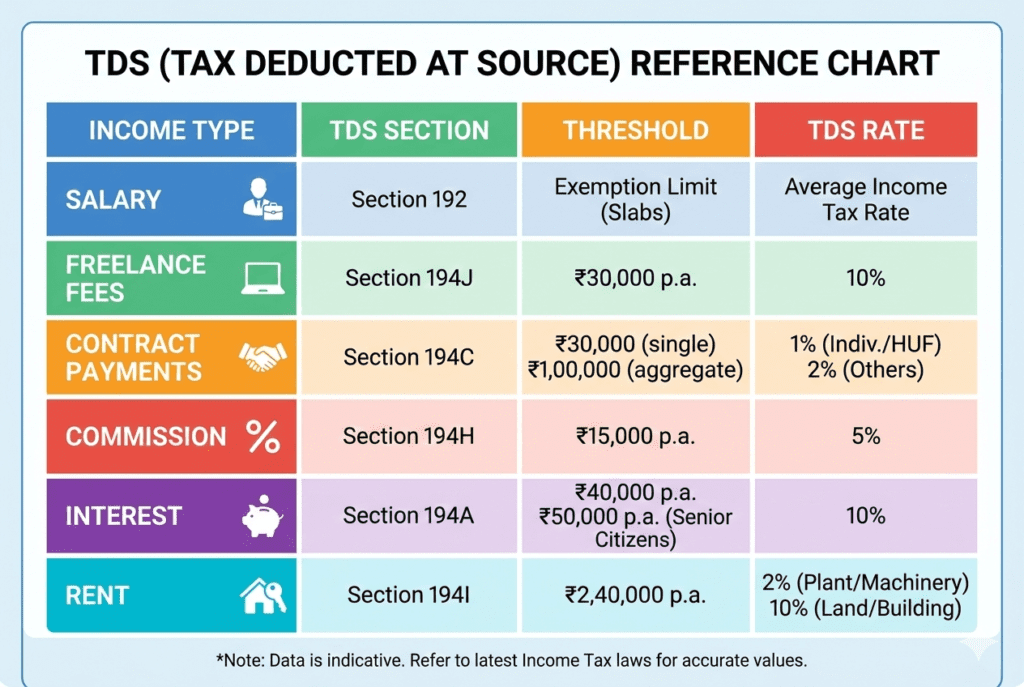

TDS ON PART-TIME INCOME

When is TDS Deducted on Part-Time Income?

| Income Type | TDS Threshold (per year) | TDS Rate |

|---|---|---|

| Salary from part-time job | Basic exemption limit (₹2.5L/₹3L/₹5L depending on regime) | As per slab |

| Freelance/Professional fees | ₹30,000 (per payment) | 10% (194J) |

| Contract payments | ₹30,000 (per invoice) or ₹1,00,000 (aggregate) | 1-2% (194C) |

| Commission/brokerage | ₹15,000 | 5% (194H) |

| Interest on savings | ₹40,000 (₹50,000 for senior citizens) | 10% (194A) |

| Rent | ₹2,40,000 | 10% (194I) |

What If TDS is Not Deducted?

| Scenario | What You Should Do |

|---|---|

| Payer was supposed to deduct TDS but didn’t | You must still pay tax (advance tax/self-assessment) |

| Payer is an individual not liable for TDS | No TDS deducted; you pay tax directly |

| Each payment is below threshold but aggregate is high | No TDS, but you must include all income |

How to Claim TDS Credit

| Step | Action |

|---|---|

| 1 | Ensure payer has your correct PAN |

| 2 | Check Form 26AS after TDS is deposited |

| 3 | If TDS not reflecting, follow up with payer |

| 4 | Claim credit while filing ITR (auto-populates) |

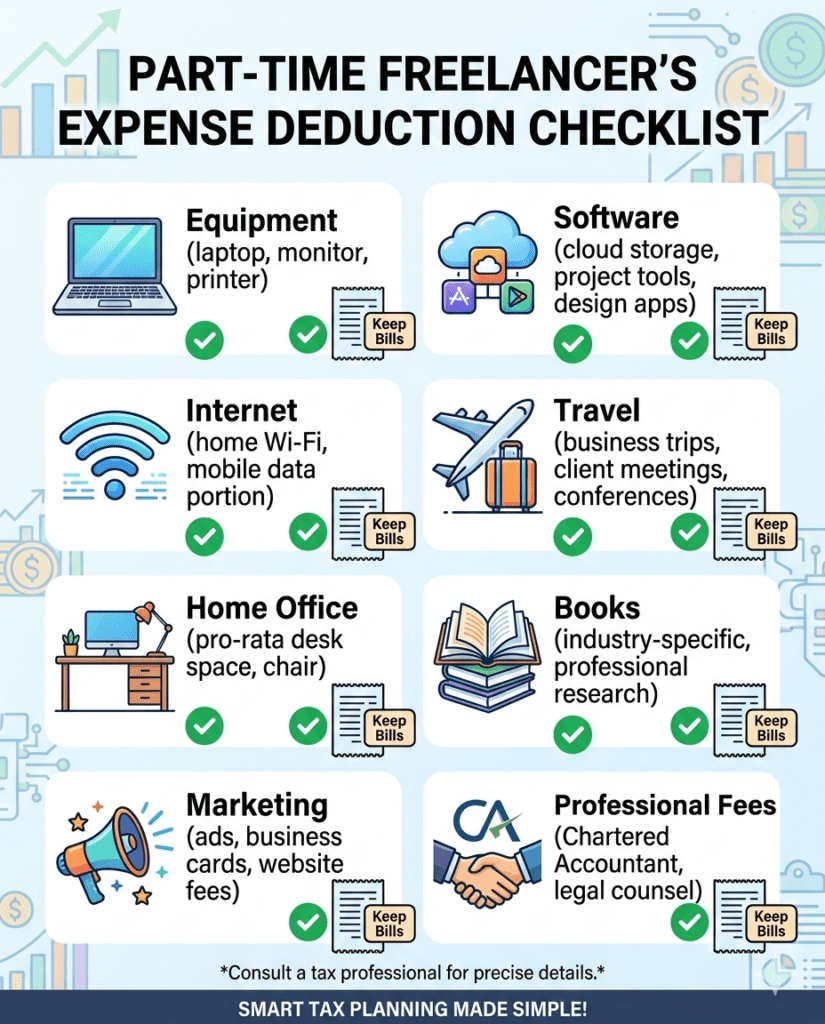

EXEMPTIONS AND DEDUCTIONS FOR PART-TIME INCOME

For Part-Time Salary (if classified as salary)

| Deduction | Maximum | Conditions |

|---|---|---|

| Standard Deduction | ₹75,000 (New Regime) / ₹50,000 (Old Regime) | Automatic for salaried |

| HRA (if applicable) | Actual HRA, rent paid minus 10% salary | Need rent receipts |

| Professional Tax | Actual paid | Varies by state |

For Freelance/Business Income

| Deduction | Examples | Documentation |

|---|---|---|

| Direct expenses | Materials, supplies, books | Invoices, bills |

| Equipment | Laptop, phone, camera | Depreciation (if capital) |

| Software/subscriptions | Design tools, cloud storage | Receipts |

| Internet/phone | Proportionate to business use | Bills |

| Travel | Client meetings, project-related | Tickets, bills |

| Home office | Portion of rent, electricity | Calculation basis |

| Professional fees | CA, legal expenses | Invoices |

For Income from Other Sources

| Deduction | Allowed For |

|---|---|

| Interest on savings | No deduction (fully taxable) |

| Rental income | Municipal taxes, 30% standard deduction, interest on loan |

| Family pension | Standard deduction of ₹15,000 or 33⅓% |

Section 80C, 80D, etc.

These deductions are available regardless of income source. You can claim:

-

80C: Up to ₹1.5 lakh (PPF, ELSS, LIC, etc.)

-

80D: Health insurance premium (up to ₹25,000/₹50,000)

-

80CCD(1B): NPS additional ₹50,000

-

80E: Education loan interest

CLUBBING OF INCOME – WHEN PART-TIME INCOME IS ADDED TO SOMEONE ELSE

Under certain circumstances, your part-time income may be clubbed (added) to another person’s income for tax purposes.

Clubbing Rules (Section 64)

| Scenario | Whose Income It’s Added To |

|---|---|

| Income of spouse from business where you have substantial interest | Your income |

| Income of spouse from assets transferred directly or indirectly | Your income |

| Income of minor child (except from manual work or special talent) | Parent with higher income |

| Income from assets transferred to son’s wife | Your income |

Example: Minor Child’s Part-Time Income

Scenario: Vikram’s 16-year-old daughter earns ₹60,000 from a part-time modeling assignment.

| Rule | Application |

|---|---|

| Income of minor child | Clubbed to parent with higher income |

| Exception | If income from own skill/talent, not clubbed (but minor’s income still taxed separately) |

| Result | Daughter files separate return; no clubbing |

Important Exceptions

| Income Type | Not Clubbed |

|---|---|

| Minor’s income from manual work | Yes (separate) |

| Minor’s income from own talent/skill | Yes (separate) |

| Spouse’s income from own professional skills | No clubbing |

| Income from assets received as inheritance | No clubbing |

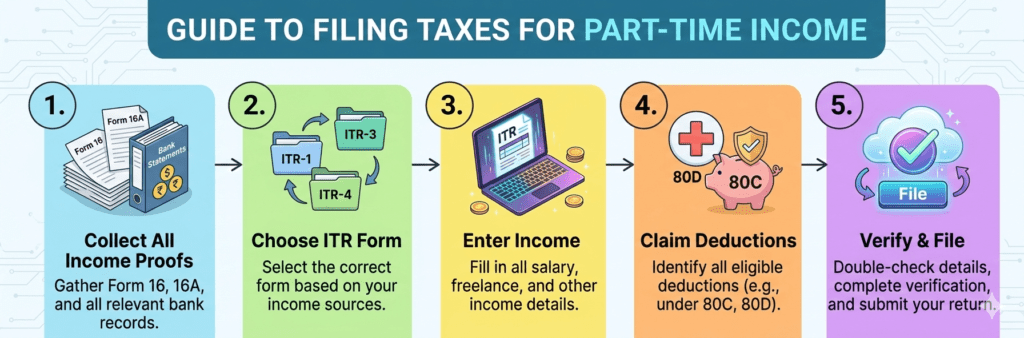

HOW TO FILE ITR WITH PART-TIME INCOME

Step 1: Determine Your Total Income

Add income from all sources:

-

Salary from full-time job

-

Part-time job/freelance income

-

Interest from savings, FD

-

Any other income

Step 2: Choose Correct ITR Form

| Income Sources | ITR Form |

|---|---|

| Salary + Part-time salary + Other Sources | ITR-1 (if total income ≤ ₹50 lakh) |

| Salary + Freelance/Business income | ITR-3 |

| Salary + Presumptive business (44ADA) | ITR-4 |

| Only freelance/business income | ITR-3 or ITR-4 |

Step 3: Gather Documents

| Document | Purpose |

|---|---|

| Form 16 (from full-time employer) | Salary details, TDS |

| Form 16A/16B/16C | TDS on part-time income |

| Bank statements | Interest income |

| Invoices raised | Freelance income proof |

| Expense bills | To claim deductions |

| Form 26AS | Verify TDS credits |

Step 4: Calculate Tax

Use India Tax Tools’ Advanced Tax Calculator to:

-

Combine all income

-

Choose between old and new regime

-

Apply deductions

-

Compute tax payable/refund

Step 5: File Online

| Step | Action |

|---|---|

| 1 | Login to income tax portal (https://www.incometax.gov.in) |

| 2 | Select appropriate ITR form |

| 3 | Enter income from all sources |

| 4 | Claim deductions (80C, 80D, etc.) |

| 5 | Verify pre-filled TDS from Form 26AS |

| 6 | Submit and e-verify |

REAL EXAMPLES: TAX ON PART-TIME INCOME

Example 1: Full-Time Job + Part-Time Freelance

Profile: Priya (from introduction)

-

Full-time salary: ₹12,00,000

-

Part-time tutoring (freelance): ₹1,20,000

-

Expenses related to tutoring: ₹15,000 (books, travel)

-

80C investments: ₹1,20,000

-

80D health insurance: ₹18,000

Step 1: Calculate Income

| Source | Amount |

|---|---|

| Salary | ₹12,00,000 |

| Freelance income (gross) | ₹1,20,000 |

| Less: Expenses | (₹15,000) |

| Net freelance income | ₹1,05,000 |

| Total Income | ₹13,05,000 |

Step 2: Choose Regime

| Regime | Taxable Income | Tax Payable |

|---|---|---|

| New Regime | ₹13,05,000 – ₹75,000 = ₹12,30,000 | ₹1,51,100 |

| Old Regime (after 80C, 80D) | ₹13,05,000 – ₹1,20,000 – ₹18,000 – std ded ₹50,000 = ₹11,17,000 | ₹1,68,200 |

Verdict: New Regime saves ₹17,100.

Example 2: Student with Part-Time Freelance

Profile: Vikram, college student

-

Part-time graphic design income: ₹80,000

-

Expenses (software, laptop): ₹25,000

-

No other income

| Calculation | Amount |

|---|---|

| Gross income | ₹80,000 |

| Less: Expenses | (₹25,000) |

| Net income | ₹55,000 |

| Tax payable | Nil (below basic exemption) |

Should he file ITR? Yes, recommended for:

-

Future loan eligibility

-

Visa applications

-

Proof of income

-

Carry forward losses (if any)

Example 3: Part-Time Job (Salary) + Full-Time Job

Profile: Rahul

-

Full-time salary: ₹8,00,000

-

Part-time teaching at coaching center (salary): ₹1,50,000

-

TDS on part-time: ₹15,000 deducted

| Calculation | Amount |

|---|---|

| Total salary | ₹9,50,000 |

| Standard deduction | ₹75,000 (New Regime) |

| Taxable | ₹8,75,000 |

| Tax payable | ₹67,600 |

| Less: TDS already deducted | (₹15,000) |

| Tax to pay | ₹52,600 |

COMMON MISTAKES TO AVOID

| Mistake | Consequence | How to Avoid |

|---|---|---|

| Not reporting part-time income | Notice from IT department, penalty | Include all income in ITR |

| Misclassifying income | Wrong TDS, wrong deductions | Understand salary vs freelance |

| Not claiming expenses | Pay more tax than needed | Track and claim all eligible expenses |

| Ignoring TDS on part-time | TDS credit lost | Ensure payer has your PAN, check 26AS |

| Not filing ITR at all | Penalty under 234F | File even if income below threshold |

| Choosing wrong regime | Higher tax liability | Calculate both before deciding |

| Not reconciling Form 26AS | Mismatch notices | Download and verify before filing |

| Missing advance tax | Interest under 234B/234C | Pay if tax liability > ₹10,000 |

FREQUENTLY ASKED QUESTIONS

Q1: Do I have to pay tax on part-time income?

Yes, part-time income is taxable and must be included in your total income. You pay tax based on your total income slab .

Q2: Will my full-time employer know about my part-time income?

No. Your employer only knows about the salary they pay you. Part-time income is reported directly in your ITR and is confidential.

Q3: What is the TDS rate on freelance part-time work?

TDS on professional fees under Section 194J is 10% if the payment exceeds ₹30,000 per transaction .

Q4: Can I claim expenses against part-time freelance income?

Yes. You can claim all legitimate business expenses incurred for earning that income (equipment, software, travel, internet, etc.) .

Q5: I’m a student with part-time income. Do I need to file ITR?

If your total income exceeds the basic exemption limit (₹2.5L/₹3L/₹4L depending on regime), filing is mandatory. Even if below threshold, filing is recommended for loan/visa purposes.

Q6: Which ITR form should I use for salary + freelance?

You need ITR-3 (if regular freelance) or ITR-4 (if opting for presumptive taxation under Section 44ADA) .

Q7: What if no TDS was deducted on my part-time income?

If TDS was not deducted (e.g., payer is individual not liable), you must still include the income and pay tax via advance tax/self-assessment tax .

Q8: Can I claim HRA on part-time salary?

HRA exemption is available only if you receive HRA as part of your salary. For part-time jobs that pay HRA, you can claim it proportionately.

Q9: Is part-time income from abroad taxable in India?

Yes, if you are a resident Indian, your global income (including part-time income from abroad) is taxable in India. DTAA benefits may apply to avoid double taxation.

Q10: What is the penalty for not disclosing part-time income?

Non-disclosure can lead to:

-

Notice under Section 142(1)

-

Penalty up to 100-300% of tax evaded

-

Prosecution in severe cases

Always declare all income.

ACTIONABLE CHECKLIST: PART-TIME INCOME TAX PLANNING

Throughout the Year

-

Maintain separate records for part-time income

-

Keep all invoices and payment proofs

-

Track all business expenses (with bills)

-

Ensure payers have your correct PAN

-

Check Form 26AS quarterly for TDS credits

At Year-End (January-March)

-

Compile all income from part-time sources

-

Calculate total expenses (if freelance)

-

Estimate total tax liability

-

Pay any remaining advance tax by 15th March

During Filing Season (July-August)

-

Collect Form 16 (full-time job)

-

Download Form 26AS and AIS

-

Choose correct ITR form (ITR-1, ITR-3, or ITR-4)

-

Enter all income accurately

-

Claim eligible deductions (80C, 80D, expenses)

-

Compare old vs new regime using India Tax Tools’ Advanced Tax Calculator

-

File ITR online

-

E-verify immediately

Tools to Help

-

Advanced Tax Calculator – Compute tax with multiple incomes

-

GST Calculator – If part-time work involves GST

-

Invoice Generator – Create professional invoices

-

TDS Calculator – Understand TDS on your income

-

80C Calculator – Plan investments

-

Due Date Tracker – Never miss advance tax or filing

SUCCESS STORY: HOW A SIDE HUSTLER SAVED ₹45,000

Profile: Anjali, 32, full-time marketing manager in Mumbai

Part-time: Freelance content writing (₹3.2 lakh/year)

Before Optimization

| Item | Amount |

|---|---|

| Part-time income declared | ₹3,20,000 |

| Expenses claimed | ₹0 |

| Tax paid (on additional income) | ~₹65,000 |

After Smart Planning

| Strategy | What She Did | Tax Saved |

|---|---|---|

| Expense tracking | Claimed laptop depreciation (₹15,000), software (₹8,000), internet (₹6,000), home office (₹24,000) | Reduced taxable income by ₹53,000 |

| Section 44ADA | Opted for presumptive (50% profit) which was lower than actual after expenses | Actually used regular scheme (expenses >50%) |

| 80C/80D | Maximized 80C (₹1.5L) and 80D (₹25,000) | ₹52,500 tax saved |

| Regime choice | New regime was better overall | ₹12,000 saved |

Total tax saved: ₹45,000 (on part-time + full-time combined)

“I used to just add my freelance income to my salary and pay tax on the full amount. Tracking expenses alone saved me over ₹15,000. Every freelancer should do this.” – Anjali

CONCLUSION: TAX ON PART-TIME INCOME MADE SIMPLE

Earning extra income through part-time work is rewarding—but only if you don’t give away a large chunk to taxes unnecessarily. The key takeaways:

- Classify correctly – salary, freelance, or other sources

- Understand TDS – know when it’s deducted and claim credit

- Claim all deductions – expenses (if freelance), 80C, 80D

- Choose the right regime – calculate both options

- File correctly – use the right ITR form, include all income

Your Next Steps

-

Calculate your total income (full-time + part-time) using India Tax Tools’ Advanced Tax Calculator

-

Decide on regime – which saves you more?

-

Track expenses – if freelance, start today

-

Plan 80C investments – before 31st March

-

File on time – avoid penalties

Remember: Part-time income is a sign of your enterprise. Don’t let tax confusion diminish its value. With smart planning, you can keep more of what you earn.

“Your side hustle deserves smart tax planning. Classify your income right, claim every expense, and never let TDS go unclaimed. Your extra effort should pay off—in your pocket, not just in taxes.”

Disclaimer: This article is for informational and educational purposes only. Tax laws, rates, and thresholds are subject to change based on government notifications. Please consult a qualified Chartered Accountant for advice tailored to your specific situation. The information provided is based on Budget 2026 announcements and current provisions as of February 2026. India Tax Tools calculators are free tools for estimation and should not be considered as professional tax advice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment