Tax Planning for Beginners: A Step-by-Step Guide for First-Time Taxpayers

Meet Priya, 24, who just landed her first job as a software engineer in Bangalore. Her offer letter says ₹8.5 lakh per annum. She’s excited but confused—her friends mention “tax planning,” “80C,” and “regime choice.” She has no idea where to start. Then there’s Rahul, 28, a freelance graphic designer who crossed ₹7 lakh income this year and suddenly realizes he needs to file taxes.

If you’re earning for the first time—whether through a job, freelancing, or business—tax planning can feel overwhelming. But here’s the truth: tax planning isn’t about hiding money or doing complex calculations. It’s simply about understanding the rules and making smart choices to keep more of what you earn.

A 2025 survey found that over 60% of first-time taxpayers pay more tax than necessary simply because they don’t know about available deductions . The good news? With a little knowledge, you can save thousands.

In this beginner-friendly guide, you’ll discover:

-

Tax basics: What is income, what is taxable, and how tax is calculated

-

Old vs New Tax Regime: Which one saves you more money (with examples)

-

Section 80C: The most important deduction (and how to use it)

-

Other deductions: 80D, 80CCD, HRA, and more

-

Step-by-step tax planning for your first job

-

Common mistakes beginners make

-

Free tools to calculate your tax

Let’s turn tax confusion into tax savings.

TAX BASICS: WHAT EVERY BEGINNER MUST KNOW

Before planning, understand the fundamentals.

What is Income Tax?

Income tax is a percentage of your earnings that you pay to the government. It funds public services—roads, schools, healthcare, defense. In India, income tax is governed by the Income Tax Act, 1961.

Who Needs to Pay Tax?

| Income Level (FY 2025-26) | Tax Liability |

|---|---|

| Up to ₹4,00,000 (New Regime) | Nil (rebate under Section 87A) |

| ₹4,00,001 – ₹12,00,000 | 5% to 15% (slab rates) |

| Above ₹12,00,000 | 15% to 30% |

For Old Regime, basic exemption is ₹2,50,000 (₹3,00,000 for senior citizens)

Types of Income

Your total income is classified into five heads:

| Head of Income | Examples |

|---|---|

| Salary | Basic, HRA, allowances, pension |

| House Property | Rental income from property |

| Business/Profession | Freelancing, trading, consultancy |

| Capital Gains | Profit from sale of shares, property, gold |

| Other Sources | Interest (savings account, FD), lottery winnings |

How Tax is Calculated (Simple Formula)

Gross Total Income (all sources) (-) Deductions (Section 80C, 80D, etc.) = Taxable Income Apply Slab Rates = Income Tax (+) Cess @ 4% = Total Tax Payable

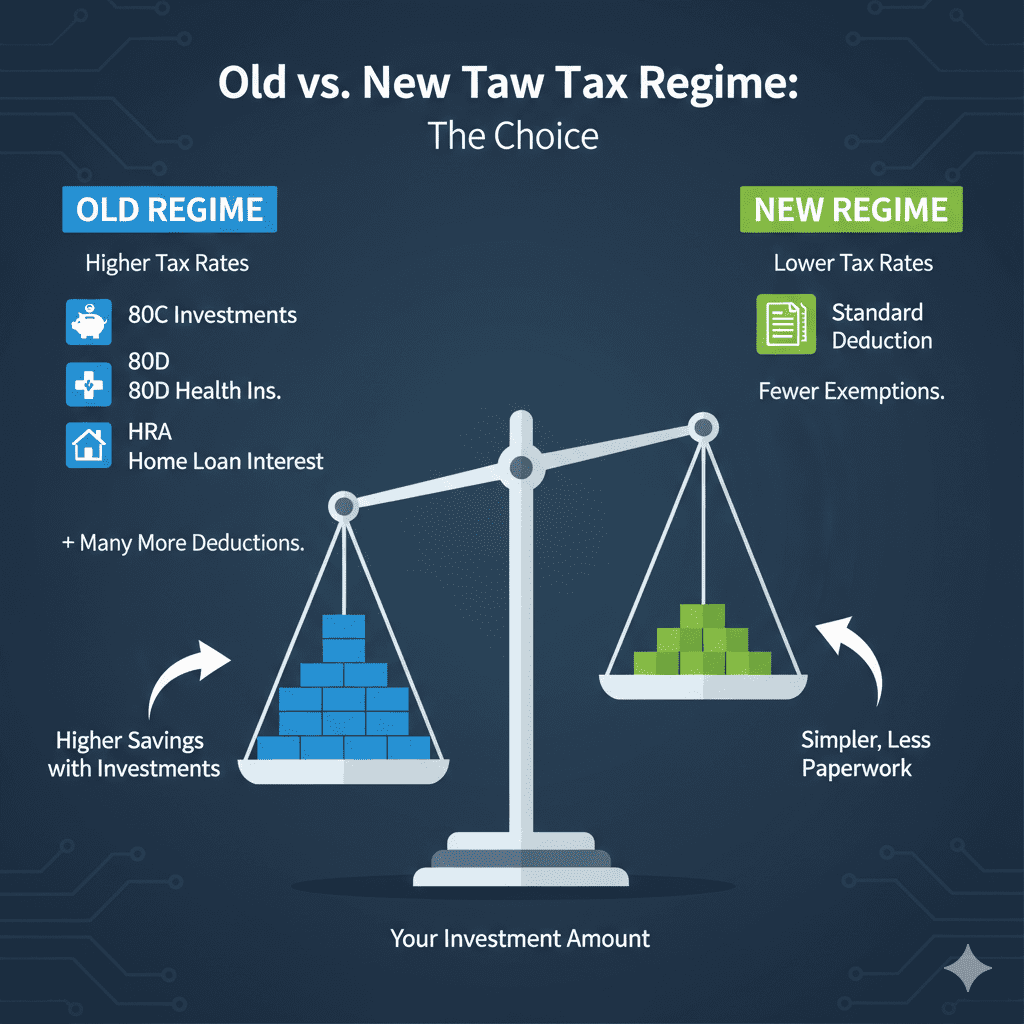

OLD VS NEW TAX REGIME: WHICH ONE SHOULD YOU CHOOSE?

The most important decision for first-time taxpayers is choosing between the Old Tax Regime and the New Tax Regime.

New Tax Regime (Default from FY 2023-24)

| Income Slab (₹) | Tax Rate |

|---|---|

| Up to 4,00,000 | Nil |

| 4,00,001 – 8,00,000 | 5% |

| 8,00,001 – 12,00,000 | 10% |

| 12,00,001 – 16,00,000 | 15% |

| 16,00,001 – 20,00,000 | 20% |

| 20,00,001 – 24,00,000 | 25% |

| Above 24,00,000 | 30% |

Key Features:

-

Lower tax rates but no deductions/exemptions (except standard deduction ₹75,000 for salaried)

-

Ideal if you have few investments (no 80C, no HRA, no home loan)

Old Tax Regime (Optional)

| Income Slab (₹) | Tax Rate |

|---|---|

| Up to 2,50,000 | Nil |

| 2,50,001 – 5,00,000 | 5% |

| 5,00,001 – 10,00,000 | 20% |

| Above 10,00,000 | 30% |

Key Features:

-

Higher tax rates but many deductions available (80C, 80D, HRA, home loan interest, etc.)

-

Ideal if you invest significantly (PPF, ELSS, life insurance, etc.)

Comparison Example: Priya’s First Salary

Scenario: Priya earns ₹8.5 lakh annually. No major investments yet. Let’s compare both regimes.

| Regime | Calculation | Tax Payable |

|---|---|---|

| New Regime | ₹8,50,000 – ₹75,000 (std deduction) = ₹7,75,000 taxable | ₹33,150 (including cess) |

| Old Regime | ₹8,50,000 – ₹50,000 (std deduction) = ₹8,00,000 taxable | ₹62,400 (including cess) |

Verdict: New Regime saves ₹29,250 for Priya.

Decision Tree for Beginners

| Your Situation | Likely Better Regime |

|---|---|

| No investments (just starting) | New Regime |

| Investing in PPF/ELSS/LIC (>₹1.5L) | Old Regime (after calculation) |

| Paying HRA (rent > ₹1L/year) | Old Regime (claim HRA) |

| Home loan (interest > ₹1.5L) | Old Regime |

| Income < ₹7.5 lakh | New Regime (often zero tax) |

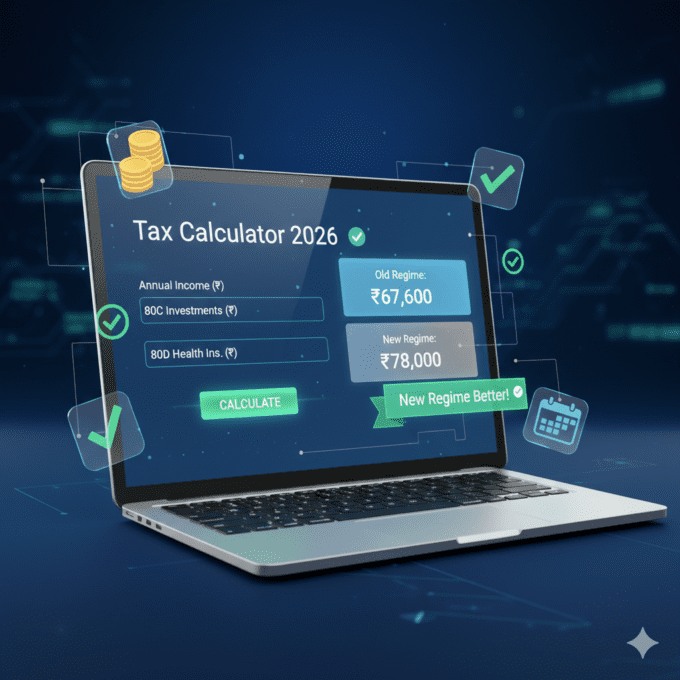

| Unsure | Calculate both using India Tax Tools’ Advanced Tax Calculator |

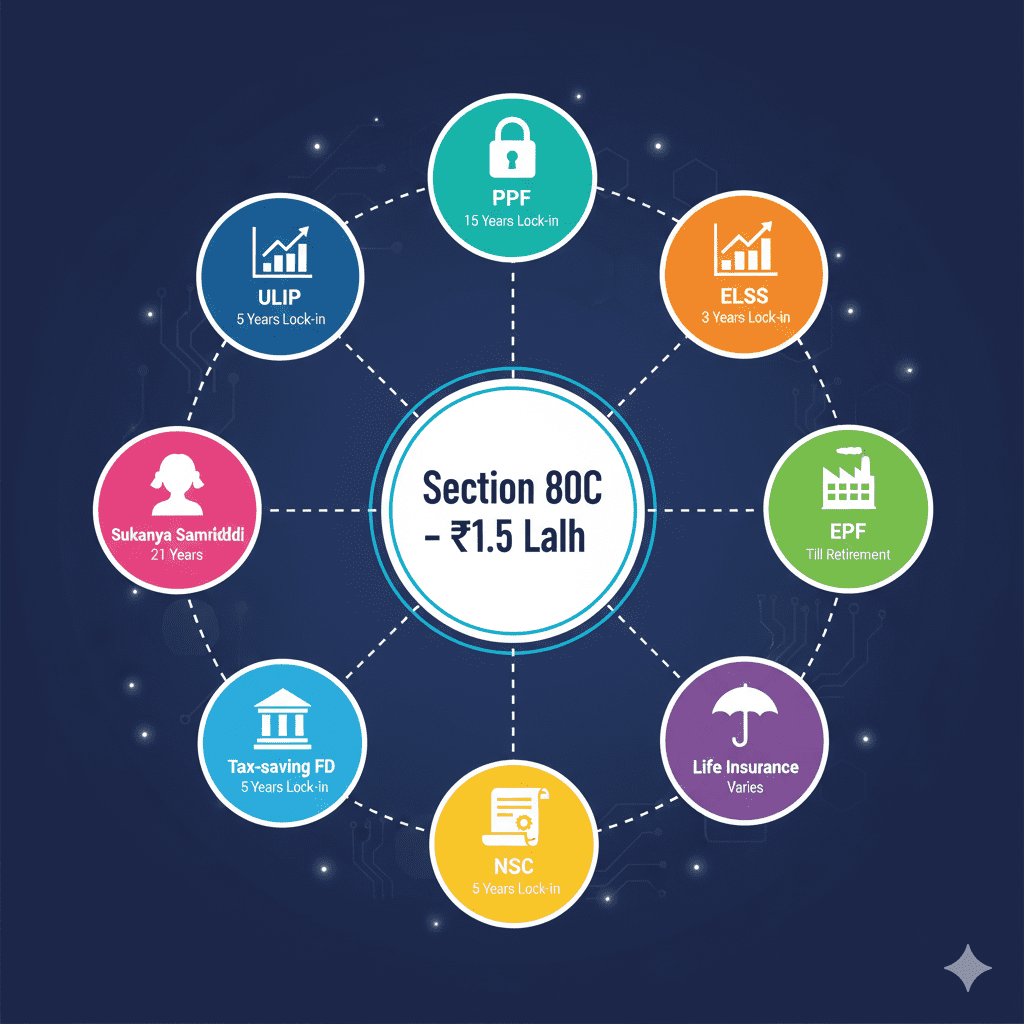

SECTION 80C: THE MOST IMPORTANT DEDUCTION

If you choose the Old Regime, Section 80C is your best friend. It allows deduction of up to ₹1,50,000 from your taxable income.

What Investments Qualify Under 80C?

| Investment | Lock-in Period | Returns | Risk |

|---|---|---|---|

| PPF (Public Provident Fund) | 15 years | 7.1% (current) | Low |

| ELSS (Equity Linked Savings Scheme) | 3 years | Market-linked (10-15%) | Moderate |

| EPF (Employee Provident Fund) | Till retirement | ~8% | Low |

| Life Insurance Premium | Policy term | Varies | Low |

| NSC (National Savings Certificate) | 5 years | ~7% | Low |

| Tax-saving FDs | 5 years | 6-7% | Low |

| Sukanya Samriddhi Yojana | 21 years | 8.2% | Low |

| ULIP | 5 years | Market-linked | Moderate |

How 80C Saves Tax

Example: Rahul earns ₹9 lakh, invests ₹1.5 lakh in PPF.

| Calculation | Without 80C | With 80C |

|---|---|---|

| Income | ₹9,00,000 | ₹9,00,000 |

| Less: 80C | Nil | (₹1,50,000) |

| Taxable Income | ₹9,00,000 | ₹7,50,000 |

| Tax (Old Regime) | ₹1,17,000 | ₹77,500 |

| Tax Saved | – | ₹39,500 |

80C Strategy for Beginners

| If You… | Suggested 80C Investment |

|---|---|

| Want safety, long-term | PPF (start with ₹500/month) |

| Want higher returns, 3-year lock-in | ELSS (via SIP) |

| Want guaranteed returns | Tax-saving FD (5 years) |

| Have a girl child | Sukanya Samriddhi Yojana |

| Want retirement focus | EPF + PPF combination |

Pro Tip: Use India Tax Tools’ 80C Calculator to see how much you can save.

OTHER DEDUCTIONS YOU SHOULD KNOW

Beyond 80C, several deductions can further reduce your tax.

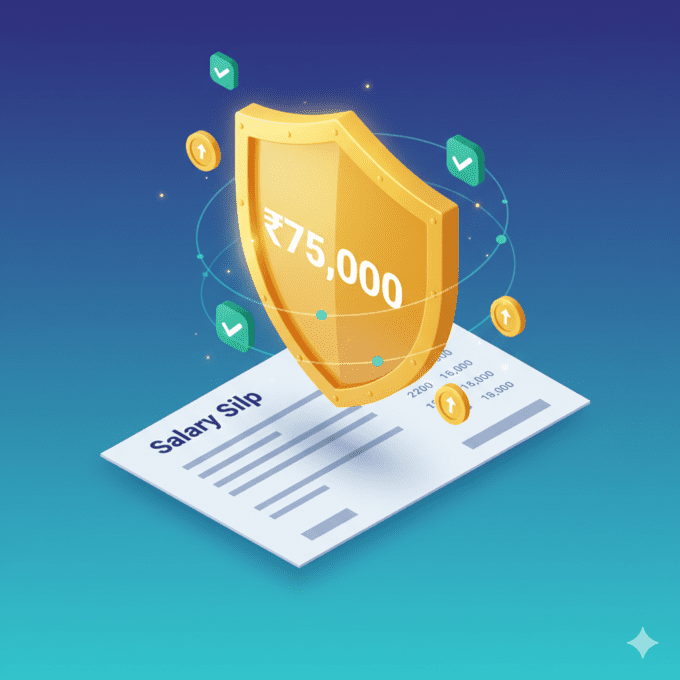

Section 80D: Health Insurance Premium

| Who | Maximum Deduction |

|---|---|

| Self + Family | ₹25,000 |

| Parents (below 60) | ₹25,000 |

| Parents (above 60) | ₹50,000 |

| Total (self + senior parents) | Up to ₹75,000 |

Tip: Even a basic health policy of ₹5-10 lakh cover qualifies.

Section 80CCD(1B): NPS Additional Deduction

-

Extra ₹50,000 deduction for investing in National Pension System (NPS)

-

Over and above ₹1.5 lakh 80C limit

-

Ideal for young taxpayers building retirement corpus

Section 24(b): Home Loan Interest

-

Deduction up to ₹2,00,000 on interest paid for self-occupied property

-

No upper limit for let-out property

Section 80E: Education Loan Interest

-

Deduction for interest paid on education loan

-

No upper limit

-

Available for 8 years or until interest paid, whichever earlier

Section 80G: Donations

-

50% or 100% deduction on donations to specified funds

-

Must be made to eligible charities (check 80G list)

Section 10(13A): HRA (House Rent Allowance)

For salaried employees living in rented accommodation, HRA exemption can be claimed. Exemption is least of:

- Actual HRA received

- Rent paid minus 10% of salary

- 50% of salary (metro cities) / 40% (non-metro)

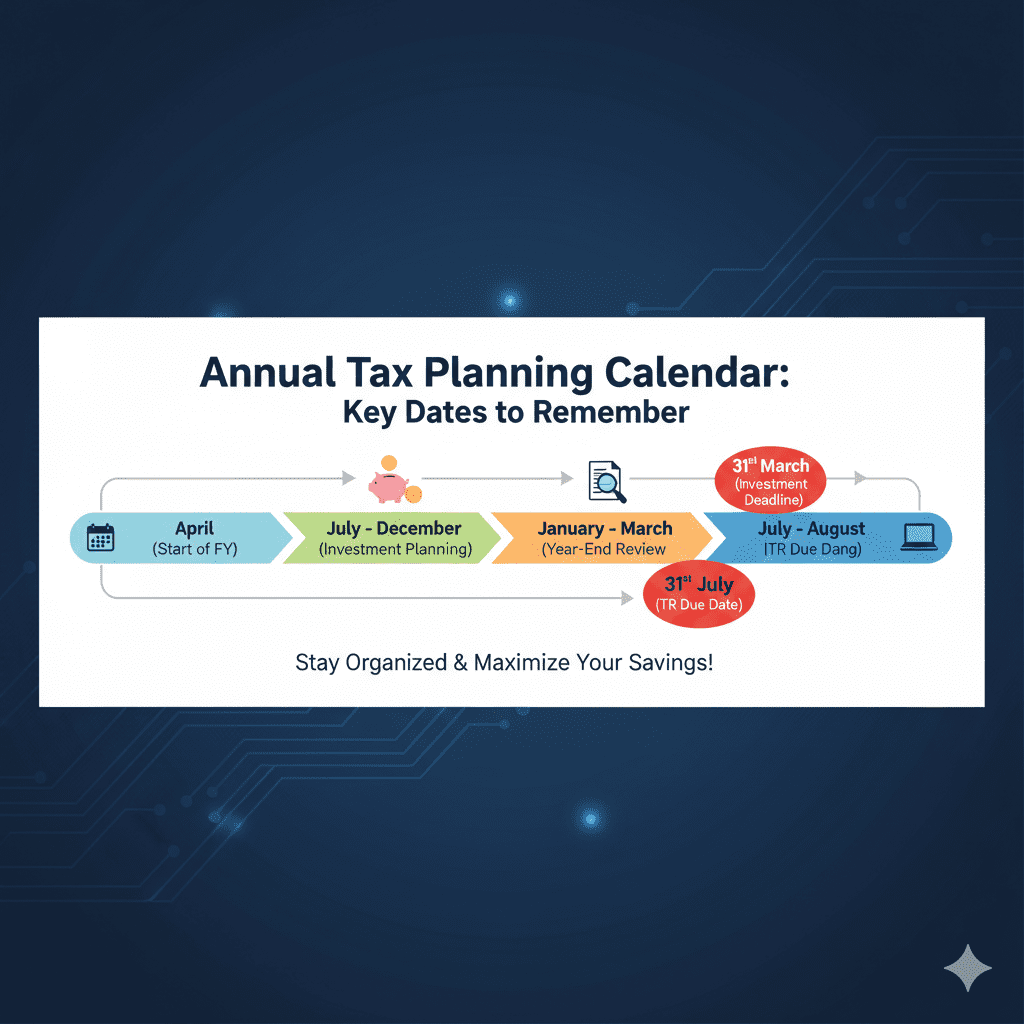

STEP-BY-STEP TAX PLANNING FOR FIRST-TIME TAXPAYERS

Follow this simple annual cycle.

Step 1: Estimate Your Income (April-May)

Calculate expected income for the year:

-

Salary (basic, HRA, allowances, bonus)

-

Interest (savings account, FD)

-

Freelance/business income

-

Any other income

Step 2: Choose Your Regime (June)

| Action | Tool |

|---|---|

| Calculate tax under both regimes | India Tax Tools’ Advanced Tax Calculator |

| Decide which regime saves more | Compare results |

| If choosing Old Regime, plan investments | See Step 3 |

Step 3: Plan Investments (July-December)

| Deduction | Target | Suggested Investment |

|---|---|---|

| 80C | ₹1,50,000 | PPF, ELSS, EPF combination |

| 80D | ₹25,000+ | Health insurance for self & family |

| 80CCD(1B) | ₹50,000 | NPS Tier 1 account |

| HRA | As applicable | Rent payments |

Step 4: Track and Adjust (January-March)

-

Check if you’re on track to meet investment targets

-

If short, make additional investments before March 31

-

Review any changes in income (bonus, new job)

Step 5: File Your Return (July-August)

-

Collect Form 16 (from employer)

-

Download Form 26AS and AIS

-

File ITR online

-

E-verify (Aadhaar OTP is fastest)

TAX PLANNING FOR FREELANCERS AND SELF-EMPLOYED

If you’re a freelancer or run a small business, your tax planning is slightly different.

Key Differences from Salaried

| Aspect | Salaried | Freelancer |

|---|---|---|

| TDS | Deducted by employer | May have TDS from clients |

| Expenses | Limited exemptions | Can claim business expenses |

| Advance Tax | Not required (usually) | Required if tax > ₹10,000 |

| Presumptive Taxation | Not applicable | Option under 44ADA (up to ₹75L receipts) |

Presumptive Taxation Under Section 44ADA

If your gross receipts are up to ₹75 lakh:

-

Declare 50% of receipts as profit

-

No need to maintain detailed books

-

No audit required

-

Tax calculated on presumed profit

Example: Priya (freelancer) has ₹60 lakh receipts.

-

Presumed profit = ₹30 lakh (50%)

-

Tax on ₹30 lakh (Old Regime) = ₹6,45,000 approx

-

Much simpler than calculating actual expenses

Expenses Freelancers Can Claim

| Expense Category | Examples |

|---|---|

| Office rent | Co-working space, home office portion |

| Equipment | Laptop, phone, printer, software |

| Internet/phone | Proportionate to business use |

| Travel | Client meetings, conferences |

| Professional fees | CA fees, legal expenses |

| Marketing | Website, ads, business promotion |

COMMON TAX PLANNING MISTAKES BEGINNERS MAKE

| Mistake | Why It Hurts | How to Avoid |

|---|---|---|

| Not filing at all | Penalty up to ₹10,000 | File even if nil tax |

| Choosing wrong regime | Pay more tax than necessary | Calculate both before deciding |

| Missing 80C deadline | Lose ₹1.5L deduction | Invest before 31st March |

| Ignoring Form 26AS | Mismatches lead to notices | Download and verify before filing |

| Not claiming HRA | Lose thousands in exemption | Submit rent receipts to employer |

| Forgetting bank interest | Interest > ₹10,000 not reported | Declare in “Other Sources” |

| Not paying advance tax | Interest under 234B/234C | Pay if tax liability > ₹10,000 |

| Investing without goal | Locked money, wrong product | Match investment to goal (80C vs retirement) |

| Not e-verifying ITR | Return considered invalid | E-verify immediately after filing |

![]()

FREQUENTLY ASKED QUESTIONS

Q1: I’m a first-time taxpayer. Do I need to file ITR?

Yes, if your income exceeds the basic exemption limit:

-

New Regime: > ₹4,00,000

-

Old Regime: > ₹2,50,000 (below 60 years)

Even if income is below threshold, filing is recommended for:

-

Visa applications

-

Loan eligibility

-

Proof of income

Q2: Which tax regime is better for beginners?

For most first-time earners with no major investments, the New Tax Regime is better due to lower rates and the ₹75,000 standard deduction. However, always calculate both using a tax calculator .

Q3: What is Section 80C and how much can I save?

Section 80C allows deduction of up to ₹1.5 lakh on specified investments (PPF, ELSS, EPF, etc.). In the old regime, this can save you up to ₹46,800 in tax (for 30% slab) .

Q4: When is the last date to invest for tax saving?

For FY 2025-26, investments must be made by 31st March 2026 to claim deduction for that year.

Q5: I have no investments. Can I still save tax?

Yes, through:

-

New Regime (lower rates + standard deduction)

-

HRA (if you pay rent)

-

80D (health insurance)

-

80CCD(1B) (NPS – even without other 80C)

Q6: What is Form 26AS and why is it important?

Form 26AS is your tax credit statement. It shows:

-

TDS deducted on your income

-

Advance tax paid

-

Self-assessment tax paid

Always verify it matches your income before filing ITR.

Q7: Do freelancers need to pay advance tax?

Yes, if your tax liability exceeds ₹10,000 in a year. Advance tax is due in installments:

-

15th June: 15%

-

15th September: 45%

-

15th December: 75%

-

15th March: 100%

Q8: What is the penalty for not filing ITR?

Late filing fee under Section 234F:

-

₹5,000 if filed by 31st December

-

₹10,000 if filed after 31st December

-

₹1,000 if total income ≤ ₹5 lakh

Q9: Can I switch between tax regimes every year?

Yes (for individuals with income from salary/business). You can choose the regime that benefits you most each year. However, business owners opting for presumptive taxation have restrictions.

Q10: What documents do I need for first-time filing?

-

PAN Card

-

Aadhaar Card

-

Form 16 (from employer)

-

Bank account details (for refund)

-

Form 26AS (download from portal)

-

Investment proofs (if claiming deductions)

ACTIONABLE CHECKLIST: FIRST-TIME TAXPAYER

Before the Financial Year (April)

-

Understand your estimated income for the year

-

Decide which tax regime suits you (calculate both)

-

If choosing old regime, plan 80C investments

During the Year (May-February)

-

Track TDS deducted (check Form 26AS periodically)

-

Make 80C investments systematically (SIP in ELSS, monthly PPF)

-

Pay advance tax if applicable (freelancers/business)

-

Keep records of all investments and rent receipts

Before March 31 (Year-End)

-

Ensure 80C investments total ₹1.5 lakh (if old regime)

-

Make any top-up investments if short

-

Pay health insurance premium (80D)

-

Check if NPS additional ₹50,000 (80CCD(1B)) is beneficial

-

Verify all TDS is correctly credited in Form 26AS

At Filing Time (July-August)

-

Collect Form 16 from employer

-

Download Form 26AS and AIS from income tax portal

-

Calculate total income (salary + interest + other)

-

Choose regime and compute tax using India Tax Tools’ Advanced Tax Calculator

-

File ITR online (ITR-1 for salary, ITR-3 for freelancers)

-

E-verify immediately (Aadhaar OTP)

-

Save acknowledgement for records

SUCCESS STORY: HOW ROHIT SAVED ₹47,000 IN HIS FIRST YEAR

Profile: Rohit, 24, first job as business analyst in Mumbai

Salary: ₹9.2 lakh per annum

First year (without planning) :

| Item | Amount |

|---|---|

| Income | ₹9,20,000 |

| Standard deduction | ₹50,000 |

| Taxable | ₹8,70,000 |

| Tax paid (old regime) | ₹1,00,000 approx |

Second year (with planning) :

| Action | Amount |

|---|---|

| Chose New Regime (after calculation) | Lower rates |

| No 80C investments needed | – |

| Standard deduction ₹75,000 | ₹75,000 |

| Taxable | ₹8,45,000 |

| Tax (new regime) | ₹65,000 |

Savings: ₹35,000 in tax + ₹12,000 saved from not investing unnecessarily = ₹47,000

“I almost blindly followed friends who invested in ELSS and LIC. But after calculating, the new regime saved me more. Don’t assume—calculate first.” – Rohit

CONCLUSION: YOUR TAX JOURNEY STARTS HERE

Tax planning isn’t complicated—it’s just knowing the rules and applying them to your situation. For first-time taxpayers, the key takeaways are simple:

- Understand your income – all sources, including interest

- Choose your regime wisely – calculate both, don’t assume

- Use deductions if beneficial – 80C, 80D, HRA, NPS

- File on time – avoid penalties and stress

- Use tools – calculators make it easy

Your Next Steps

-

Calculate your tax using India Tax Tools’ Advanced Tax Calculator

-

Decide your regime before making investments

-

Start small – even ₹500/month in PPF or ELSS adds up

-

Set reminders for investment deadlines (31st March) and filing (31st July)

-

Stay informed – tax rules change; follow reliable sources

Remember: Tax planning isn’t about avoiding tax—it’s about paying exactly what you owe, no more, no less. Start early, stay consistent, and watch your savings grow.

“Tax planning isn’t about how much you earn—it’s about how much you keep. Start early, calculate wisely, and let the rules work for you.”

Disclaimer: This article is for informational and educational purposes only. Tax laws, rates, and deductions are subject to change based on government notifications. Please consult a qualified Chartered Accountant for advice tailored to your specific situation. The information provided is based on Budget 2026 announcements and current provisions as of February 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment